What contents does a taxpayer registration certificate in Vietnam include?

What contents does a taxpayer registration certificate in Vietnam include?

Under Article 34 of Tax Administration Law 2019 regulating the issuance of taxpayer registration certificates:

Issuance of taxpayer registration certificate

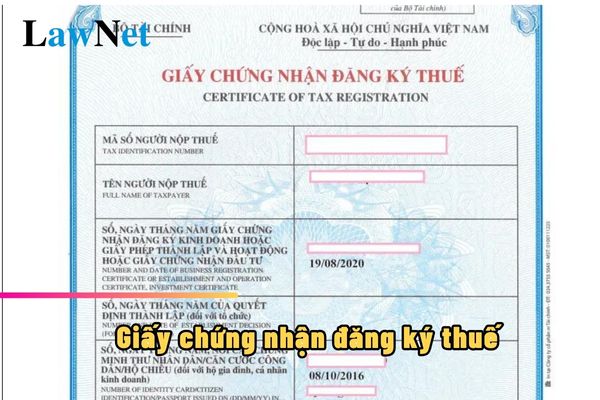

1. Tax authorities shall issue taxpayer registration certificates to taxpayers within 03 working days starting from the date of receipt of taxpayers’ satisfactory taxpayer registration application as prescribed by law. Information on a taxpayer registration certificate shall include:

a) Name of the taxpayer;

b) TIN;

c) Number, date of the business registration certificate or establishment and operation license or investment registration certificate for business organizations and individuals; number, date of the establishment decision for organizations not required to apply for business registration; information of identity card, citizen identification or passport for individuals not subject to business registration;

d) Supervisory tax authority.

2. Tax authorities shall inform TINs to taxpayers instead of taxpayer registration certificates in the following cases:

a) An individual authorizes his/her income payer to apply for taxpayer registration on behalf of the individual and his/her dependants;

b) An individual applies for taxpayer registration through the tax declaration application;

c) An organization or individual applies for taxpayer registration so as to deduct and pay tax on taxpayers’ behalf;

d) An individual applies for taxpayer registration for his/her dependant(s).

3. In case the taxpayer registration certificate or TIN notification is lost or damaged, tax authorities shall reissue it within 02 working days starting from the date of receipt of the satisfactory application from the taxpayer as prescribed by law.

Thus, the taxpayer registration certificate will include the following contents:

- Name of the taxpayer;

- TIN;

- Number, date of the business registration certificate or establishment and operation license or investment registration certificate for business organizations and individuals; number, date of the establishment decision for organizations not required to apply for business registration; information of identity card, citizen identification or passport for individuals not subject to business registration;

- Supervisory tax authority.

What contents does a taxpayer registration certificate in Vietnam include? (Image from the Internet)

Will the taxpayer registration certificate in Vietnam be reissued in case the issued certificate is torn?

Under Clause 3, Article 34 of the Law on Tax Administration 2019, the tax authority shall reissue the taxpayer registration certificate to the taxpayer in the following cases:

- It is lost.

- It is torn or damaged.

- It is burned.

Thus, the taxpayer registration certificate in Vietnam will be reissued in case the issued certificate is torn.

What are the procedures for reissuing a taxpayer registration certificate in case the issued certificate is torn in Vietnam?

Under Sub-item 18, Item 1, Part 2 of the Procedures issued together with Decision 2589/QD-BTC in 2021, the procedures for the first-time taxpayer registration for dependents at the tax authority are detailed as follows:

Step 1.

- When the taxpayer loses, tears, damages, or burns the taxpayer registration certificate, the taxpayer registration certificate for individuals, the TIN notification, or the TIN notification for dependents, they shall send an application for reissuance of the taxpayer registration certificate, the TIN notification to the direct managing tax authority;

- For the case of electronic taxpayer registration application: The taxpayer (NNT) accesses the electronic information portal of their choice to fill out the declaration form and attach the prescribed electronic documents (if any), then electronically sign and send to the tax authority via the electronic information portal of their choice;

The taxpayer submits the application (the taxpayer registration application simultaneously with the business registration application under the one-stop-shop mechanism) to the competent state management authority as prescribed. The competent state management authority shall send the received application information of the taxpayer to the tax authority via the electronic information portal of the General Department of Taxation.

Step 2. Tax authority receives:

- For physical taxpayer registration applications:

+ If the application is submitted directly at the tax authority: The tax official receives and stamps the receipt on the taxpayer registration application, specifying the date of receipt, the number of documents according to the application list in case the taxpayer registration application is submitted directly at the tax authority. The tax official writes a receipt slip detailing the return appointment date and the deadline for processing the received application;

+ If the taxpayer registration application is sent by postal service: The tax official stamps the receipt, writes the date of receipt on the application, and records the reference number of the tax authority;

The tax official checks the taxpayer registration application. If the application is incomplete and needs explanation or supplementation with information or documents, the tax authority shall notify the taxpayer using form No. 01/TB-BSTT-NNT within 02 working days from the date of receiving the application.

- For electronic taxpayer registration applications:

The tax authority shall receive the application via the electronic information portal of the General Department of Taxation, and proceed to check and resolve the application through the tax authority's electronic data processing system:

+ Receiving the application: The electronic information portal of the General Department of Taxation sends a receipt notification of the taxpayer's electronic taxpayer registration application submission to the taxpayer via the electronic information portal chosen by the taxpayer to create and send the application (the General Department of Taxation’s electronic information portal / competent state authority’s electronic information portal or T-VAN service provider) no later than 15 minutes after receiving the taxpayer's electronic taxpayer registration application;

+ Checking and resolving the application: The tax authority shall check and resolve the taxpayer's application under the legal provisions on taxpayer registration and return the result through the electronic information portal chosen by the taxpayer to create and send the application:

++ If the application is complete and meets the prescribed procedures and an outcome is required: The tax authority sends the application resolution result to the electronic information portal chosen by the taxpayer to create and send the application within the deadline;

++ If the application is incomplete and does not meet the prescribed procedures, the tax authority sends a notification of the non-acceptance of the application to the electronic information portal chosen by the taxpayer to create and send the application within 02 working days from the date of the receipt notification.

- When is the deadline for paying tax, duty payment guarantee and tax deposit in Vietnam?

- Are natural aquatic resources exempt from severance tax in Vietnam?

- Are natural swallow's nests subject to severance tax in Vietnam?

- What are the principles for developing a List of goods to be imported free of duty in Vietnam?

- How long is the CIT period of the first year in Vietnam?

- Shall individuals be entitled to tax refund if their taxed incomes do not reach a tax-liable level in Vietnam?

- What are regulations on responsibilities of income payer regarding PIT refund when being delegated to settle tax in Vietnam?

- Is it necessary to terminate the tax identification number when a business temporarily suspends its operations in Vietnam?

- What is the value-added tax declaration form for 2024 in Vietnam?

- What are forms for declaring corporate income tax in Vietnam?