What is the Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam?

What is the Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam?

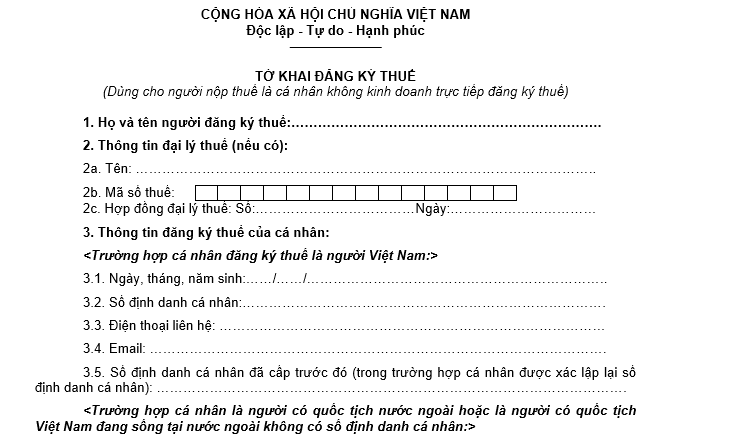

Pursuant to Form 05-DK-TCT issued together with Circular 86/2024/TT-BTC, the taxpayer registration declaration is stipulated as follows:

Download Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86.

Note: Form 05-DK-TCT - Taxpayer registration declaration is used for individuals not engaged in business for direct taxpayer registration.

What is the Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam? (Image from the Internet)

What are instructions for completing Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam?

Below is Form 05-DK-TCT - Taxpayer registration declaration according to Circular 86:

1. Full Name: Clearly and completely write the individual's name in uppercase letters for taxpayer registration.

2. Tax Agent Information: Fully fill out the information of the tax agent in cases where the tax agent is contracted with the taxpayer to carry out taxpayer registration procedures on behalf of the taxpayer in accordance with the Law on Tax Administration.

3. Personal Taxpayer Registration Information

* For individuals who are Vietnamese citizens, fill in items 3.1 to 3.4 below:

3.1. Date of Birth: Clearly write the date of birth of the individual registering taxpayer.

3.2. Personal Identification Number: Write the individual's identification number used for taxpayer registration.

Note: Individuals must accurately declare their full name, date of birth, and personal identification number according to the information stored in the National Population Database.

3.3. Contact Phone: Accurately write the individual's phone number.

3.4. Email: Accurately write the individual's email address.

* For individuals who are foreign nationals or Vietnamese nationals residing abroad without a personal identification number, fill in items 3.1 to 3.8 below:

3.1. Date of Birth: Clearly write the date of birth of the individual registering taxpayer.

3.2. Gender: Check one of the two boxes Male or Female.

3.3. Nationality: Clearly write the nationality of the individual registering taxpayer.

3.4. Legal Documents: Check the box for one of the documents such as passport/laissez-passer/border ID/other valid personal identification document of the individual and clearly write the number, date of issue, and "place of issue," which should only specify the province or city where it was issued.

3.5. Permanent Address: Fully write all information regarding the individual's place of permanent residence.

3.6. Current Address: Fully write all information regarding the individual's current place of residence (only write if this address is different from the permanent residence address).

3.7. Write the phone number of the individual registering taxpayer.

3.8. Write the email address of the individual registering taxpayer (if any).

The taxpayer must fully and accurately declare the email information. This email address is used as an electronic transaction account with the tax authority for electronic taxpayer registration documents.

* Signature and full name of the taxpayer registration: The taxpayer registration individual must sign and write their full name in this section.

* Tax Agent Employee: In cases where the tax agent registers on behalf of the taxpayer, fill in this information.

Where do individuals not engaged in business submit their initial taxpayer registration dossier in Vietnam?

According to Article 32 of the Law on Tax Administration 2019, the location for submitting the initial taxpayer registration documents is stipulated as follows:

Article 32. Location for Submitting Initial Taxpayer Registration Documents

- Taxpayers registering together with business registration, cooperative registration, business registration, submit the taxpayer registration documents at the location for submitting business registration, cooperative registration, business registration according to the provisions of the law.

- Taxpayers registering directly with the tax authority submit their taxpayer registration documents at the following locations:

a) Organizations, business households, and business individuals submit taxpayer registration documents at the tax authority where the organization, business household, and business individual have their headquarters;

b) Organizations and individuals responsible for withholding and submitting taxes on behalf of others submit taxpayer registration documents at the tax authority managing the organization or individual directly responsible for withholding and submitting taxes;

c) Households and individuals not engaged in business submit taxpayer registration documents at the tax authority where taxable income arises, where their permanent residence is registered, where temporary residence is registered, or where obligations with the state budget arise.

- Individuals authorizing organizations or individuals to pay income to register taxpayers on behalf of themselves and their dependents, submit taxpayer registration documents through the organization or individual paying the income. The organization or individual paying the income is responsible for compiling and submitting taxpayer registration documents on behalf of the individual to the tax authority managing the organization or individual paying the income.

As per these regulations, individuals not engaged in business directly registering taxpayers with the tax authority must submit taxpayer registration documents at the tax authority where taxable income arises, where their permanent residence is registered, where their temporary residence is registered, or where obligations with the state budget arise.