What is the form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

- What is the form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

- What are the regulations on documents for form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

- Vietnam: Can sponsorship for policy beneficiaries not prescribed by law be deducted when calculating taxable income?

What is the form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

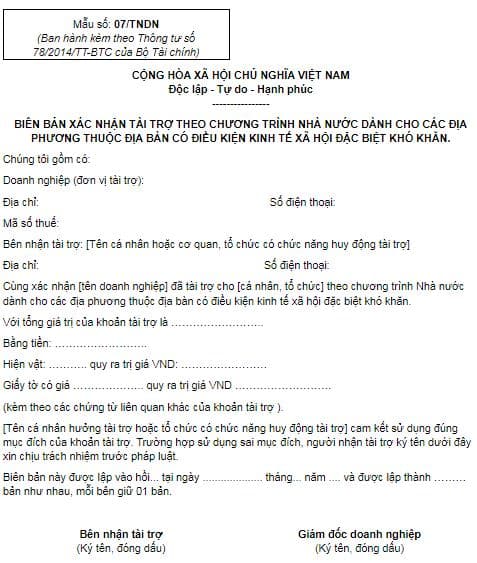

Currently, the form of certification of sponsorship for extremely disadvantaged areas State programs is made according to the Form 07/TNDN issued together with Circular 78/2014/TT BTC as follows:

Download the form of certification of sponsorship for extremely disadvantaged areas State programs: Click here.

What is the form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

What are the regulations on documents for form of certification of sponsorship for extremely disadvantaged areas State programs in Vietnam?

Pursuant to Clause 2, Article 6 of Circular 78/2014/TT BTC as amended by Article 4 of Circular 96/2015/TT-BTC as follows:

Deductible and non-deductible expenses when calculating taxable income

...

2. The expenses below are not deductible when calculating taxable income:

...

2.1. Expenses that do not meet all of the conditions in Clause 1 of this Article.

If the enterprise incurs expenses related to damage caused by natural disasters, epidemics, blazes, and other force majeure events (hereinafter referred to as calamities) without compensation, such expenses will be deductible when calculating taxable income. In particular:

The enterprise must determine the value of damage caused by calamities in accordance with law.

The damage value equals (=) total damage value minus (-) the value of damage that must be compensated by insurers other entities as prescribed by law.

a) Documents about assets/goods damaged by calamities that are included in deductible expenses include:

- A statement of value of damaged assets/goods made by the enterprise.

A statement of value of damaged assets/goods must specify the value of damaged assets/goods, causes, responsibilities for such damage, categories, quantity, value of recoverable assets/goods (if any); statement of damaged goods certified by legal representative of the enterprise.

- A compensation claim upheld by the insurer (if any).

- Documents about responsibility for provision of compensation (if any).

b) Expired goods and goods damaged because of natural deterioration that are not compensated will be deductible expenses when calculating taxable income.

Documents about expired goods and goods damaged because of natural deterioration and that are included in deductible expenses include:

- Statement of damaged goods made by the enterprise

A statement of value of damaged goods must specify the value of damaged goods, causes; categories, quantity, and values of recoverable goods (if any) enclosed with a statement of inventory of damaged goods certified by the legal representative of the company.

- A compensation claim upheld by the insurer (if any).

- Documents about responsibility for provision of compensation (if any).

c) The aforementioned documents shall be retained at the enterprise and presented to the tax authority on request.

...

2.26. Provision of sponsorship for scientific research against the law; provision of sponsorship for beneficiaries of incentive policies against the law; provision of sponsorship for extremely disadvantaged areas State programs.

Sponsorship under a State Program means a program run by the government in an extremely disadvantaged area (including sponsorship for building new bridges in extremely disadvantaged residential areas) under a project approved by a competent authority.

Provision of sponsorship shall comply with corresponding regulations of law.

Documents about sponsorship for extremely disadvantaged areas under State program, sponsorship for new bridges in extremely disadvantaged residential areas under a project approved by a competent authority, sponsorship for beneficiaries of incentive policies include: Certification of sponsorship bearing the signature of the representative of the sponsoring enterprise, the sponsorship recipient (or an organization permitted to raise sponsorship) (form no. 07/TNDN enclosed with Circular No. 78/2014/TT-BTC); invoices/receipts for purchase of goods (in case of in-kind sponsorship) or proof of payment (in case of monetary sponsorship).

Regulations on scientific research, procedures and documents about sponsorship for scientific research shall comply with regulations of the Law on Science and Technology and relevant guiding documents.

According to the above regulations, a dossier of certification of funding under a state program for an area with extremely difficult socio-economic conditions will include the following components:

- Certification of sponsorship

- Invoices/receipts for purchase of goods (in case of in-kind sponsorship) or proof of payment (in case of monetary sponsorship)

Vietnam: Can sponsorship for policy beneficiaries not prescribed by law be deducted when calculating taxable income?

Pursuant to Clause 2, Article 6 of Circular 78/2014/TT BTC as amended by Article 4 of Circular 96/2015/TT-BTC as follows:

Deductible and non-deductible expenses when calculating taxable income

...

2. The expenses below are not deductible when calculating taxable income:

2.26. Provision of sponsorship for scientific research against the law; provision of sponsorship for beneficiaries of incentive policies against the law; provision of sponsorship for extremely disadvantaged areas State programs.

...

Thus, expenditures to finance policy beneficiaries that are not prescribed by law will not be deducted when determining taxable income.

LawNet