What is the spreadsheet template and amortization of fixed assets in Vietnam in 2023? What are the content of the spreadsheet and the amortization of fixed assets?

What is the principle of depreciation for fixed assets in Vietnam?

Pursuant to Article 9 of Circular 45/2013/TT-BTC (added by Clause 4 and Article 1 of Circular 147/2016/TT-BTC and corrected by Article 1 of Decision 1173/QD-BTC in 2013), the principle of depreciation of fixed assets is as follows:

(1) All existing fixed assets of the enterprise must be depreciated, except for the following fixed assets:

- Fixed assets have been fully depreciated but are still being used in production and business activities.

- Depreciated fixed assets have not been completely lost.

- Other fixed assets managed by the enterprise but not under the ownership of the enterprise (except financial lease fixed assets)

- Fixed assets are not managed, monitored, or recorded in the accounting books of the enterprise.

- Fixed assets used in welfare activities to serve employees of the enterprise (except fixed assets serving employees working at the enterprise, such as motels between shifts, cafeterias between shifts, changing houses, etc.) toilets, clean water tanks, garages, rooms or medical stations for medical examination and treatment, shuttles for workers, training and vocational training establishments, and housing for workers (built by enterprises).

- Fixed assets from non-refundable aid after being handed over to enterprises by competent authorities for scientific research

- Intangible fixed assets are long-term land use rights acquired through land use levy collection or lawful long-term land use rights transfers.

- Class 6 fixed assets specified in Clause 2 and Article 1 of Circular 45/2013/TT-BTC are not required to depreciate; only detailed books are opened to monitor the annual depreciation value of each asset and are not subject to depreciation. recorded as a decrease in capital to form assets.

(2) Depreciation expenses of fixed assets, which are included in reasonable expenses when calculating corporate income tax, comply with the provisions of legal documents on corporate income tax.

(3) In case the fixed assets used in welfare activities serving employees of the enterprise specified in Clause 1 of Article 9 of Circular 45/2013/TT-BTC are involved in production and business activities, the enterprise shall, based on the time and nature of using these fixed assets, calculate and depreciate the business expenses of the enterprise and notify the tax authority directly managing it for monitoring and management.

(4) Fixed assets that have not been fully depreciated are lost or damaged but cannot be repaired or remedied. The enterprise determines the cause and compensation liability of the collective or individual.

The difference between the residual value of the property and the compensation caused by the organization or individual, the compensation amount of the insurance agency, and the recovered value (if any), is offset by the enterprise using the financial reserve fund.

If the financial reserve fund is not enough to make up for it, the difference between the company and the enterprise shall be included in the reasonable expenses of the enterprise when determining corporate income tax.

(5) Enterprises leasing operating fixed assets must depreciate the leased fixed assets.

(6) Enterprises that lease fixed assets in the form of financial leases (referred to as "financial lease fixed assets" for short) must depreciate the leased fixed assets like fixed assets owned by the enterprise according to current regulations.

In the event that, at the beginning of the lease, the lessee commits not to repurchase the leased asset as stipulated in the finance lease contract, the lessee is entitled to depreciate the fixed asset according to the terms of the lease contract. lease in the contract.

(7) In cases of re-evaluating the value of fixed assets that have been depreciated for capital contribution or transfer upon separation, consolidation, or merger, these fixed assets must be valued by professional valuation organizations but not at a level below 20% of the original cost of the asset.

Depreciation time for these assets is the time when the enterprise officially receives the property to put it into use, and the depreciation period is from 3 to 5 years. The specific time is decided by the enterprise, which must notify the tax authority before implementation.

For equitized enterprises, the time to depreciate the above-mentioned fixed assets is the time when the enterprise is granted a business registration certificate and converts it into a joint stock company.

(8) For enterprises with 100% state capital, when determining the value of enterprises for equitization using the discounted cash flow (DCF) method, the increased difference of state capital between the actual value and the recorded value in the accounting books is not recorded as intangible fixed assets and is gradually amortized to production and business expenses during the period but for a period not exceeding 10 years.

The time to begin allocating to expenses is the time when the enterprise officially transforms into a joint stock company (with a business registration certificate).

(9) The deduction or cessation of depreciation of fixed assets is made from the date (according to the number of days of the month) on which the fixed asset increases or decreases. Enterprises shall record the increase and decrease of fixed assets according to current regulations on enterprise accounting.

(10) For capital construction works that have been completed and put into use, the enterprise has recorded an increase in fixed assets at the provisional price because the final settlement has not been made. When the settlement of completed capital construction works has a difference between the provisional value and the settlement value, the enterprise must adjust the historical cost of the fixed assets according to the settlement value already approved by the competent authority.

