What is the Form 07/DK-NPT-TNCN - Dependant registration form for personal income tax declaration in Vietnam?

What is the Form 07/DK-NPT-TNCN - Dependant registration form for personal income tax declaration in Vietnam?

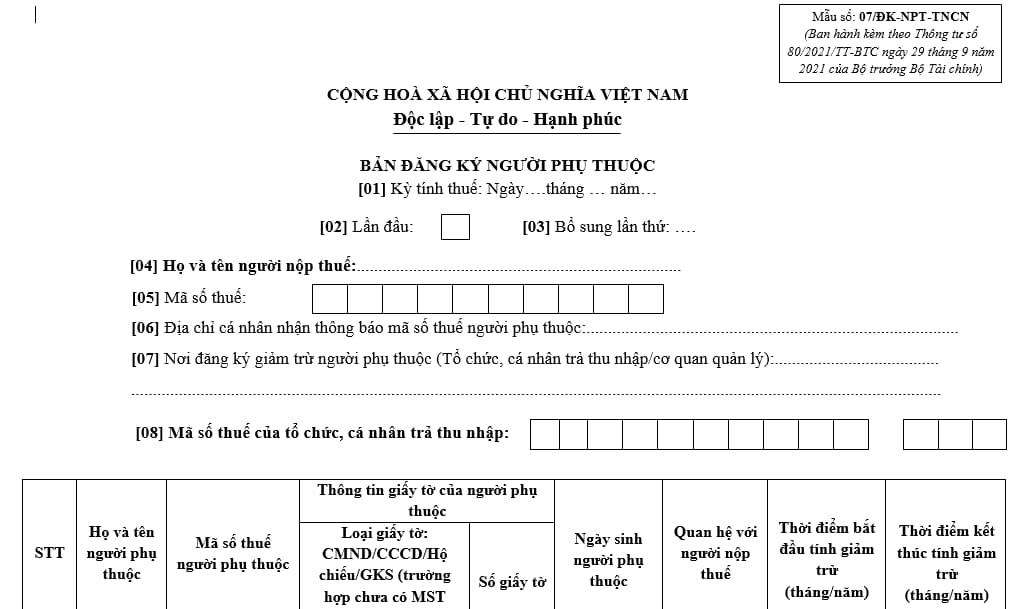

The current dependant registration form is Form 07/DK-NPT-TNCN, specified in Section 7 of Appendix II issued together with Circular 80/2021/TT-BTC as follows:

Download Form 07/DK-NPT-TNCN dependant registration form: Here

What is the Form 07/DK-NPT-TNCN - Dependant registration form for personal income tax declaration in Vietnam? (Image from the Internet)

What is the maximum number of dependants for personal exemption in Vietnam?

The personal exemption consists of two parts: the personal personal exemption and the dependant deduction. Taxpayers are automatically eligible for a personal personal exemption when calculating personal income tax and are not limited in the number of dependants they can register for deduction.

Based on Point c Clause 1 Article 9 of Circular 111/2013/TT-BTC, the principles for calculating personal exemptions can be summarized as follows:

- Taxpayers with income from salaries and wages are automatically eligible for a personal exemption.

- Taxpayers can claim personal exemptions for dependants once they have registered as a taxpayer and have been issued a tax code.

- Each dependant can only be claimed for deduction by one taxpayer in a given tax year. If multiple taxpayers share the same dependant, they must agree on which one will register the deduction.

Therefore, the law does not limit the number of dependants for a single taxpayer, as long as they qualify for the deduction and meet the corresponding conditions stipulated by regulations.

Which incomes are not eligible for personal exemption when calculating personal income tax in Vietnam?

According to Clause 1, Article 19 of the Personal Income Tax Law 2007 (amended and supplemented by Clause 4, Article 1 of the Amended Personal Income Tax Law 2012) and Clause 4, Article 6 of the Law on Amendments to Tax Laws 2014, personal exemptions are amounts subtracted from taxable income before calculating tax on income from business, salary, and wages for resident taxpayers.

This means that the following types of income specified in Article 2 of Circular 111/2013/TT-BTC are not eligible for personal exemptions:

(1) Income from capital investment, including:

- Loan interest.- Dividend income.- Additional value received upon dissolution of an enterprise, conversion of business models, division, separation, merger, consolidation of enterprises, or withdrawal of capital.- Income from capital investment in other forms, except for income from foreign bonds of the Government of Vietnam.

(2) Income from capital transfer, including:

- Income from transferring capital in economic organizations.- Income from transferring securities.- Income from transferring capital in other forms.

(3) Income from real estate transfers, including:

- Income from transferring land use rights and assets attached to land.- Income from transferring ownership or use rights of houses (including houses to be formed in the future).- Income from transferring land lease rights, water surface lease rights.- Other income from real estate transfers in any form.

(4) Income from winning prizes, including:

- Lottery winnings.- Prizes from promotional campaigns.- Winnings from betting.- Prizes from games, contests with prizes, and other types of winnings.

(5) Income from royalties, including:

- Income from transferring or licensing intellectual property rights.- Income from technology transfers.

(6) Income from franchising.

(7) Income from inheritances: securities, shares in economic organizations, business establishments, real estate, and other assets requiring ownership registration or use registration.

(8) Income from gifts: securities, shares in economic organizations, business establishments, real estate, and other assets requiring ownership registration or use registration.

- How long is the duration of exemption from licensing fees for a new enterprise in Vietnam? What are cases of licensing fee exemption in Vietnam?

- What are cases where the input VAT must not be deducted in Vietnam? What are the conditions for VAT input deduction?

- What are cases where personal income late payment interest is charged in Vietnam?

- How long can a taxpayer delay submitting tax declaration dossiers before their information is published in Vietnam?

- What is the Form 01/CT-KTT for amendments to the information of tax accounting books in Vietnam?

- When is the deadline for submitting annual financial statements in Vietnam? How much is the penalty for late submission?

- Shall import-export duties be paid in foreign currency in Vietnam?

- What is the excise tax rate for beer in Vietnam in 2024?

- What is coefficient K for monitoring invoicing beyond a safety threshold in Vietnam? What is the formula for calculating coefficient K in Vietnam?

- What are cases where the input VAT must not be deducted in Vietnam?