What is the current form of certificate of sponsorship for education of enterprise in Vietnam?

What is the current form of certificate of sponsorship for education of enterprise in Vietnam?

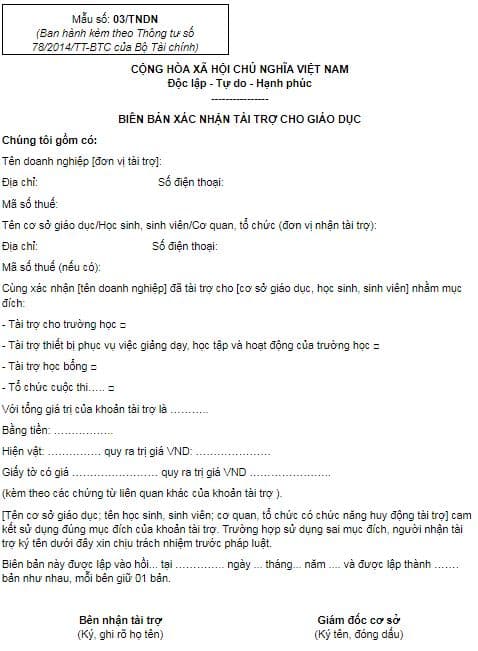

Currently, the form of minutes of certification of sponsorship for education of enterprises is made according to Form 03/TNDN issued together with Circular 78/2014/TT-BTC as follows:

Download the current form of certificate of sponsorship for education: Here.

What is the current form of certificate of sponsorship for education of enterprise in Vietnam?

Vietnam: What are the sponsorships for education which are not deductible when calculating taxable income?

Pursuant to Clause 2, Article 6 of Circular 78/2014/TT-BTC as amended by Article 4 of Circular 96/2015/TT-BTC as follows:

Deductible and non-deductible expenses when calculating taxable income

...

2. The expenses below are not deductible when calculating taxable income:

...

2.1. Expenses that do not meet all of the conditions in Clause 1 of this Article.

If the enterprise incurs expenses related to damage caused by natural disasters, epidemics, blazes, and other force majeure events (hereinafter referred to as calamities) without compensation, such expenses will be deductible when calculating taxable income. In particular:

The enterprise must determine the value of damage caused by calamities in accordance with law.

The damage value equals (=) total damage value minus (-) the value of damage that must be compensated by insurers other entities as prescribed by law.

a) Documents about assets/goods damaged by calamities that are included in deductible expenses include:

- A statement of value of damaged assets/goods made by the enterprise.

A statement of value of damaged assets/goods must specify the value of damaged assets/goods, causes, responsibilities for such damage, categories, quantity, value of recoverable assets/goods (if any); statement of damaged goods certified by legal representative of the enterprise.

- A compensation claim upheld by the insurer (if any).

- Documents about responsibility for provision of compensation (if any).

b) Expired goods and goods damaged because of natural deterioration that are not compensated will be deductible expenses when calculating taxable income.

Documents about expired goods and goods damaged because of natural deterioration and that are included in deductible expenses include:

- Statement of damaged goods made by the enterprise

A statement of value of damaged goods must specify the value of damaged goods, causes; categories, quantity, and values of recoverable goods (if any) enclosed with a statement of inventory of damaged goods certified by the legal representative of the company.

- A compensation claim upheld by the insurer (if any).

- Documents about responsibility for provision of compensation (if any).

c) The aforementioned documents shall be retained at the enterprise and presented to the tax authority on request.

...

2.22. Provision of sponsorship for education (including sponsorship for vocational education) for illegitimate recipients according to Point (a) or without documentation mentioned in Point (b) below:

a) Sponsorship for education include: Sponsorship for public and private schools of national education system as prescribed by regulations of law on education, provided such sponsorship is not meant to contribute capital or buy shares of schools; Sponsorship for infrastructure and equipment serving teaching and learning in schools; Sponsorship for regular operations of schools; Sponsorships for students of compulsory education institutions, vocational education institutions, and higher education institutions prescribed in the Law on Education (direct sponsorship for students, sponsorship provided via educational institutions, organizations permitted to raise sponsorships as prescribed by law); Sponsorship for competitions in the schools subjects participated by learners; Sponsorship for establishment of scholarship funds as prescribed by regulations of law on education.

According to the above regulations, educational funding expenses other than the following grants are not deductible when calculating corporate income tax:

- Sponsorship for public and private schools of national education system as prescribed by regulations of law on education, provided such sponsorship is not meant to contribute capital or buy shares of schools;

- Sponsorship for infrastructure and equipment serving teaching and learning in schools;

- Sponsorship for regular operations of schools; Sponsorships for students of compulsory education institutions, vocational education institutions, and higher education institutions prescribed in the Law on Education (direct sponsorship for students, sponsorship provided via educational institutions, organizations permitted to raise sponsorships as prescribed by law);

- Sponsorship for competitions in the schools subjects participated by learners;

- Sponsorship for establishment of scholarship funds as prescribed by regulations of law on education.

How many types of education sponsorship are there in Vietnam?

Pursuant to Article 4 of Circular 16/2018/TT-BGDDT stipulating the following forms of education funding:

- Cash sponsorships: Sponsors may transfer a sum of money in the Vietnam dong or another foreign currency, diamonds, gems and precious metals directly to educational institutions or into accounts of educational institutions opened at state treasuries or commercial banks.

- Sponsorships in kind: Sponsors may transfer to educational institutions such material objects as textbooks, notebooks, clothes, food, food supplies, materials, equipment, teaching aids, construction works and other valuable objects in order to satisfy actual needs of students and educational institutions.

As regards construction works transferred as a sponsorship, evaluation and approval of technical designs and total cost estimates, granting of construction permits, quality control of construction works, pre-acceptance testing, hand-over, warranty and insurance shall be conformable to existing legislative regulations on capital construction investment.

- Non-material sponsorships: Sponsors may transfer or grant rights of free use of copyrights and rights of ownership of property under intellectual property protection; land use rights; contribution of labor days; provide training services, and those relating to sightseeing tours, surveys, seminars, or consultants, free of charge to educational institutions.

LawNet