What is the form of a list and conventional prices of special assets for fixed assets at authorities in Vietnam?

What is the special asset in Vietnam?

Pursuant to Article 5 of Circular 45/2018/TT-BTC stipulating special assets as follows:

Special assets

1. Fixed assets of which costs of forming or real values are not determined, however, they require to be managed strictly, (such as: antiques, exhibits in museums, monuments, ranked historical relics), fixed assets which are brands of public sector entities and have undetermined costs of forming and are defined as special assets.

2. Based on the actual conditions and management requirements for the assets specified in clause 1 of this Article, Ministers and Heads of central agencies and People’s Committees of provinces shall promulgate the list of special assets under the management of ministries and central or local agencies (using form No. 03 in Appendix 02 hereto) in order to exercise unified management.

3. The cost of a special asset recorded in the accounting book and declared while logging information into National Asset Database shall be determined according to the conventional price. The conventional price of one special asset is 10.000.000 VND (ten million VND).

Thus, special assets are fixed assets of which costs of forming or real values are not determined, however, they require to be managed strictly, (such as: antiques, exhibits in museums, monuments, ranked historical relics), fixed assets which are brands of public sector entities and have undetermined costs of forming.

What is the form of a list and conventional prices of special assets for fixed assets at authorities in Vietnam?

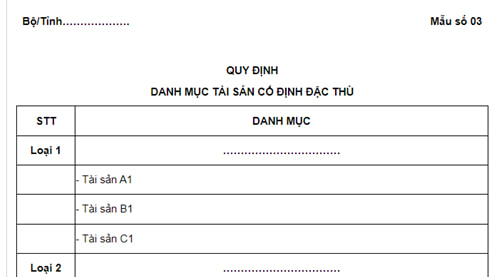

The form of a list and conventional prices of special assets in managing public property shall follow Form No. 03, Appendix 2 issued together with Circular 45/2018/TT-BTC as follows:

See the form of a list and conventional prices of special assets: here.

Are special assets in Vietnam not eligible for depreciation calculation?

Pursuant to Article 12 of Circular 45/2018/TT-BTC stipulating the scope of depreciation calculation of fixed assets as follows:

Scope of depreciation calculation of fixed assets

1. The current fixed assets of agencies, organizations and units and the fixed assets provided to the enterprises by the state without calculation of the state capital portion shall be calculated for their depreciation, except the cases specified in clause 2, clause 3 of this Article.

2. The fixed assets of public sector entities must be depreciated according to Article 16 hereof, including:

a. The fixed assets of public sector entities that pay for the regular expenses and investment expenses themselves.

b. The fixed assets of public sector entities which require its depreciation to be included in the service price according to the law.

c. The fixed assets of public sector entities which are not specified in point a and b of this clause shall be used in business activities, leasing activities, joint venture and association activities without establishing new legal entity.

3. The following fixed assets shall not be calculated for their depreciation:

a. The fixed assets are the land use rights which must be determined to be included in the value of such assets as specified in Article 100 of the Decree No. 151/2017/ND-CP

b. The special fixed assets specified in Article 5 hereof, except the fixed assets which are brands of public sector entities and are used in joint venture and association activities without establishing new legal entity according to point c, clause 2 of this Article.

c. Rented fixed assets.

d. Fixed assets being kept on behalf of the State.

dd. Fixed assets that are still usable after their depreciation is being fully calculated or their costs are being completely depreciated.

e. Fixed assets that are not usable though their depreciation is not fully calculated and their costs are not completely depreciated.

Thus, special assets in Vietnam are not eligible for depreciation calculation? and depreciations of fixed assets being trademarks of public administrative units shall be used in business activities, leasing activities, joint venture and association activities without establishing new legal entity.

Note: The above provisions are applied to fixed assets at state agencies, public administrative units, units of the people's armed forces, agencies of the Communist Party of Vietnam, organizations using the state budget (hereinafter referred to as agencies, organizations and units) and fixed assets assigned by the State to enterprises for management, excluding state funds in enterprises.

LawNet