What is the PIT finalization declaration form in Vietnam for individuals to declare tax finalization by themselves?

- Vietnam: What is the PIT finalization declaration dossier for individuals to declare tax finalization by themselves with respect to incomes from salaries and wages?

- What is the PIT finalization declaration form in Vietnam for individuals to declare tax finalization by themselves?

- When is an individual earning income from wages and salaries not required to finalize personal income tax in Vietnam?

Vietnam: What is the PIT finalization declaration dossier for individuals to declare tax finalization by themselves with respect to incomes from salaries and wages?

Pursuant to subsection 9.2, Section 2, Appendix I promulgated together with Decree 126/2020/ND-CP, for individuals who declare personal income tax directly with tax authorities, the income tax finalization dossier for individuals includes:

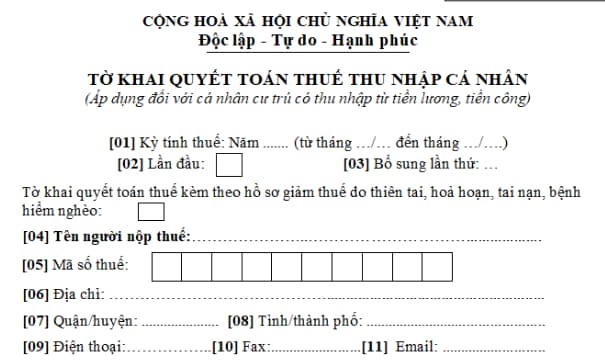

- Personal income tax finalization declaration form No. 02/QTT-TNCN issued together with Appendix II of Circular 80/2021/TT-BTC

- Appendix to the list of family circumstance-based deductions for dependents, Form No. 02-1, BK-QTT-TNCN issued together with Appendix II of Circular 80/2021/TT-BTC

- Copies (photocopies from the original) of documents proving the tax amount deducted, temporarily paid in the year, and tax paid abroad (if any). In case the income-paying organization fails to issue tax withholding documents to individuals because it has ceased to operate, the tax authority shall base its decision on the tax branch's database to consider and process the final settlement dossier. tax for individuals without the required tax withholding documents.

In cases where an organization or individual pays income using an electronic PIT withholding document, the taxpayer shall use a copy of the electronic PIT withholding document (the paper copy is converted from the taxpayer's self-printed form). original electronic PIT withholding documents sent to taxpayers by income-paying organizations and individuals).

- Copies of the tax withholding certificate (specifying which income tax declaration has been paid) issued by the income-paying agency or a copy of the bank statement for the tax amount paid abroad, certified by the taxpayer. taxpayers in cases where, according to the provisions of foreign laws, the foreign tax offices do not issue certificates of paid tax amounts.

- Copies of invoices and vouchers evidencing contributions to charity funds, humanitarian funds, and study promotion funds (if any).

- Documents proving the amount paid by the unit or organization paying income abroad in case the individual receives income from international organizations, embassies, or consulates and receives income from foreign countries. outside.

- Dossier for registration of dependents (if deduction is calculated for dependents at the time of tax finalization for dependents who have not yet registered dependents).

What is the PIT finalization declaration form in Vietnam for individuals to declare tax finalization by themselves?

What is the PIT finalization declaration form in Vietnam for individuals to declare tax finalization by themselves?

Currently, the form of personal income tax finalization declaration for individuals earning income from wages is Form 02/QTT-TNCN issued together with Circular 80/2021/TT-BTC as follows:

Download the personal income tax finalization form for individuals earning wages here.

When is an individual earning income from wages and salaries not required to finalize personal income tax in Vietnam?

Pursuant to Item d.3 Point d. of Clause 6 of Article 8 of Decree 126/2020/ND-CP, if it falls into one of the following cases, it is not required to finalize personal income tax:

- Individuals whose personal income tax amount to pay more after the final settlement of each year is 50,000 VND or less

- Individuals whose personal income tax payable is less than the temporarily paid tax amount without requesting a tax refund or an offset in the next tax return period;

- Individuals earning incomes from salaries and wages who sign labor contracts for 3 months or more at a unit and at the same time have an average monthly income of not more than VND 10 million in other places in the year may withhold personal income tax at the rate of 10% if there is no request and no tax finalization is required for this income;

- Individuals whose employer buys life insurance (except voluntary retirement insurance) or other optional insurance with accumulated premiums that the employer or insurance enterprise has deducted. deduction of PIT at the rate of 10% on the premium amount corresponding to the part purchased or contributed by the employer to the employee.

LawNet