What are rates for license fee for organizations engaged in the production of goods and services with charter capital of VND 10 billion or less in Vietnam?

What are rates for license fee for organizations engaged in the production of goods and services with charter capital of VND 10 billion or less in Vietnam?

According to Article 4 of Decree 139/2016/ND-CP (amended and supplemented by Clause 2, Article 1 of Decree 22/2020/ND-CP), the rate of the license fee is prescribed as follows:

Article 4. Rate of license fee

- The rate of license fee for organizations engaged in the production and trading of goods and services is as follows:

a) Organizations with a charter capital or investment capital above 10 billion VND: 3,000,000 VND/year;

b) Organizations with a charter capital or investment capital of up to 10 billion VND: 2,000,000 VND/year;

c) Branches, representative offices, business locations, public service providers, and other economic organizations: 1,000,000 VND/year.

The rate of license fee for organizations specified in points a and b of this clause is based on the charter capital stated in the business registration certificate; in the absence of charter capital, it is based on the investment capital stated in the investment registration certificate.

- The rate of license fee for individuals and households engaged in the production and trading of goods and services is as follows:

a) Individuals, groups of individuals, and households with an annual revenue above 500 million VND: 1,000,000 VND/year;

b) Individuals, groups of individuals, and households with an annual revenue over 300 million to 500 million VND: 500,000 VND/year;

c) Individuals, groups of individuals, and households with an annual revenue over 100 million to 300 million VND: 300,000 VND/year.

[...]

Thus, the rate of the license fee for organizations engaged in the production of goods and services with a charter capital of up to 10 billion VND is 2,000,000 VND per year.

What are rates for license fee for organizations engaged in the production of goods and services with charter capital of VND 10 billion or less in Vietnam? (Image from the Internet)

Which entities are exempt from the license fee in Vietnam ?

According to Article 3 of Decree 139/2016/ND-CP (amended and supplemented by Clause 1, Article 1 of Decree 22/2020/ND-CP), the subjects exempt from business license tax include:

- Individuals, groups of individuals, and households engaged in production and trading with an annual revenue of up to 100 million VND.

- Individuals, groups of individuals, and households engaging in irregular production and trading; without a fixed location as guided by the Ministry of Finance.

- Individuals, groups of individuals, and households producing salt.

- Organizations, individuals, groups of individuals, and households engaged in aquaculture, fishing, and fishery logistics services.

- Cultural post offices of communes; press agencies (print, spoken, visual, and electronic media).

- Cooperatives and unions of cooperatives (including branches, representative offices, business locations) engaged in agriculture as stipulated in the law on agricultural cooperatives.

- People's credit funds; branches, representative offices, and business locations of cooperatives, unions of cooperatives, and private enterprises operating in mountainous areas. Mountainous areas are determined according to the regulations of the Committee for Ethnic Affairs.

- Exemption from business license tax in the first year of establishment or starting production and business activities (from January 1 to December 31) for:

+ Newly established organizations (granted a new tax code, new enterprise code).

+ Households, individuals, groups of individuals starting production and business activities for the first time.

+ During the business license tax exemption period, if an organization, household, individual, or group of individuals establishes a branch, representative office, or business location, those branches, representative offices, and business locations are exempt from the business license tax during this period.

- Small and medium enterprises converted from business households (as stipulated in Article 16 of the Law on Support for Small and Medium Enterprises 2017) are exempt from the business license tax for 3 years from the date of being granted the first business registration certificate.

+ During the business license tax exemption period, if small and medium enterprises establish branches, representative offices, or business locations, those branches, representative offices, and business locations are exempt during the period the small and medium enterprise is exempt.

+ Branches, representative offices, and business locations of small and medium enterprises (eligible for business license tax exemption according to Article 16 of the Law on Support for Small and Medium Enterprises 2017) established before February 25, 2020, will have their exemption period calculated from February 25, 2020, until the end of the enterprise's exemption period.

+ Small and medium enterprises converted from business households before February 25, 2020, will follow the business license tax exemption provisions in Article 16 and Article 35 of the Law on Support for Small and Medium Enterprises 2017.

- Public primary and preschool educational institutions.

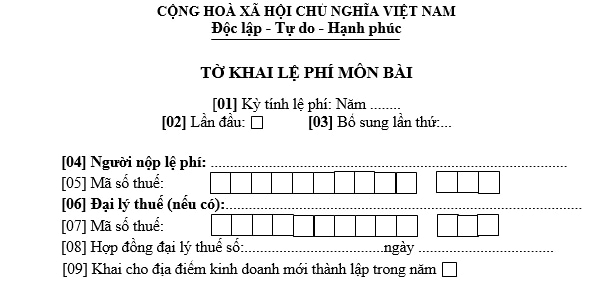

What is the Form of license fee declaration according to Circular 80 in Vietnam?

In the Appendix issued with Circular 80/2021/TT-BTC, the form of the license fee declaration is prescribed as follows:

Download the license fee declaration form according to Circular 80