What is the form of environment protection tax declaration? What are the subjects of environmental protection tax in Vietnam?

- What is the form of environment protection tax declaration in Vietnam?

- What are the subjects of environmental protection tax in Vietnam?

- What is the regulation on taxable time in Vietnam?

- When will the environmental protection taxpayer be paid tax refund in Vietnam?

- What are the regulations on the performance of tax declaration, tax calculation and tax payment in Vietnam?

What is the form of environment protection tax declaration in Vietnam?

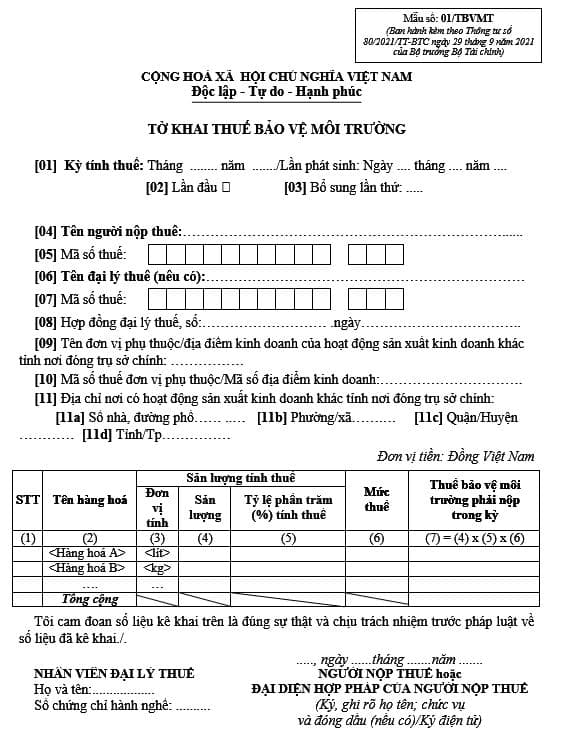

The form of environment protection tax declaration is Form 01/TBVMT issued together with Circular 80/2021/TT-BTC, below is the form of environment protection tax declaration as follows:

Download the form of environment protection tax declaration 2023: Here.

What is the form of environment protection tax declaration? What are the subjects of environmental protection tax in Vietnam? (Image from the Internet)

What are the subjects of environmental protection tax in Vietnam?

Pursuant to Article 3 of the Law on Environmental Protection Tax 2010, there are 09 groups of subject to environmental protection tax:

- Gasoline, oil, grease, including:

+ Gasoline, except ethanol;

+ aircraft fuel;

+ diesel oil;

+ Petroleum;

+ Fuel oil;

+ lubricants;

+ Grease.

- Coal, including:

+ Lignite;

+ Anthracite Coal (anthracite);

+ Fat coal;

+ Other coal.

- Hydrogen-chlorofluorocarbon liquid (HCFC).

- Taxable-plastic bag.

- Herbicide which is restricted from use.

- Pesticide which is restricted from use.

- Forest product preservative which is restricted from use.

- Warehouse disinfectant which is restricted from use.

- When it is necessary to supplement other taxable objects as per period, the National Assembly Standing Committee shall consider and regulate.

The Government shall specify this Article.

What is the regulation on taxable time in Vietnam?

Pursuant to Article 9 of the Law on Environmental Protection Tax 2010, the time for calculating environmental protection tax is as follows:

- For goods manufactured, sold, exchanged, donated, taxable time is the time transferring the ownership or right to use goods.

- For manufactured goods brought into internal consumption, taxable time is the time when taxable goods brought into use.

- For imported goods, taxable time is the time of registration of customs declarations.

For gasoline, petroleum produced or imported for sale, taxable time is the time when the business hub of petrol and oil sold.

When will the environmental protection taxpayer be paid tax refund in Vietnam?

Pursuant to Article 11 of the Law on Environmental Protection Tax 2010 as follows:

Tax refund

Environmental protection taxpayer is paid tax refund in the following cases:

1. Imported goods are still stored in warehouse, storage at the border gate and are subject to be supervised by the customs authority for re-export to foreign countries;

2. Imported goods to transport, sell abroad through agents in Vietnam; gasoline, petrol sold for vehicles of foreign firms on the route through Vietnam's ports or means of Vietnam's transportation on international transport road under the provisions of law;

3. Goods temporarily imported for re-export by business mode of temporary import for re-export.

4. Goods imported by the importer re-exporting to foreign countries;

5. Goods temporarily imported for participation in fairs, exhibitions and introduction of products in accordance with the law when re-exported to foreign countries.

Thus, according to the above provisions, the environmental protection taxpayer is paid tax refund in the following cases:

- Imported goods are still stored in warehouse, storage at the border gate and are subject to be supervised by the customs authority for re-export to foreign countries;

- Imported goods to transport, sell abroad through agents in Vietnam; gasoline, petrol sold for vehicles of foreign firms on the route through Vietnam's ports or means of Vietnam's transportation on international transport road under the provisions of law;

- Goods temporarily imported for re-export by business mode of temporary import for re-export.

- Goods imported by the importer re-exporting to foreign countries;

- Goods temporarily imported for participation in fairs, exhibitions and introduction of products in accordance with the law when re-exported to foreign countries.

What are the regulations on the performance of tax declaration, tax calculation and tax payment in Vietnam?

Pursuant to Article 10 of the Law on Environmental Protection Tax 2010 stipulating the implementation of tax declaration, tax calculation and tax payment

- The tax declaration, tax calculation, tax payment for environmental protection on goods produced and sold, exchanged, internally consumed, donated shall be made by the month and the provisions of the law on tax administration.

- The tax declaration, tax calculation, tax payment for environmental protection on imported goods shall be made at the same to time of import tax declaration and tax payment.

- Environmental protection tax is only paid once for goods produced or imported.

LawNet