Enterprises do not have to adjust the level of depreciation expense deducted from the time the fixed asset is completed, handed over, and put into use until the time of settlement is approved.

Depreciation expense after the time of settlement is determined on the basis of subtracting (-) the value of the approved fixed asset settlement from the amount depreciated until the time of approving the settlement of fixed assets and dividing (: ) the remaining amortization period of fixed assets as prescribed.

(11) For fixed assets that enterprises are monitoring, managing, and depreciating according to Circular 203/2009/TT-BTC but which do not meet the criteria for historical cost of fixed assets as prescribed in Article 2 of this Circular, the residual value of these assets shall be allocated to the enterprise's production and business expenses, and the allocation period shall not exceed 3 years from the effective date of this Circular.

What is the spreadsheet template and amortization of fixed assets in Vietnam in 2023? What are the content of the spreadsheet and the amortization of fixed assets? (Image from the Internet)

What is the spreadsheet template and amortization of fixed assets in Vietnam in 2023?

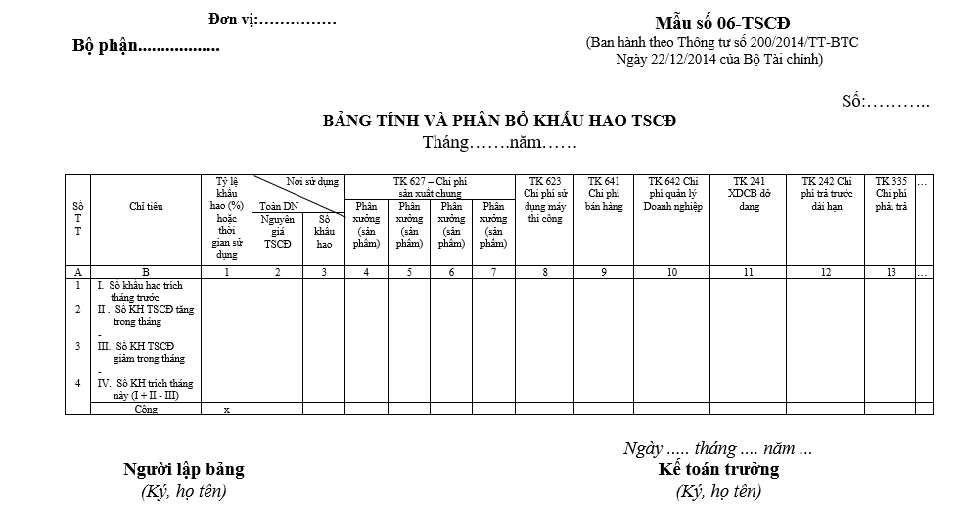

Pursuant to Form No. 06—Fixed Assets in Appendix 3 issued together with Circular 200/2014/TT-BTC, which stipulates the spreadsheet form and amortization of fixed assets in 2023 as follows:

Download the 2023 spreadsheet template and amortization of fixed assets by clicking here.

What are the content of the spreadsheet and the amortization of fixed assets in Vietnam?

According to the note form No. 06-TSCD Appendix 3 issued together with Circular 200/2014/TT-BTC, as follows:

- Purpose:

Used to record the depreciation of fixed assets to be deducted and allocate such depreciation amounts to users of fixed assets on a monthly basis.

- Main structure and content

The spreadsheet and amortization of fixed assets have vertical columns reflecting the depreciation amount to be calculated for each user of the fixed asset (such as for the production department, Accounts 623, 627, and for the sales department, Account 641, for the department). management department (Account 642) and the horizontal rows reflect the depreciation amount calculated in the previous month, the amount of depreciation that increased or decreased, and the amount of depreciation to be calculated in this month.

- Establishment basis:

+ The depreciation line calculated for the previous month is taken from the spreadsheet and amortized the previous month's fixed assets.

+ Lines of increase and decrease in depreciation of fixed assets this month are reflected in detail for each fixed asset related to the increase and decrease in depreciation of fixed assets according to current regulations on depreciation of fixed assets.

The line of depreciation payable for this month is calculated by (=). Depreciation amount calculated in the previous month plus (+) With the amount of depreciation increasing, minus (-) The depreciation amount decreased in the month.

This month's depreciation amount on the fixed asset depreciation allocation table is used to record in the relevant statements, journals, documents, and accounting books (the credit column to Account 214) and is also used to determine the actual cost of finished products and services.

LawNet