What are the procedures for the separate provision of authenticated e-invoices in Vietnam?

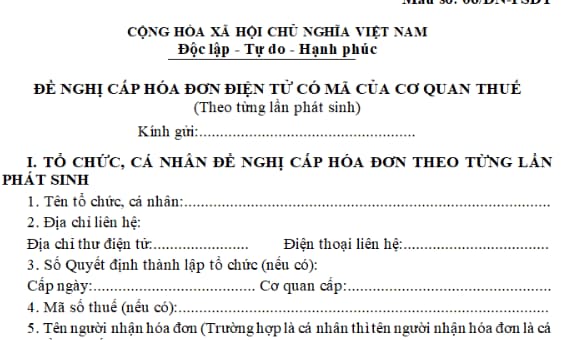

What is the application form for the separate provision of authenticated e-invoices in Vietnam?

Currently, the application form for separate provision of authenticated e-invoices incurred is specified in form 06/DN-PSĐT issued together with Decree 123/2020/ND-CP, specifically as follows:

Download the application form for separate provision of authenticated e-invoices here.

What are the procedures for the separate provision of authenticated e-invoices in Vietnam? (Image from the Internet)

What are the procedures for the separate provision of authenticated e-invoices in Vietnam?

Pursuant to Point b, Clause 2, Article 13 of Decree 123/2020/ND-CP has the following provisions:

Use of e-invoices in sale of goods and provision of services

...

2. Issuance and tax declaration upon tax authority’s separate provision of authenticated e-invoices:

...

b) Enterprises, business entities, other organizations, household businesses and individual businesses eligible for separate provision of authenticated e-invoices shall submit the application for provision of authenticated e-invoices (using form No. 06/DN-PSDT in Appendix IA enclosed herewith) to the tax authority and enter the tax authority’s e-invoice system to generate e-invoices.

After the applicant has fully declared and paid VAT, personal income tax, corporate income tax, other taxes and fees (if any), the tax authority shall authenticate the e-invoices generated by the applicant.

The applicant shall be held responsible for the accuracy of information on the e-invoices authenticated separately by the tax authority.

Accordingly, if enterprises, business entities, other organizations, household businesses and individual businesses eligible for separate provision of authenticated e-invoices shall submit the application for provision of authenticated e-invoices to the tax authority and enter the tax authority’s e-invoice system to generate e-invoices.

The applicant has to fully declare and pay VAT, personal income tax, corporate income tax, other taxes and fees

Then, the tax authority shall authenticate the e-invoices generated by the applicant.

At the same time, the applicant shall be held responsible for the accuracy of information on the e-invoices authenticated separately by the tax authority.

How to determine the tax authorities providing separate authenticated e-invoices in Vietnam?

Pursuant to Point c, Clause 2, Article 13 of Decree 123/2020/ND-CP, the way to determine the tax authorities providing separate authenticated e-invoices is guided as follows:

- For organizations and enterprises: The tax authority in charge of the area where the organization or enterprise applies for taxpayer registration, the area in which the organization is headquartered according to the decision on establishment, or the area in which goods/services are sold.

- For household businesses and individual businesses:

+ A household business or individual business with a fixed business location shall submit the application for provision of authenticated e-invoices to the Sub-department of taxation of the district where the household or individual business is located.

+ A household business or individual business without a fixed business location shall submit the application for provision of authenticated e-invoices to the Sub-department of taxation of the district where they register or reside.

LawNet