Vietnam: How to fill out Section 1 of the VAT reduction appendix according to Resolution 142 on HTKK?

Vietnam: How to fill out Section 1 of the VAT reduction appendix according to Resolution 142 on HTKK?

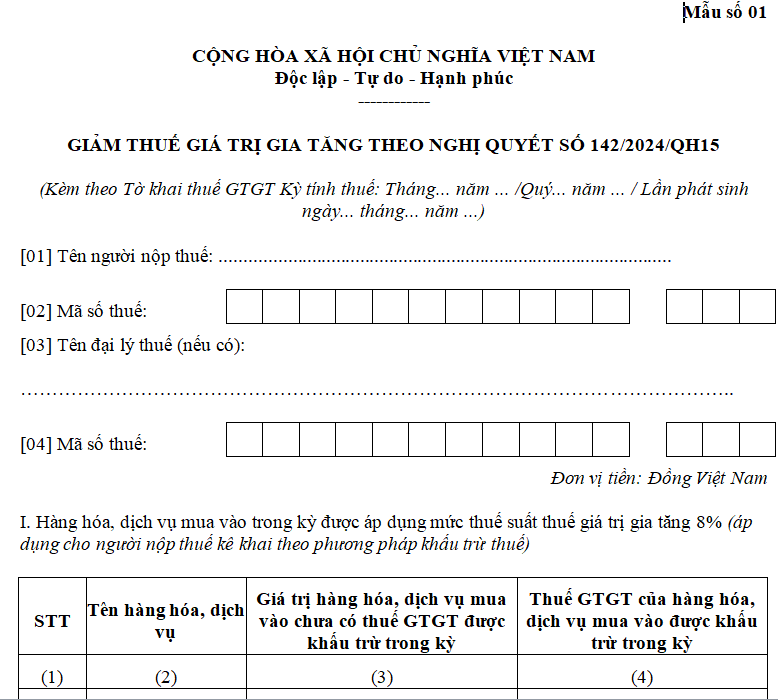

The appendix form for VAT reduction according to Resolution 142/2024/QH15 on HTKK software version 5.2.3 consists of three sections. The method to fill out Section 1 for purchased goods or services at a tax rate of 8% (applies to taxpayers declaring under the input tax deduction method) is as follows:

- Name of goods, services (2): Enter the name of the goods or services purchased during the period to which a VAT rate of 8% applies.

- Value of goods, services purchased before deducted VAT during the period (3): Enter the value of goods or services purchased excluding deductible VAT during the period.

- VAT of goods, services purchased deductible during the period (4): After entering the information of goods, services for which the tax is reduced and the pre-tax price in columns (2) and (3), the HTKK software will automatically calculate the VAT amount at a rate of 8% in column (4).

Vietnam: How to fill out Section 1 of the VAT reduction appendix according to Resolution 142 on HTKK? (Image from the Internet)

What is the VAT reduction appendix form in Vietnam according to Resolution 142?

The VAT reduction appendix form according to Resolution 142/2024/QH15 on HTKK Software is the VAT reduction appendix stipulated in Appendix IV issued with Decree 72/2024/ND-CP:

Download the VAT reduction appendix form according to Resolution 142/2024/QH15

Which goods and services are not eligible for VAT reduction in Vietnam in 2024?

Article 1 of Decree 72/2024/ND-CP applies VAT reduction for goods and service groups currently subject to a 10% tax rate, excluding the following:

- Telecommunications, financial services, banking, securities, insurance, real estate business, metals and fabricated metal products, mining products (except coal mining), coke, refined petroleum, chemical products.

Details in Appendix I issued with Decree 72/2024/ND-CP

- Goods and services subject to special consumption tax.

Details in Appendix II issued with Decree 72/2024/ND-CP

- Information technology according to the law on information technology.

Details in Appendix III issued with Decree 72/2024/ND-CP

- The VAT reduction for each type of goods and services specified in Clause 1, Article 1 of Decree 72/2024/ND-CP is uniformly applied at different stages such as import, production, processing, and commercial business. For extracted coal products (including the case where extracted coal is screened, classified by a closed process before selling), the VAT reduction applies. Coal products listed in Appendix I issued with Decree 72/2024/ND-CP, at stages other than extraction for sale, are not eligible for VAT reduction.

General enterprises and economic groups implementing a closed process for products prior to sale are also eligible for VAT reduction for extracted coal products sold.

In the case that goods and services listed in Appendices I, II, and III issued with Decree 72/2024/ND-CP are either subject to 0% VAT or 5% VAT according to the Law on Value-Added Tax, then the provisions of the Law on Value-Added Tax apply, and VAT reduction is not provided.

When does the VAT reduction according to Decree 72 apply?

According to Clause 1, Article 2 of Decree 72/2024/ND-CP:

Effective date and implementation

1. This Decree takes effect from July 1, 2024, until the end of December 31, 2024.

2. Ministries, based on their functions, tasks, and the People's Committees of provinces and centrally-affiliated cities, shall direct relevant agencies to implement propaganda, guidance, inspection, and supervision so that consumers understand and benefit from the VAT reduction stipulated in Article 1 of this Decree, focusing on stabilizing supply and demand for goods and services subject to VAT reduction to maintain price stability in the market (prices excluding VAT) from July 1, 2024, to December 31, 2024.

3. If difficulties arise during implementation, the Ministry of Finance will issue instructions and resolutions.

4. Ministers, Heads of ministerial-level agencies, Heads of agencies under the Government of Vietnam, Chairpersons of the People's Committees of provinces and centrally-affiliated cities, and relevant enterprises, organizations, and individuals are responsible for implementing this Decree.

Decree 72/2024/ND-CP is effective from July 1, 2024, to December 31, 2024.

This also means that the VAT reduction to 8% only applies until the end of December 31, 2024.

From January 1, 2025, the VAT rate for goods and services previously reduced will revert to 10% (unless otherwise regulated by new legislation).

- What is the currency unit used in tax accounting in Vietnam?

- Which enterprise groups will the General Department of Taxation of Vietnam focus on inspecting and auditing in 2025?

- What are guidelines on online submission of unemployment benefits application in Vietnam in 2025? Are unemployment benefits subject to personal income tax?

- How long can the tax audit period on taxpayers’ premises in Vietnam be extended for complex matters?

- From January 1, 2025, which entities are exempted from ferry service fees from the state budget in Vietnam?

- How to determine VAT applicable to ships sold to foreign organizations in Vietnam?

- What is the maximum penalty for late submission of tax declaration dossiers in Vietnam?

- What is the duty-free allowance on gifts given for humanitarian in Vietnam?

- Are votive papers subject to excise tax up to 70% in Vietnam?

- Shall enterprises use invoices during suspension of operations in Vietnam?