What are the regulations on the sample application form for a Tax Registration Certificate for individuals in Vietnam?

What are the regulations on the sample application form for a Tax Registration Certificate for individuals in Vietnam?

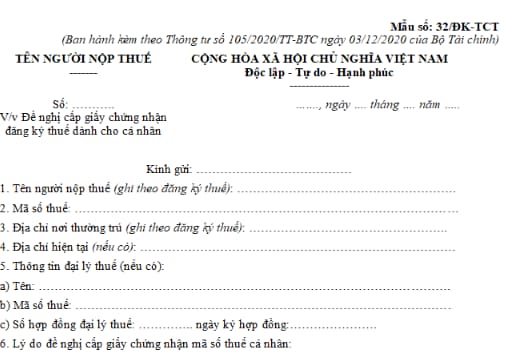

Currently, the sample form of application for a Tax Registration Certificate for individuals is specified in form No. 32/DK-TCT issued together with Circular 105/2020/TT-BTC, specifically as follows:

Download the Application Form for Tax Registration Certificate for individuals: here

What are the regulations on the sample application form for a Tax Registration Certificate for individuals in Vietnam?

Who are the tax registrants in Vietnam?

Pursuant to Clause 1, Article 30 of the Law on Tax Administration in Vietnam 2019 provides as follows:

Article 30. Applying for taxpayer registration and TIN issuance

1. Taxpayers must apply for taxpayer registration and shall be issued with TINs by tax authorities before beginning their business operations or incurring amounts payable to the state budget. The following entities shall apply for taxpayer registration:

a) Enterprises, organizations and/or individuals shall apply for taxpayer registration through the interlinked single-window system together with enterprise, cooperative or business registration (hereinafter referred to as “business registration”) as prescribed in the Law on Enterprises in Vietnam and other relevant regulations;

b) Organizations and individuals beside those stipulated in Point a of this clause shall register directly with tax authorities as regulated by the Minister of Finance in Vietnam.

…

Accordingly, tax registration subjects include:

(1) Enterprises, organizations and/or individuals shall apply for taxpayer registration through the interlinked single-window system together with enterprise, cooperative or business registration (hereinafter referred to as “business registration”) as prescribed in the Law on Enterprises in Vietnam and other relevant regulations;

(2) Taxpayers subject to tax registration directly with tax authorities, according to the guidance in Article 4 of Circular 105/2020/TT-BTC, including:

- Enterprises operating in the sectors of insurance, accounting, auditing, lawyers, notarization, or other specialized sectors that are not required for enterprise registration at business registration authorities as per the specialized laws (hereinafter referred to as business entities)

- Public sector entities, business entities of armed forces; business entities of political organizations, socio-political organizations, social organizations, socio-professional organizations that conduct business as prescribed by law but are not required to apply for enterprise registration at business registration authorities; organizations of neighbor countries on land with Vietnam that conduct sale, barter at border marketplaces, checkpoint marketplaces and marketplaces in checkpoint economic zones; representative offices of foreign organizations in Vietnam; artels that are established and operating under the Civil Code (hereinafter referred to as business entities).

- Organizations established by competent authorities without production or business operation but taking on liabilities to government budget (hereinafter referred to as other entities)

- Foreign organizations and individuals, organizations in Vietnam that use foreign humanitarian aid and/or non-refundable aid to buy VAT-inclusive goods or services in Vietnam to provide non-refundable aid and/or humanitarian aid; diplomatic missions and consular offices and representative agencies of international organizations in Vietnam that are eligible for VAT refund as entities entitled to diplomatic immunity and privileges; ODA project owners that are eligible for VAT refund, representative offices of ODA project sponsors, organizations designated by foreign sponsors to manage ODA grant programs/projects (hereinafter referred to as other entities).

- Foreign organizations without Vietnamese’s legal status, foreign individuals doing independent business in Vietnam in accordance with Vietnam’s law and earning incomes in Vietnam or taking on tax liabilities in Vietnam (hereinafter referred to as foreign contractors or foreign sub-contractors).

- Overseas suppliers without permanent establishments in Vietnam that operate electronic commerce, business based on digital platform and other services together with organizations or individuals in Vietnam (hereinafter referred to as overseas suppliers).

- Enterprises, cooperatives, business entities, other entities and individuals that are responsible for withholding and remitting the taxes on behalf of other taxpayers and declare and determine their own taxes separately from those taxes of the said taxpayers as per the tax law (except for the income payers upon withholding and remitting personal income taxes on others' behalf); commercial banks, payment service intermediary providers or entities authorized by overseas suppliers to declare, withhold and remit taxes on behalf of overseas suppliers (hereinafter referred to withholding agents). An income payer shall, upon withholding and remitting a personal income tax, use the TIN that was already issued.

- Executives, general executive companies, joint ventures, organizations authorized by the Vietnamese Government to receive profits distributed from petroleum fields in the overlapping areas, contractors, and investors entering into petroleum contracts or agreements, parent company - Petro Vietnam as the representative of host country that receives profits distributed from petroleum contracts or agreements

- Households, individuals engaged in production and business of goods or services, including individuals of neighbor countries on land with Vietnam engaging in sale and barter at border marketplace, checkpoint marketplaces, marketplaces in checkpoint economic zones) (hereinafter referred to as household/individual businesses).

- Individuals earning incomes subject to personal income tax (excluding individual businesses)

- Individuals who have dependents as per the law on personal income tax.

- Organizations and individuals authorized by tax authorities to collect amounts receivable (hereinafter referred to as authorized tax collectors).

- Other entities, households and individuals taking on liabilities to the government budget.

What information does the tax registration certificate in Vietnam include?

Pursuant to Clause 1, Article 34 of the Law on Tax Administration in Vietnam 2019, the information on the tax registration certificate includes:

- Name of the taxpayer;

- TIN;

- Number, date of the business registration certificate or establishment and operation license or investment registration certificate for business organizations and individuals; number, date of the establishment decision for organizations not required to apply for business registration; information of identity card, citizen identification or passport for individuals not subject to business registration;

- Supervisory tax authority.

LawNet