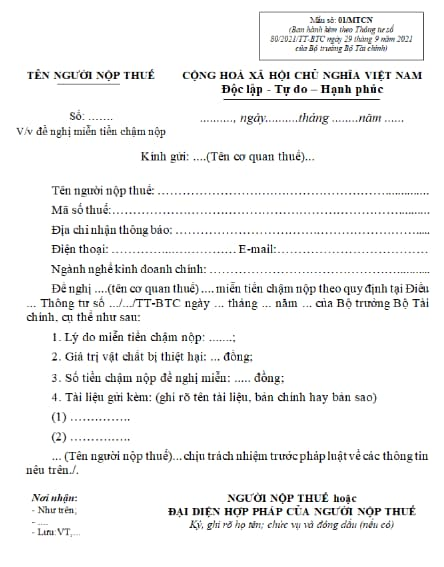

What is the Form 01/MTCN on application for exemption of late payment interest in Vietnam?

What is the Form 01/MTCN on application for exemption of late payment interest in Vietnam?

The current application form for exemption of late payment interest is Form 01/MTCN issued together with Circular 80/2021/TT-BTC, as follows:

Download Form 01/MTCN: Here

What is the Form 01/MTCN on application for exemption of late payment interest in Vietnam? (Image from the Internet)

What are cases of exemption of late payment interest in Vietnam?

According to Clause 27, Article 3 of the 2019 Law on Tax Administration, Clause 8, Article 59 of the 2019 Law on Tax Administration, and Clause 1, Article 3 of Decree 126/2020/ND-CP, taxpayers required to pay delay fees are exempted in case of force majeure.

Specific cases of force majeure include:

- Taxpayers who suffer material damage due to natural disasters, catastrophes, epidemics, fires, unexpected accidents;

- Other force majeure cases as regulated by the Government of Vietnam, including war, riots, strikes that halt production or business operations, or risks not caused by the taxpayer’s subjective fault, where the taxpayer lacks the financial ability to pay to the state budget.

How to calculate late payment interest in Vietnam?

Based on Article 59 of the 2019 Law on Tax Administration, the regulations are as follows:

Handling Late Tax Payment Fees

1. Cases where taxpayers are required to pay delay fees include:

a) Taxpayers who are late in paying taxes compared to the regulated due dates, extended due dates, dates stated in tax authority notifications, dates in tax imposition or enforcement decisions by tax authorities;

b) Taxpayers who amend tax declarations increasing the amount of tax payable, or tax authorities or authorized state agencies discover underreported tax liabilities, must pay delay fees on the additional tax amount from the day following the final tax payment due date of the erroneous tax period or from the expiry date of the original customs declaration;

c) Taxpayers who amend tax declarations decreasing the refunded tax amount or tax authorities or authorized state agencies discover that the refunded tax amount is less than what was reimbursed must pay delay fees on the reimbursed amount to be recovered from the date of receiving the refund from the state budget;

d) Cases where taxpayers are allowed to pay tax debts in installments as regulated in Clause 5, Article 124 of this Law;

e) Cases where no administrative tax management penalties are imposed due to the expiration of the statute of limitations, but the taxpayer is still subject to tax recovery as regulated in Clause 3, Article 137 of this Law;

f) Cases where no administrative tax management penalties are imposed for acts regulated in Clause 3 and Clause 4, Article 142 of this Law;

g) Agencies or organizations authorized by tax authorities to collect taxes but delay the transfer of taxpayers' taxes, delay fees, or fines to the state budget must pay delay fees on the delayed amount according to regulations.

2. The calculation rate and period for delay fees are regulated as follows:

a) The delay fee is calculated at 0.03% per day on the delayed tax amount;

b) The delay fee period is calculated continuously from the day following the delay onset as regulated in Clause 1 of this Article to the day immediately preceding the day the tax debt, refund recovery, increased tax amount, enforced tax amount, or delayed tax transfer is paid into the state budget.

3. Taxpayers self-determine the delay fees according to Clause 1 and Clause 2 of this Article and pay into the state budget as regulated. If there is excess tax payment, delay fees, or fines, the process follows Clause 1, Article 60 of this Law.

4. After 30 days from the tax payment due date, if taxpayers have not paid taxes, delay fees, or fines, tax authorities notify taxpayers about the outstanding amounts and the number of late days.

5. Delay fees are not calculated in the following cases:

a) Taxpayers providing goods and services paid by state budget funds, including subcontractors as stated in contracts with investors and directly paid by investors, are exempt from delay fees if unpaid.

The tax debt exempt from delay fees equals the unpaid amount due from the state budget but does not exceed the unpaid amount;

b) Cases regulated in Point b, Clause 4, Article 55 of this Law where delay fees are exempt during analysis, inspection, or valuation periods, pending the determination of actual payments or adjustments added to the customs value.

...

The delay fee for a 1-day period is calculated as follows:

1-Day Delay Fee Calculation = 0.03% x Delayed Tax Amount

- What is the classification of digital certificates in taxation in Vietnam?

- What is the import and export tariff schedule of Vietnam in 2024? Which goods are subject to export duties?

- What is the Form for corporate income tax for real estate transfer in Vietnam according to Circular 80?

- Vietnam: What does the supplementary personal income tax declaration dossier include?

- What are the educational requirements for tax agent employees in Vietnam?

- Shall the tax for use of collateral pending settlement be declared quarterly or monthly in Vietnam?

- Which income of a Vietnamese non-resident is subject to personal income tax?

- What is the Form for declaring a 20% reduction in the VAT rate in Vietnam according to Decree 72?

- What are 3 types of tax explanation form for accountants in Vietnam? What is the penalty for late submission of VAT return in November 2024?

- Vietnam: Compilation of all Appendix 2 forms of Circular 80/2021/TT-BTC