Form 04-DK-TCT - Taxpayer registration declaration under Circular 86 in Vietnam and Instructions

What are details of the Form 04-DK-TCT - Taxpayer registration declaration according to Circular 86 and instructions for completion?

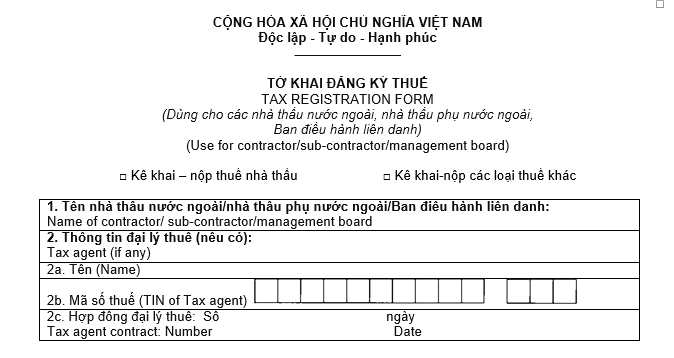

Pursuant to Form 04-DK-TCT issued together with Circular 86/2024/TT-BTC, the Form 04-DK-TCT - Taxpayer registration declaration is as follows:

Download Form 04-DK-TCT - Taxpayer registration declaration according to Circular 86

Note: Form 04-DK-TCT - Taxpayer registration declaration is for foreign contractors, foreign sub-contractors/Joint Operation Boards

Form 04-DK-TCT - Taxpayer registration declaration under Circular 86 in Vietnam and Instructions (Image from the Internet)

What are instructions for filling Form 04-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam?

Below are the instructions for filling Form 04-DK-TCT - Taxpayer registration declaration according to Circular 86 in Vietnam:

Taxpayers must check one of the appropriate boxes before declaring detailed information. To be specific:

Contractor/sub-contractor/management board must select one of the appropriate boxes before declaring detailed information, as follows:

- “Kê khai-nộp thuế nhà thầu”: Applicable to cases where a foreign contractor, foreign sub-contractor, or Joint Operation Board directly declares and pays contractor tax with the tax department (VAT, CIT according to the provisions of foreign contractor tax law and tax management law).

“Contractor tax declaration and payment”: Applicable to the contractor/sub-contractor/management board for direct contractor tax declaration and payment and submission to the tax department (VAT, CIT in accordance with the contractor tax law and tax management law).

- “Kê khai - nộp các loại thuế khác”: Applicable to cases where a foreign contractor, foreign sub-contractor directly declares personal income tax, license fees, etc. with the tax department and the Vietnamese party declares, deducts, and pays on behalf of foreign contractor tax according to the provisions of foreign contractor tax law and tax management law.

“Other tax and fee declaration and payment”: Applicable to the contractor/sub-contractor/management board for direct PIT, other fees declaration and payment and submission to the tax department, and Vietnamese parties deduct and pay on behalf of contractor/sub-contractor regarding VAT, CIT in accordance with the contractor tax law and tax management law.

1. Name of contractor/sub-contractor/management board: Write the full name (including abbreviated name) of the contractor or sub-contractor or management board engaged in business activities in Vietnam not under the forms stipulated in the Law of Investment.

2. Information of Tax agent: Write the full information of the tax agent in case the Tax agent signs a contract with the taxpayer to carry out taxpayer registration procedures on behalf of the taxpayer, according to the Tax Management Law.

3. Nationality: Fill in clearly the nationality of the contractor/sub-contractor/management board.

4. Address of head office:

If the taxpayer is an individual, fill in the address, telephone number, fax number of residence.

If the taxpayer is an organization or company, fill in the address, telephone number, fax number of the head office.

5. Address of Management office in Vietnam:

If the taxpayer is an individual, fill in the address, telephone number, fax number of the individual residing in Vietnam to conduct business.

If the contractor/sub-contractor is an organization or company, fill in the address, telephone number, fax number of the management office in Vietnam.

6. Business license in Vietnam: Based on the business license granted by the competent Government authority, fill in the relevant items in the form (if any).

7. Contract for contractor/sub-contractor operation in Vietnam: Based on the signed contract, fill in the relevant items in the form if selecting “Contractor tax declaration and payment”.

8. Contract objectives: Declare each operation objective of the contract concretely if selecting “Contractor tax declaration and payment”.

9. Location of business according to the contract: Declare each operation location of the contract concretely. In case of doing business at many different locations, the contractor/sub-contractor has to declare fully the locations to do business if selecting “Contractor tax declaration and payment”.

10. Contract duration: Fill in clearly the contract duration from month, year to month, year if selecting “Contractor tax declaration and payment”.

11. Do you have a sub-contractor: If there are sub-contractors taking part in the contract, please declare fully in the Sub-contractor form of BK04-DK-TCT declaration attached.

12. Declare information of representative of contractor (or sub-contractor): Provide specific information about the representative of the contractor (or sub-contractor).

13. Declare information of VAT calculation method: if selecting “Contractor tax declaration and payment”.

14. Declare information of CIT calculation method: if selecting “Contractor tax declaration and payment”.

15. Declare information of financial year (From ... to ...): Indicate the financial year as the calendar year. If the financial year is different from the calendar year, declare information is from the starting quarter to the ending quarter and the financial year must be a full 12 months.

16. Attachments: List all documents attached to the Tax Registration Form.

17. Staff tax agent: Staff tax agent must declare the name and certificate number in this area if the tax agent declares on behalf of the contractor/sub-contractor.

What does the first-time taxpayer registration dossier for an organization registering directly with the tax authorities in Vietnam include?

Based on Article 31 of the Tax Management Law 2019 stipulating the first-time taxpayer registration dossier:

Article 31. First-time taxpayer registration dossier

- Taxpayers registering taxpayers together with enterprise registration, cooperative registration, business registration shall have their taxpayer registration dossier as their enterprise registration dossier, cooperative registration, business registration according to the provisions of law.

- Taxpayers who are organizations registering taxpayers directly with the tax department shall have their taxpayer registration dossier include:

a) Taxpayer registration declaration;

b) A copy of the establishment and operation license, decision on establishment, certificate of investment registration, or other equivalent documents issued by the competent authority that remain valid;

c) Other relevant documents.

- Taxpayers who are households, household businesses, individuals registering taxpayers directly with the tax department shall have their taxpayer registration dossier include:

a) Taxpayer registration declaration or tax declaration;

b) Copy of identification card, copy of citizen identification card, or copy of passport;

c) Other relevant documents.

[...]

According to the above provisions, the first-time taxpayer registration dossier for organizations registering taxpayers directly with the tax department includes the following documents:

- Taxpayer registration declaration

- A copy of the establishment and operation license, decision on establishment, certificate of investment registration, or other equivalent documents issued by the competent authority that remain valid

- Other relevant documents