What is the current interest rate of international Vietcombank credit cards? Is there an overdue debt fee for late credit card payments in Vietnam?

- Vietnam: What is the current international Vietcombank credit card interest rate?

- What are eligible entities to use credit cards in Vietnam according to current legal regulations?

- Is there an overdue debt fee for late credit card payments in Vietnam?

- What are the cases of rejection of credit card payments in Vietnam?

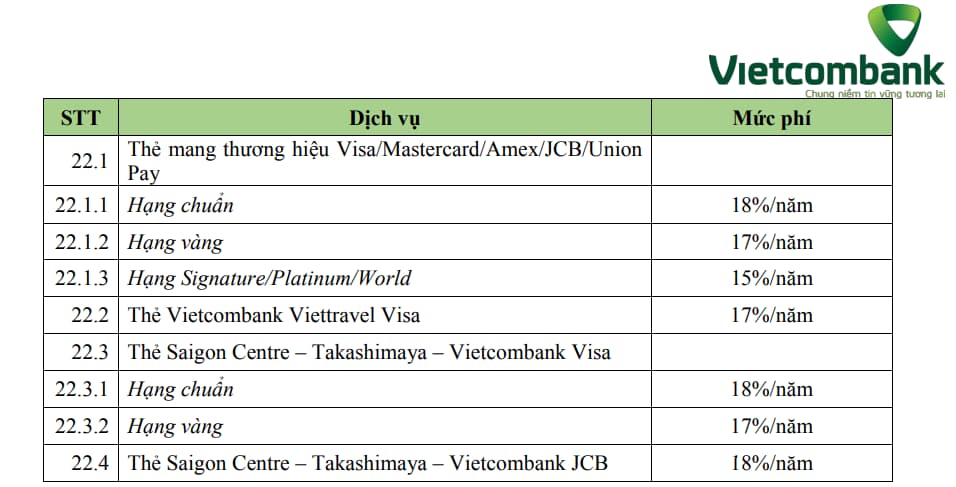

Vietnam: What is the current international Vietcombank credit card interest rate?

According to the announcement on Vietcombank's information page, international Vietcombank credit card interest rates are as follows:

Note: International credit card interest rates are calculated as a percentage per year (%/year), a year is 365 days (Three hundred sixty-five days). Vietcombank may change this Fee Schedule from time to time and will notify fee changes 07 days before application, through Vietcombank's official website (website: www.vietcombank.com.vn) or other methods according to Vietcombank's regulations from time to time.

Vietnam: What is the current interest rate of international Vietcombank credit cards? (Image from the Internet)

What are eligible entities to use credit cards in Vietnam according to current legal regulations?

Pursuant to the provisions of Article 16 of Circular 19/2016/TT-NHNN, the eligible entities to use credit cards in Vietnam are as follows:

For principal cardholders being individuals:

-Any person who is 18 years of age or older and has full legal capacity as prescribed by law is permitted to use debit cards, credit cards and/or prepaid cards;

- Any person aged 15 to less than 18 years who does not have lack of legal capacity or limited legal capacity, and has his/her own assets to be taken as security in the card usage is permitted to use debit cards without overdraft facility and prepaid cards.

For principal cardholders being organizations:

Organizations legally established and operated under Vietnamese law, including: juridical persons, private enterprises shall be permitted to use all types of cards. The cardholder being organization may authorize a person to use the organization’s card on its behalf or use supplementary card as prescribed in this Circular.

With respect to supplementary cardholders

A supplementary cardholder may use card as specific authorization of the principal cardholder in accordance with the following requirements:

- An person who is 18 years of age or older and has full legal capacity as prescribed by law is permitted to use debit cards, credit cards and/or prepaid cards;

- An person aged 15 to less than 18 years who does not have lack of legal capacity or limited legal capacity and obtain an authorization in writing made by his/her legal representative to permit him/her to use debit cards without overdraft facility and prepaid cards;

- An person aged 6 to less than 15 years who does not have lack of legal capacity or limited legal capacity and obtain an authorization in writing made by his/her legal representative to permit him/her to use debit cards without overdraft facility and prepaid cards;

In case foreigners use the cards specified in Clauses 1 and 3 of this Article, they must be allowed to reside in Vietnam for a period of 12 months or more.

Note: Circular 19/2016/TT-NHNN is amended by Circular 26/2017/TT-NHNN, Circular 28/2019/TT-NHNN, Circular 17/2021/TT-NHNN

Is there an overdue debt fee for late credit card payments in Vietnam?

In Article 13 of Circular 19/2016/TT-NHNN amended by Clause 6, Article 1 of Circular 17/2021/TT-NHNN, it is stipulated:

Agreement on card issuance and usage

1. An agreement on card issuance and usage must contain at least the following contents:

...

g. The credit facility agreement to the cardholder, includes: Card facility agreement and changes of card facility agreement, including overdraft limit (for debit cards) and credit limit; interest rates, how interest is charged on the loan, order of recovery of loan principal and interest (for overdrafted credit and debit cards); credit granting period, terms of credit, loan term, minimum sum of repayment, method of repayment, overdue debt fee (if any). The credit facility agreement concluded with the cardholder may be specified in the agreement on card issuance and usage or in another document;

...

Card fees and charges specified in Article 5 of Circular 19/2016/TT-NHNN are as follows:

Card fees and charges

1. Only card issuers are permitted to collect fees and charges from cardholders. Each card issuer must collect fees and charges according to its own schedule of card service fees and charges and must not collect any additional type of fees/charges not mentioned in the announced schedule of card service fees and charges. The schedule of card service charges must specify types of fees and charges applicable to every card and card services. The schedule of card service fees and charges of card issuers must comply with regulations of law, be posted publicly and provided for cardholders before its application and upon any change to this schedule. Types of notification and supply of information of those charges to cardholders must be specified in the agreement on card issuance and usage. A period of at least 7 days is required for the application of any change of the service charges from the date on which it is informed and such period must be specified in the agreement on card issuance and usage.

Thus, when opening a credit card, the agreement on card issuance and usage will contain provisions on overdue debt fee (if any). Currently, card issuers often impose fines on overdue debts. Therefore, if you are late in paying your credit card even for 1 day, you will have to pay a overdue debt fee and corresponding interest rate.

In short, when paying late on a credit card, customers will be subject to overdue debt fees and corresponding interest rates as agreed in the agreement on card issuance and usage and fee schedule announced by the card issuer.

What are the cases of rejection of credit card payments in Vietnam?

Pursuant to the provisions of Article 27 of Circular 19/2016/TT-NHNN amended and supplemented by Article 1 of Circular 26/2017/TT-NHNN and Circular 17/2021/TT-NHNN, payments of credit cards in particular and bank cards in general may be rejected in the following cases:

(1) Card issuers, acquirers and merchants must reject the card payment in any of the following cases:

- The card is used in a prohibited card transaction as prescribed in Article 8 of Circular 19/2016/TT-NHNN;

- The card has been lost as notified by the cardholder;

- The card is expired;

- The card is locked.

(2) The card issuer, the acquirer, the merchant may refuse card payment if they have reasonable doubts as to truthfulness and transaction purpose of the card holder in accordance with the law on anti-money laundering.

(3) Card issuers, acquirers and merchants may reject the card payment as agreed in any of the following cases:

- The balance on the payment deposit account, the credit limit or the overdraft limit (if any) is insufficient for the payment;

- The cardholder breaches any of the regulations of the card issuer on the cases of rejection of card payments as agreed upon by the cardholder and the card issuer.

LawNet