What is the latest form of notice of invoice destruction result in Vietnam? What are the penalties for destroying invoices after expiry of the regulated time limit?

What is the latest form of notice of invoice destruction result in Vietnam?

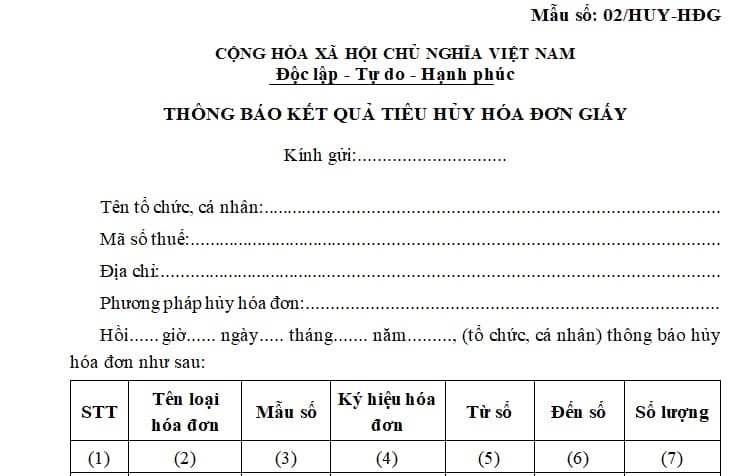

Form No. 02/HUY-HDG of Annex IA issued together with Decree 123/2020/ND-CP. Below is a sample image of the notice of invoice destruction result:

Download the notice of invoice destruction result: Here.

What is the latest form of notice of invoice destruction result in Vietnam? What are the penalties for destroying invoices after expiry of the regulated time limit? (Image from the Internet)

What are the dossiers for destruction of tax authority-ordered printed invoices in Vietnam?

Pursuant to Point b, Clause 2, Article 27 of Decree 123/2020/ND-CP stipulates as follows:

Destruction of tax authority-ordered printed invoices

1. Enterprises, business entities, household or individual businesses shall destroy their unused invoices. Invoices must be destroyed within 30 days from the date on which the destruction is notified to the tax authority. If an invoice is expired according to the tax authority’s notice (in case of enforcement of payment of tax debts), the relevant enterprise, business entity, household or individual business shall carry out the destruction of invoice within 10 days from the date of the tax authority’s notice or the date on which the lost invoice is found.

Invoices issued by accounting units shall be destroyed in accordance with regulations of the Law on accounting.

Invoices which are not yet issued but are exhibits of lawsuit cases shall not be destroyed and must be handled in accordance with regulations of laws.

2. Invoices of enterprises, business entities, household or individual businesses shall be destroyed as follows:

a) The enterprise, business entity, household or individual business shall make the list of invoices to be destroyed.

b) The enterprise or business entity shall establish an invoice destruction council. The invoice destruction council is comprised of senior representatives and representatives of accounting department. The household or individual business is not required to establish an invoice destruction council.

c) The invoice destruction record shall bear signatures of members of the invoice destruction council who shall assume legal liability for any mistakes thereof.

d) Invoice destruction dossier includes:

- The decision on establishment of the invoice destruction council, except household or individual businesses;

- The list of invoices to be destroyed, including: Name, form number and reference number of the invoice, number of destroyed invoices (from number….to number…., or number of each invoice if the invoice numbers are not continuous);

- The invoice destruction record;

- The notice of invoice destruction result includes: type, reference number and quantity of destroyed invoice, from number…..to number….., reasons, date and time, and method of destruction, using Form No. 02/HUY-HDG in Appendix IA enclosed herewith.

The invoice destruction dossier shall be kept by the enterprise, business entity, household or individual business using invoices. The notice of invoice destruction result is made into 02 copies of which one copy is kept on file, and the other is sent to the supervisory tax authority within 05 working days from the date of invoice destruction.

3. Destruction of invoices by tax authorities

a) Tax authorities shall take charge of destroying invoices which are printed according to orders of a Provincial Department of Taxation, are not sold or issued but are no longer used.

b) The General Department of Taxation shall promulgate procedures for destruction of invoices printed according to orders of Provincial Departments of Taxation.

Thus, according to the provisions on the invoice destruction dossier, there are:

- The decision on establishment of the invoice destruction council, except household or individual businesses;

- The list of invoices to be destroyed, including: Name, form number and reference number of the invoice, number of destroyed invoices (from number….to number…., or number of each invoice if the invoice numbers are not continuous);

- The invoice destruction record;

- The notice of invoice destruction result includes: type, reference number and quantity of destroyed invoice, from number…..to number….., reasons, date and time, and method of destruction, using Form No. 02/HUY-HDG in Appendix IA enclosed herewith.

Vietnam: What are the penalties for destroying invoices after expiry of the regulated time limit?

Pursuant to Article c, clause 2, point a, clause 3, Article 27 of Decree 125/2020/ND-CP stipulates as follows:

Penalties for violations against regulations on cancellation, destruction or elimination of invoices

1. Penalties in the form of cautions shall be imposed for the act of cancelling or destroying invoices from 1 to 5 days after expiry of the regulated time limit under mitigating circumstances.

2. Fines ranging from VND 2,000,000 to VND 4,000,000 shall be imposed for one of the following violations:

a) Cancelling invoices released but not issued, or invalidated invoices, in breach of regulations.

b) Failing to cancel invoices released but not issued yet, or invalidated invoices, or failing to cancel invoices purchased from tax authorities but expired;

c) Cancelling or destroying invoices from 1 to 10 working days after expiry of the regulated time limit, except the case prescribed in clause 1 of this Article.

3. Fines ranging from VND 4,000,000 to VND 8,000,000 shall be imposed for one of the following violations:

a) Cancelling or destroying invoices at least 11 working days after expiry of the regulated time limit;

b) Failing to cancel or destroy invoices in accordance with laws;

c) Failing to cancel e-invoices containing defects after being issued after expiry of the time limit for tax authorities’ issuing notification of these defects to sellers;

d) Failing to cancel externally ordered invoices not released yet but no longer used according to regulations;

dd) Cancelling or destroying invoices in breach of procedures or processes prescribed by laws;

e) Destroying invoices though these invoices are not classified as those subject to destruction under laws.

4. Remedies: Compelling the cancellation or destruction of invoices with respect to the acts specified in point b of clause 2, point b, c and d of clause 3 of this Article.

Thus, according to the above provisions, destroying invoices after expiry of the regulated time limit can be fined up to 16,000,000 VND (according to Clause 5, Article 5 of Decree 125/2020/ND-CP, this is the penalty for individuals if organizations violate penalty will be doubled).

In addition, the form of warning is only applied to act of cancelling or destroying invoices from 1 to 5 days after expiry of the regulated time limit under mitigating circumstances.

LawNet