What is the form of CIT return for foreign airlines in Vietnam? What are the components of CIT return for foreign airlines?

- Form No. 01/HKNN: What is the form of CIT return for foreign airlines in Vietnam?

- Shall the CIT for foreign airlines in Vietnam be declared quarterly?

- What are the components of CIT return for foreign airlines in Vietnam?

- When is the deadline for submission of tax declaration dossiers for foreign airlines in Vietnam?

Form No. 01/HKNN: What is the form of CIT return for foreign airlines in Vietnam?

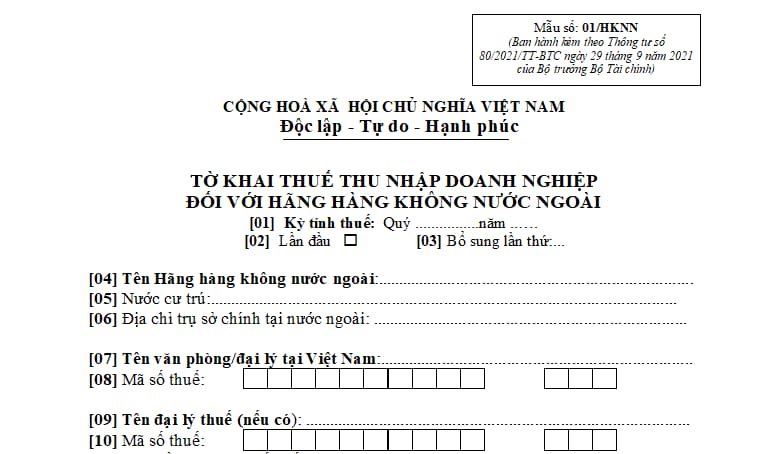

The form of CIT return for foreign airlines is Form No. 01/HKNN issued together with Circular 80/2021/TT-BTC. Below is an image of the form of CIT return for foreign airlines:

Download the form of CIT return for foreign airlines: Here.

Form No. 01/HKNN: What is the form of CIT return for foreign airlines in Vietnam? What are the components of CIT return for foreign airlines? (Image from the Internet)

Shall the CIT for foreign airlines in Vietnam be declared quarterly?

Pursuant to Point a, Clause 2, Article 8 of Decree 126/2020/ND-CP stipulates as follows:

Taxes declared monthly, quarterly, annually, separately; tax finalization

...

2. The following taxes and other amounts shall be declared quarterly:

a) Corporate income tax incurred by foreign airliners and foreign reinsurers.

b) VAT, corporate income tax, personal income tax declared on behalf of pledgors by credit institutions and third parties authorized by credit institutions to manage the collateral pending settlement.

c) Personal income tax deducted by income payers that are eligible to declare VAT quarterly and also decide to declare personal income tax quarterly; individuals earning salaries or remunerations (hereinafter referred to as “salary earners”) who decide to declare personal income tax quarterly with tax authorities.

d) Taxes and other amounts payable to state budget declared and paid on behalf of individuals by other organizations or individuals that are eligible to declare VAT quarterly and decide to declare tax on behalf of these individuals quarterly, except for the case specified in Point g Clause 4 of this Article.

dd) Surcharges when crude oil price increases (except petroleum activities of Vietsovpetro JV in block 09.1).

...

Thus, according to the above regulations, CIT for foreign airlines shall be declared quarterly.

What are the components of CIT return for foreign airlines in Vietnam?

Pursuant to Section 13.4 specified in Appendix I issued together with Decree 126/2020/ND-CP, components of CIT return for foreign airlines in Vietnam include:

- Corporate income tax declaration for foreign airlines (Form No. 01/HKNN issued together with Circular 80/2021/TT-BTC).

- A copy of the contractor contract or subcontractor contract certified by the taxpayer (for the first tax return of the contractor contract).

- Copy of business license or practice license certified by the taxpayer.

When is the deadline for submission of tax declaration dossiers for foreign airlines in Vietnam?

Pursuant to Point b, Clause 1, Article 44 of the Law on Tax Administration 2019:

Deadlines for submission of tax declaration dossiers

1. Deadlines for submission of tax declaration dossiers of taxes declared monthly and quarterly:

a) For taxes declared monthly: the 20th of the month succeeding the month in which tax is incurred;

b) For taxes declared quarterly: the last day of the first month of the succeeding quarter.

2. For taxes declared annually:

a) For annual tax statement dossiers: the last day of the 3rd month from the end of the calendar year or fiscal year. For annual tax declaration dossiers: the last day of the first month from the end of the calendar year or fiscal year

b) For annual personal income tax statements prepared by income earners: the last day of the 4th month from the end of the calendar year;

c) For presumptive tax declarations prepared by household businesses and individual businesses: the 15th of December of the preceding year. For new household businesses and individual businesses: within 10 days from the date of commencement of the business.

3. For declaration of taxes that are declared and paid upon incurrence: the 10th day from the day on which tax is incurred.

4. For tax declaration dossiers upon shutdown, contract termination, business conversion or business re-arrangement: the 45th day from the occurrence of the event.

5. The Government shall specify the deadlines for submission of statements of farming land levies, non-farming land levies; land levies; land rents, water surface rents; mineral extraction licensing fee; water resource extraction licensing fee; registration fee; licensing fees; other amounts payable to state budget in accordance with regulations of law on management and use of public property; multinational profit reports.

6. Deadlines for submission of customs dossiers of exports and imports are specified by the Law on Customs.

7. In case a taxpayer declares tax electronically on the last day of the time limit for declaration and the information portal of the tax authority is not functional, the taxpayer may submits the electronic declaration on the next day after the online portal is functional again.

Thus, according to the above regulations, the deadlines for submission of tax declaration dossiers for foreign airlines is the last day of the first month of the quarter following the quarter in which the tax liability arises.

LawNet