What is the latest application form for TIN deactivation? What is the application for TIN deactivation in Vietnam?

What is the latest application form for TIN deactivation in Vietnam?

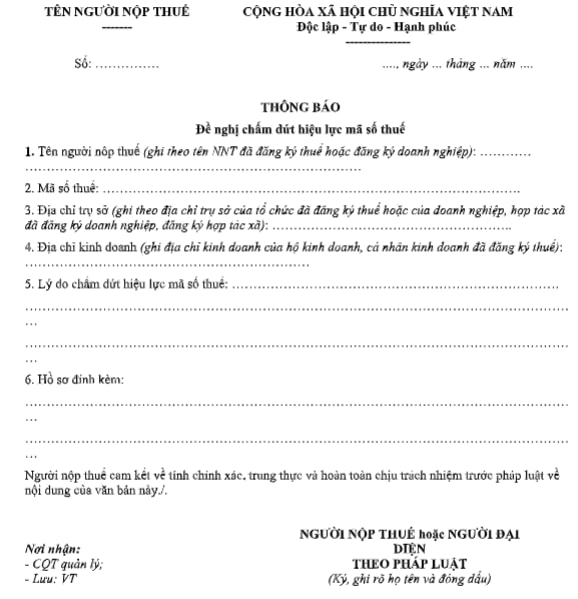

Currently, the latest application form for TIN deactivation is form No. 24/DK-TCT - Application for TIN deactivation issued with Circular 105/2020/TT-BTC according to the provisions of Article 38 and Article 39 of the Law on Tax Administration 2019.

Download form No. 24/DK-TCT - Application for TIN deactivation: download

What is the latest application form for TIN deactivation? What is the application for TIN deactivation in Vietnam?

What is the latest application for TIN deactivation in Vietnam?

Pursuant to Article 14 of Circular 105/2020/TT-BTC regulating application for TIN deactivation for taxpayer applying for tax registration directly with the tax authority are:

- Application for TIN deactivation is form No. 24/DK-TCT - Application for TIN deactivation issued with Circular 105/2020/TT-BTC according to the provisions of Article 38 and Article 39 of the Law on Tax Administration 2019.; download

- Other documents (if any):

+ For For the household/individual business; place of business of household/individual business as prescribed in Point i, Clause 2, Article 4 of Circular 105/2020/TT-BTC, application includes:

Copy of decision on revocation of certificate of household business registration (if any).

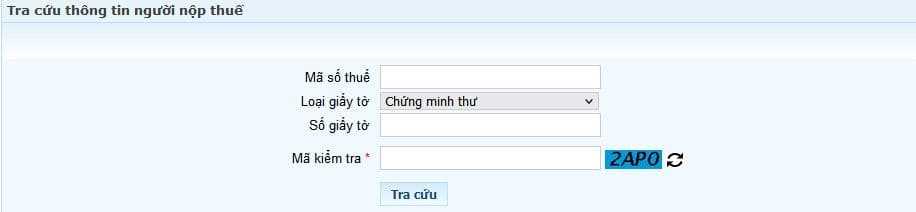

What are the instructions for looking up TIN in Vietnam?

Individuals can look up their TIN through the following two methods:

Method 1: Look up TIN through website http://tracuunnt.gdt.gov.vn/tcnnt/mstcn.jsp

Step 1: Taxpayers access the website http://tracuunnt.gdt.gov.vn/tcnnt/mstcn.jsp

Step 2: Taxpayers select the "Information about personal income tax payers" section.

Step 3: The taxpayer enters the ID card number or ID card as required

Step 4: The taxpayer enters the confirmation code and selects "Look Up" to see the results.

Method 2: Look up TIN through website https://thuedientu.gdt.gov.vn/

Step 1: Visit the website: https://thuedientu.gdt.gov.vn/

Step 2: Select the "Individual" box

Step 3: Select LOOK UP INFORMATION OF TAXPAYER

Step 4: Enter your ID card number or citizen identification card and receive the OTP code

Step 5: Select Lookup and view the information displayed

What are the regulations on TIN issuance in Vietnam?

Pursuant to the provisions of Clause 3, Article 30 of the Law on Tax Administration 2019, the following content is stipulated:

Applying for taxpayer registration and TIN issuance

...

3. Issuance of TINs:

a) Each enterprise, business organization or other organization is issued with 01 unique TIN to use throughout its entire operation, from the date of taxpayer registration to the date of TIN deactivation. A taxpayer’s branches, representative offices and/or dependent units that pay their own tax shall be issued with separate TINs. In case an enterprise, organization, branch, representative office or dependent unit combines taxpayer registration via the interlinked single-window system with business registration, the number of the certificate of enterprise registration, cooperative registration and/or business registration (hereinafter referred to as “business registration certificate”) is also the TIN;

b) Each individual is issued 01 unique TIN to use throughout their whole life. Any dependant of that individual shall be issued with a TIN for the purpose of claiming personal exemption for personal income taxpayers. The TIN issued to the dependant is also his/her personal TIN, which is used when paying his/her tax;

c) Enterprises, organizations and individuals responsible for deducting and paying tax on behalf of taxpayers shall be issued with separate TINs for use when deducting tax;

d) Issued TINs shall not be reissued to another taxpayer;

dd) TINs of enterprises, business organizations and other organizations shall remain unchanged after they are converted, sold, gifted or inherited;

e) TIN issued to a household, household business or individual business is issued to the individual representing the household, household business or individual business.

Accordingly, the issuance of TINs is regulated as follows:

(1) For enterprises, business organizations or other organizations:

- Each enterprise, business organization or other organization is issued with 01 unique TIN to use throughout its entire operation, from the date of taxpayer registration to the date of TIN deactivation.

- A taxpayer’s branches, representative offices and/or dependent units that pay their own tax shall be issued with separate TINs.

- In case an enterprise, organization, branch, representative office or dependent unit combines taxpayer registration via the interlinked single-window system with business registration, the number of the certificate of enterprise registration, cooperative registration and/or business registration (hereinafter referred to as “business registration certificate”) is also the TIN;

(2) For individuals:

- Each individual is issued 01 unique TIN to use throughout their whole life.

- Any dependant of that individual shall be issued with a TIN for the purpose of claiming personal exemption for personal income taxpayers.

- The TIN issued to the dependant is also his/her personal TIN, which is used when paying his/her tax;

LawNet