What is the latest audit report form for financial disposition at the time of official transformation into a joint-stock company in Vietnam?

- What is the latest audit form for financial disposition at the time of official transformation into a joint-stock company in Vietnam?

- What are the contents of the audit report form for financial disposition at the time of official transformation into a joint-stock company in Vietnam?

- What are the regulations on financial disposition at the time of official transformation into a joint-stock company in Vietnam?

What is the latest audit form for financial disposition at the time of official transformation into a joint-stock company in Vietnam?

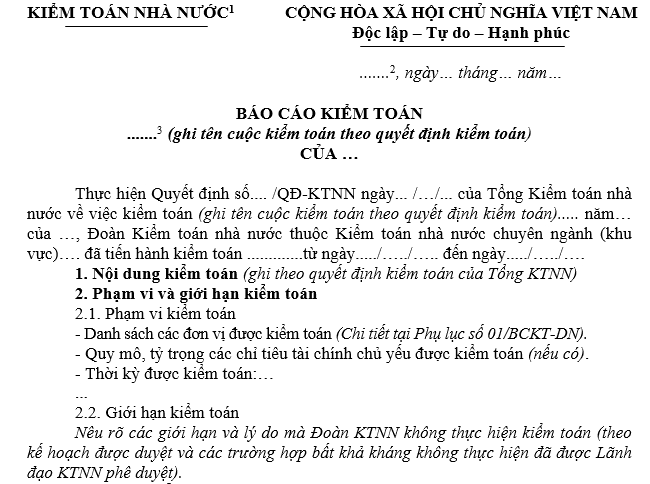

The latest audit form for financial disposition at the time of official transformation into a joint-stock company is the Form No. 04/BCKT-DN Table of contents issued together with Decision 01/2023/ QD-KTNN.

Download the latest audit form for financial disposition at the time of official transformation into a joint-stock company here.

What is the latest audit form for financial disposition at the time of official transformation into a joint-stock company in Vietnam? (Image from the Internet)

What are the contents of the audit report form for financial disposition at the time of official transformation into a joint-stock company in Vietnam?

Pursuant to the contents of Form No. 04/BCKT-DN Table of Contents issued together with Decision 01/2023/ QD-KTNN.

The specific content of the report includes the following two parts:

(1) Audit situation and results:

- Feature situation

+ Overview of the economic and social situation;

+ The change of policy mechanism during the audit year;

+ Factors that have great influence on the management and administration activities of the audited unit.

- Audit results

+ Auditing financial indicators at the time of official transformation into a joint stock company;

+ Auditing the financial handling and finalization of state capital at the time of official transformation into a joint stock company;

+ Evaluate, confirm and conclude on the compliance with laws, policies and accounting regimes; financial handling and finalization of state capital at the time of official transformation into a joint stock company;

+ Emphasis and other issues (if any);

(2) Audit recommendations:

- For audited units.

- For relevant ministries and branches… (if any).

- For the Prime Minister, the Government, the National Assembly... (if any).

What are the regulations on financial disposition at the time of official transformation into a joint-stock company in Vietnam?

Pursuant to the provisions of Article 8 of Circular 46/2021/TT-BTC, the financial disposition at the time of official transformation into a joint-stock company is regulated as follows:

- Each equitized enterprise shall continue to comply with regulations on financial management

- Excess or deficient asset value compared with the value of the equitized enterprise decided and announced by the owner's representative agency shall be handled according to the provisions.

- The equitized enterprise shall treat receivables and payables determined at the time they are granted the certificate of initial registration of the joint-stock company.

- The equitized enterprise shall manage and use reward and welfare fund arising from the time of business valuation to the time when the equitized enterprise is granted the certificate of initial registration of the joint-stock company in accordance with regulations.

- For any exchange rate difference arising due to revaluation of items of foreign currency origin at the time of being official transformed into a joint stock company.

- In case where stock dividends arises after the time of business valuation and by or before the time of official transformation into a joint stock company

In case where, at the time of official transformation to a joint stock company, the aforesaid dividend distribution Resolution is not available, the equitized enterprise shall direct the representative for their ownership interest to request the capital contribution transferee to issue a profit distribution Resolution (in the case of having controlling shares at the transferee) or request the joint stock company to give clear explanation.

At the time of officially being transformed into a joint stock company, the equitized enterprise shall use risk provisions to deal with the loss of intercorporate financial investments qualified for such provisions

- After being granted the certificate of initial registration of the joint-stock company, the joint-stock company shall be responsible for fulfilling the financial obligations and completing regulatory procedures to be allocated land, rent land or granted a certificate of the right to use land, own the house and other land-attached property in accordance with the provisions of the current land law and legislation on tax administration.

- Time limits for a tax authority’s completion of finalization of taxes and other payables to the state budget of equitized enterprises after being granted the certificate of initial registration of the joint-stock company shall be subject to the Law on Tax Administration.

Decision 01/2023/ QD-KTNN will officially take effect from February 25, 2023.

LawNet