What is a sample letter asking whether the VAT rate is 8% or 10% sent to the tax authority in Vietnam? To download excel files of goods and services that are not subject to 8% VAT?

- What is a sample letter asking whether the VAT rate is 8% or 10% sent to the tax authority in Vietnam?

- Which goods and services are subject to the 8% and 10% VAT rates in Vietnam?

- Vietnam: To download excel files of goods and services that are not subject to 8% VAT?

- Vietnam: When will the 8% VAT rate apply?

What is a sample letter asking whether the VAT rate is 8% or 10% sent to the tax authority in Vietnam?

The sample letter asking whether the VAT rate is 8% or 10% sent to the tax authority is a document asking for answers to questions prepared by the taxpayer and sent to the tax authority. Below is a sample reference letter requesting answers to VAT rates sent to the tax authority:

Download the sample letter requesting answers to VAT rates here: download

What is a sample letter asking whether the VAT rate is 8% or 10% sent to the tax authority in Vietnam? To download excel files of goods and services that are not subject to 8% VAT? (Picture from internet)

Which goods and services are subject to the 8% and 10% VAT rates in Vietnam?

Pursuant to Article 1 of Decree 44/2023/ND-CP stipulates as follows:

VAT reduction

1. VAT on goods and services that are currently subject to 10% VAT shall be reduced, except the following goods and services:

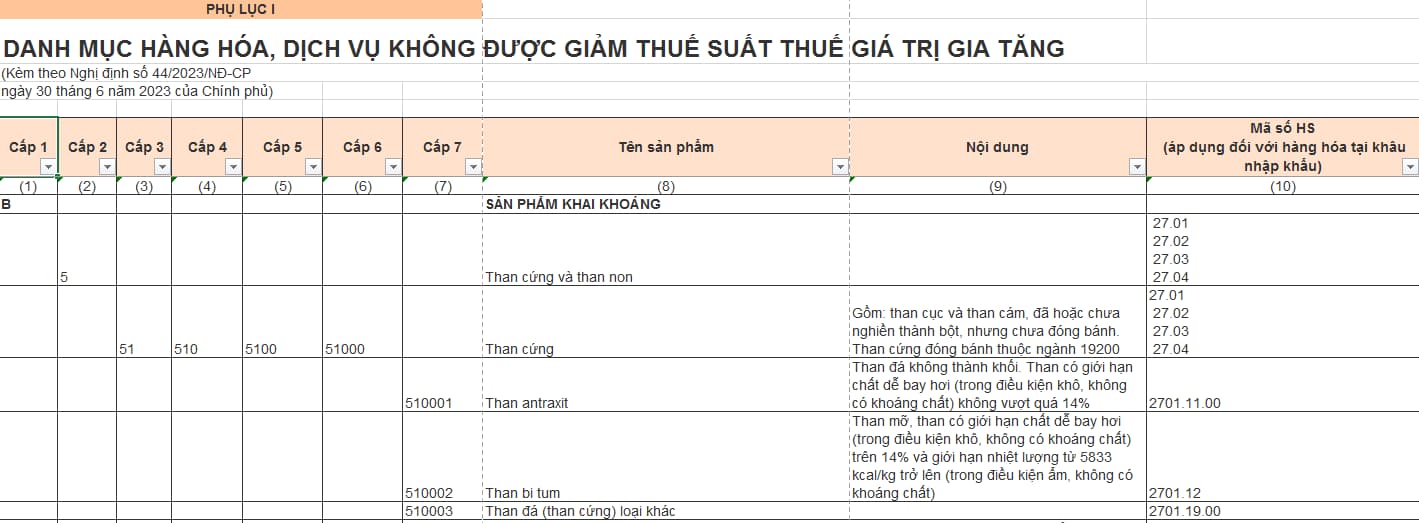

a) Telecommunication, financial activities, banking activities, securities, insurance, trading of real estate, metal and precast metal products, mining products (excluding coal mining), coke mining, refined oil, chemical products. Further details are provided in Appendix I enclosed herewith.

b) Goods and services subject to excise tax. Further details are provided in Appendix II enclosed herewith.

c) Information technology products and services as prescribed in the Law on information technology. Further details are provided in Appendix III enclosed herewith.

d) VAT on goods and services of a specific type prescribed in Clause 1 of this Article shall be reduced consistently at all stages, including import, production, processing and trading. Coal products mined for sale (including coal products mined and then washed, sieved and classified under a closed process before they are sold) are eligible for VAT reduction. Coal products in Appendix I enclosed herewith are not eligible for VAT reduction at any stages other than the mining stage.

Coal products produced under a closed process of economic corporations or groups shall be also eligible for VAT reduction.

In case any of the goods and services in Appendixes I, II and III enclosed herewith is not subject to VAT or is subject to 5% VAT in accordance with the Law on value-added tax, VAT on that good or service shall be paid in accordance with the Law on value-added tax and shall not be reduced.

2. VAT reduction rates

a) Business establishments that pay VAT using the credit-invoice method shall pay 8% VAT on the goods and services specified in Clause 1 of this Article.

...

Accordingly, the 8% VAT rate is a reduced tax rate to support the socio-economic recovery and development program, applicable to groups of goods and services currently subject to 10% VAT.

So:

(1) Group of goods and services subject to 10% tax rate includes:

- Telecommunications, financial activities, banking, securities, insurance, real estate business, metals and prefabricated metal products, mining products (excluding coal mining), coke, refined petroleum, chemical products. Further details are provided in Appendix I enclosed with Decree 44/2023/ND-CP.

- Products and services subject to special consumption tax. Further details are provided in Appendix II enclosed with Decree 44/2023/ND-CP.

- Information technology according to the law on information technology. Further details are provided in Appendix III enclosed with Decree 44/2023/ND-CP.

In other words, the 10% tax rate applies to goods and services that are not subject to VAT, tax rates of 0%, 5%, and are not eligible for tax rate reduction to 8%.

(2) Group of goods and services subject to 8% tax rate includes:

- Goods and services do not apply VAT rates of 5%, 0% and 10%.

Vietnam: To download excel files of goods and services that are not subject to 8% VAT?

Below is an excel files of goods and services that are not subject to 8% VAT in 2023 according to Decree 44/2023/ND-CP:

Download the excel file list of goods that are not subject to 8% VAT here: download

Vietnam: When will the 8% VAT rate apply?

Pursuant to Article 2 of Decree 44/2023/ND-CP stipulating the effectiveness and organization of implementation as follows:

Effect and implementation organization

1. This Decree takes effect from July 01, 2023 to December 31, 2023 inclusively.

2. Ministries, within the ambit of their assigned functions and tasks, and Provincial People’s Committees shall direct relevant agencies to disseminate, instruct and inspect the implementation of regulations on VAT reduction in Article 1 of this Decree, especially solutions for stabilizing supply and demand for goods and services eligible for VAT reduction so as to ensure stable market prices of goods and services (prices exclusive of VAT) for the period from July 01, 2023 to December 31, 2023 inclusively.

3. Difficulties that arise during the implementation of this Decree should be reported to the Ministry of Finance of Vietnam for consideration.

4. Ministers, heads of ministerial agencies, heads of Governmental agencies, Chairpersons of Provincial People’s Committees and relevant enterprises, organizations and individuals are responsible for the implementation of this Decree.

Thus, the 8% VAT reduction policy for goods and services reduced according to the provisions of Decree 44/2023/ND-CP applies until December 31, 2023.

LawNet