What income does the PIT declaration form - Form 04/CNV-TNCN in Vietnam apply to?

What income does the PIT declaration form - Form 04/CNV-TNCN in Vietnam apply to?

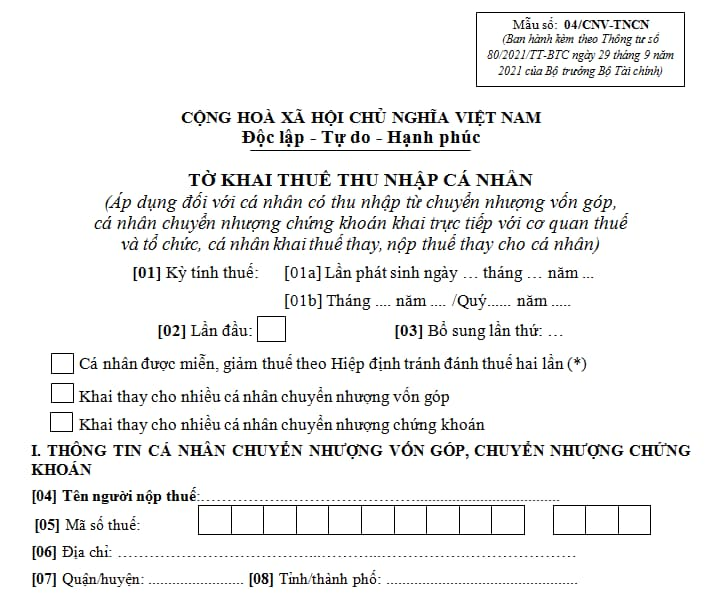

The PIT declaration form - Form 04/CNV-TNCN applies to individuals with income from contributed capital transfer or securities transfer who directly declare with the tax authority, and organizations or individuals declaring and paying tax on behalf of the individuals as specified in Appendix 2 issued together with Circular 80/2021/TT-BTC as follows:

Download the PIT declaration form - Form 04/CNV-TNCN: Here

What income does the PIT declaration form - Form 04/CNV-TNCN in Vietnam apply to? (Image from the Internet)

What does the PIT declaration dossier for individuals with income from capital transfer who directly declare tax with the tax authority in Vietnam include?

Under Section 9.4 of Appendix 1 issued together with Decree 126/2020/ND-CP, the PIT declaration dossier for individuals with income from capital transfer who directly declare tax with the tax authority in Vietnam includes:

- PIT declaration form (applicable to individuals with income from capital contribution transfers, individuals transferring securities who directly declare with the tax authority, and organizations or individuals declaring and paying tax on behalf of the individuals) according to Form 04/CNV-TNCN (issued together with Appendix 2 Circular 80/2021/TT-BTC).

- A copy of the Capital Transfer Agreement.

- A copy of documents determining the value of capital contributions according to accounting books; in case of capital contribution by repurchase, a transfer agreement must be presented.

- Copies of documents proving the costs related to determining income from the contributed capital transfer as prescribed in Appendix 1 Decree 126/2020/ND-CP.

What authorities receive the PIT declaration dossiers submitted by individuals with income from capital transfer who directly declare tax with the tax authority in Vietnam?

Under Point e, Clause 6, Article 11 Decree 126/2020/ND-CP, the regulation is as follows:

Tax declaration dossier submission location

Tax declaration dossiers shall be submitted at the locations specified in Clauses 1, 2 and 3 Article 45 of the Law on Tax administration and the following locations:

...

6. Declarations of taxes that have to be declared and paid separately shall be submitted to the supervisory tax authorities as prescribed in Point b Clause 4 Article 45 of the Law on Tax administration, except in the following cases:

a) In the cases specified in Points a, d, e, k Clause 4 Article 8 of this Decree, tax declaration dossiers shall be submitted to tax authorities responsible for the areas where business operations take place or where other taxes.

b) Tax declaration dossiers of exports and imports prescribed in Point c Clause 4 Article 8 of this Decree shall be submitted to the customs authorities where the customs declarations are registered.

In case a new customs declaration has to be made when paying tax during the export or import process, the tax declaration dossier shall be submitted to the customs authority to which the first export or import declaration is submitted.

c) Declarations of corporate income tax on capital transfer by foreign contractors shall be submitted to the supervisory tax authorities of the enterprises in which the foreign contractors invest capital (including the cases in which the transferee declares tax on behalf of the foreign contractor, or, if the tax is declared by the organization established in accordance with Vietnam’s law and invested in by the foreign contractor in case the transferee is also a foreign contractor).

d) Contractors shall submit declarations of corporate income tax on transfer of the right to participate in petroleum agreements to their supervisory tax authorities (including change of owner of the contractor holding the right to participate in the petroleum agreement).

dd) Individuals that have income from capital transfer or capital investment and declare tax directly with tax authorities shall submit tax declaration dossiers to the supervisory tax authorities of the issuers.

e) Individuals having income from copyrights, franchising, wining prizes overseas; receipt of inheritance, gifts that are other kinds of property (except real estate or property subject to registration of right to ownership or enjoyment) overseas shall submit tax declaration dossier to the supervisory tax authorities of the areas where they reside.

g) Individuals having income from leasing out property (except real estate) shall submit tax declaration dossiers to the supervisory tax authorities of the areas where they reside. Individuals having income from leasing out real estate in Vietnam shall submit tax declaration dossiers to the supervisory tax authorities of the areas where the real estate is located. Individuals leasing out overseas real estate shall submit tax declaration dossiers to the supervisory tax authorities of the areas where they reside.

h) Individuals having income from receipt of inheritance or gifts that are other property subject to registration of right to ownership or enjoyment) shall submit tax declaration dossiers to the tax authorities where registration fees are declared.

i) Household businesses and individual businesses that do not have fixed business locations and regular business operation shall submit declarations to supervisory tax authorities of the areas where the individuals reside.

k) Organizations and individuals applying for registration of right to ownership and right to enjoyment of property except housing and land (including the cases in which registration fees are exempted as prescribed by law) shall submit registration fee declarations to the tax authorities to which the application is submitted or another location decided by the President of the People’s Committee of the province.

...

Thus, individuals with income from capital transfer who directly declare tax with the tax authority in Vietnam will submit the tax declaration dossiers to the supervisory tax authorities of the issuers.

- When is the deadline for paying tax, duty payment guarantee and tax deposit in Vietnam?

- Are natural aquatic resources exempt from severance tax in Vietnam?

- Are natural swallow's nests subject to severance tax in Vietnam?

- What are the principles for developing a List of goods to be imported free of duty in Vietnam?

- How long is the CIT period of the first year in Vietnam?

- Shall individuals be entitled to tax refund if their taxed incomes do not reach a tax-liable level in Vietnam?

- What are regulations on responsibilities of income payer regarding PIT refund when being delegated to settle tax in Vietnam?

- Is it necessary to terminate the tax identification number when a business temporarily suspends its operations in Vietnam?

- What is the value-added tax declaration form for 2024 in Vietnam?

- What are forms for declaring corporate income tax in Vietnam?