What is the form of payment statement according to Circular 200 and Circular 133 for enterprises in Vietnam?

- What is the form of payment statement and instructions on how to record according to Circular 200 for enterprises in Vietnam?

- What is the form of payment statement and how to record it according to Circular 133 for small and medium enterprises in Vietnam?

- How many years should the statements used directly for accounting books be retained?

What is the form of payment statement and instructions on how to record according to Circular 200 for enterprises in Vietnam?

Currently, the form of payment statement according to Circular 200 for enterprises is specified in Form 09-TT issued together with Circular No. 200/2014/TT-BTC specifically as follows:

Download the form of payment statement according to Circular 200 for enterprises: Click here.

Guidance on methods and responsibilities for recording payment statements according to Circular 200:

- In the upper left corner write the name of the unit. The first part clearly states the full name, department, and address of the payer and clearly states what the spending is for.

- Columns A, B, C, D specify the ordinal number, serial number, date and month of the voucher and explain the spending content of each voucher.

Column 1: Enter the amount.

- The payment statement must clearly state the total amount in words and numbers of the original documents attached.

- The payment statement is made in 2 copies:

+ 1 copy is kept at the cashier.

+ 1 copy is kept in the fund accountant.

What is the form of payment statement according to Circular 200 and Circular 133 for enterprises in Vietnam?

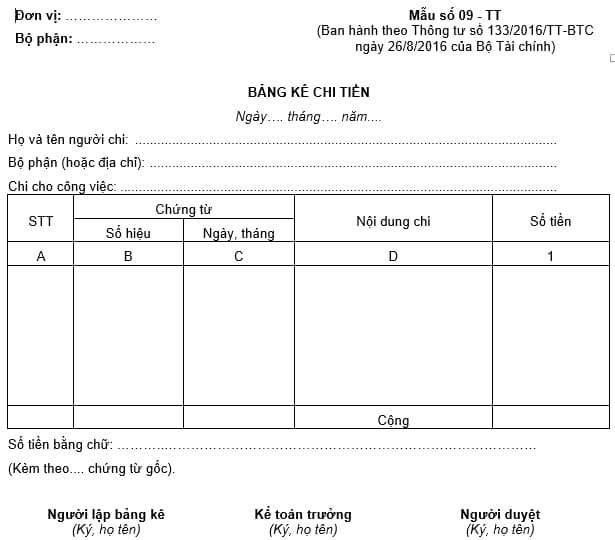

What is the form of payment statement and how to record it according to Circular 133 for small and medium enterprises in Vietnam?

Currently, the form of payment statement and the method of recording according to Circular 133 for small and medium enterprises is specified in Form No. 09-TT issued together with Circular No. 133/2016/TT-BTC, specifically as follows:

Download the form of payment statement and how to record according to Circular 133 for small and medium enterprises in Vietnam: Click here.

Guidance on methods and responsibilities for recording payment statements according to Circular 133:

- In the upper left corner write the name of the unit. The first part clearly states the full name, department, and address of the payer and clearly states what the spending is for.

- Columns A, B, C, D specify the ordinal number, number, date and month of the voucher and explain the spending content of each voucher.

- Column 1: Enter the amount.

- The payment statement must clearly state the total amount in words and numbers of the original documents attached.

- The payment statement is made in 2 copies:

+ 1 copy is kept at the cashier.

+ 1 copy is kept in the fund accountant.

How many years should the statements used directly for accounting books be retained?

Pursuant to Article 13 of Decree No. 174/2016/ND-CP stipulating:

Accounting documents to be retained for at least 10 years

The following accounting documents have to be retained for at least 10 years:

1. Accounting records directly recorded in accounting books and financial statements, statements, detailed accounting books, general accounting books, monthly, quarterly and annual financial statements, annual statements, internal audit reports, accounting document destruction records and other documents directly recorded in accounting books and financial statements.

2. Accounting documents related to liquidation or transfer of fixed assets; reports on stocktaking and asset valuation.

3. Accounting documents of investors, including annual accounting documents and terminal statements of completed Group B and Group C projects.

4. Accounting documents related to establishment, division, consolidation, merger, conversion of the enterprise, dissolution, bankruptcy, shutdown or termination of a project.

5. Relevant documents such as audit documents issued by State Audit Office of Vietnam, inspection documents issued by competent authorities or documents of independent audit organizations.

6. Documents other than those specified in Article 12 and Article 14 hereof.

7. In the cases where other laws prescribe that the documents specified in Clause 1 through 6 of this Article have to be retained for more than 10 years, such law shall apply.

Thus, the statements used directly for accounting books must be retained for at least 10 years.

LawNet