What are the detailed guidelines for determining goods eligible for VAT reduction in Vietnam in 2023? What are the principles of determining goods eligible for VAT reduction?

- Vietnam: What is the VAT reduction policy of 8% in 2023 according to Decree 44/2023/ND-CP?

- What are the principles of determining goods eligible for VAT reduction in Vietnam?

- How to determine goods eligible for VAT reduction in Vietnam in 2023 according to product and service codes?

- How to determine goods eligible for VAT reduction in Vietnam in 2023 by HS code?

Vietnam: What is the VAT reduction policy of 8% in 2023 according to Decree 44/2023/ND-CP?

According to the provisions of Article 1 of Decree 44/2023/ND-CP, VAT on goods and services that are currently subject to 10% VAT shall be reduced, except the following goods and services:

- Telecommunication, financial activities, banking activities, securities, insurance, trading of real estate, metal and precast metal products, mining products (excluding coal mining), coke mining, refined oil, chemical products. Further details are provided in Appendix I enclosed herewith.

- Goods and services subject to excise tax. Further details are provided in Appendix II enclosed herewith.

- Information technology products and services as prescribed in the Law on information technology. Further details are provided in Appendix III enclosed herewith.

- VAT on goods and services of a specific type prescribed in Clause 1 of this Article shall be reduced consistently at all stages, including import, production, processing and trading. Coal products mined for sale (including coal products mined and then washed, sieved and classified under a closed process before they are sold) are eligible for VAT reduction. Coal products in Appendix I enclosed herewith are not eligible for VAT reduction at any stages other than the mining stage.

Coal products produced under a closed process of economic corporations or groups shall be also eligible for VAT reduction.

In case any of the goods and services in Appendixes I, II and III enclosed herewith is not subject to VAT or is subject to 5% VAT in accordance with the Law on value-added tax, VAT on that good or service shall be paid in accordance with the Law on value-added tax and shall not be reduced.

What are the detailed guidelines for determining goods eligible for VAT reduction in Vietnam in 2023? What are the principles of determining goods eligible for VAT reduction?

What are the principles of determining goods eligible for VAT reduction in Vietnam?

Pursuant to the provisions of Decree 44/2023/ND-CP, the determination of subjects eligible for VAT reduction in 2023 from 10% to 8% will be based on a number of regulations as follows:

- The tax reduction applies to groups of goods and services currently subject to the 10% tax rate, except for the group of goods and services specified in Appendices I, II, III issued together with Decree 44/2023/ND-CP

- Business establishments shall base on the product industry codes and the list of HS codes (applicable to goods at the stage of importation) to look up and compare them with Appendices I, II and III issued together with the Decree 44/2023/ND-CP to determine whether goods and services are eligible for tax reduction.

- Goods and services that are not subject to VAT or subject to 0% or 5% VAT will not be eligible for VAT reduction.

- The reduction of value added tax is applied uniformly at the stages of import, production, processing, business and trade.

Particularly for coal products, it is only applied to the selling stage of mining (including coal mined and then going through screening, sorting, and then sold out), other stages are not eligible for tax reduction.

How to determine goods eligible for VAT reduction in Vietnam in 2023 according to product and service codes?

Decree 44/2023/ND-CP stipulates that business establishments shall base on the product codes of goods and services and the list of HS codes (applicable to goods at the stage of importation) to search, compare with the list of goods and services not eligible for VAT reduction in the Appendix I, II, III issued together with Decree 44/2023/ND-CP to determine the goods and services eligible for VAT reduction.

Specifically:

In order to determine whether the goods or services being traded are eligible for VAT reduction, the name and product code of such goods or services must be identified.

Accordingly, in order to determine the name and code of goods and services being traded, one of the following two ways:

Method 1: Look up the list of business line codes through the National Business Registration Portal (in case the business establishment has fully completed the registration procedures, changed business lines) , then based on the list of business lines to determine the product code (goods, services).

Method 2: List the products that your establishment is actually doing business in (in fact, many establishments still do business lines and trades that have not been registered for business).

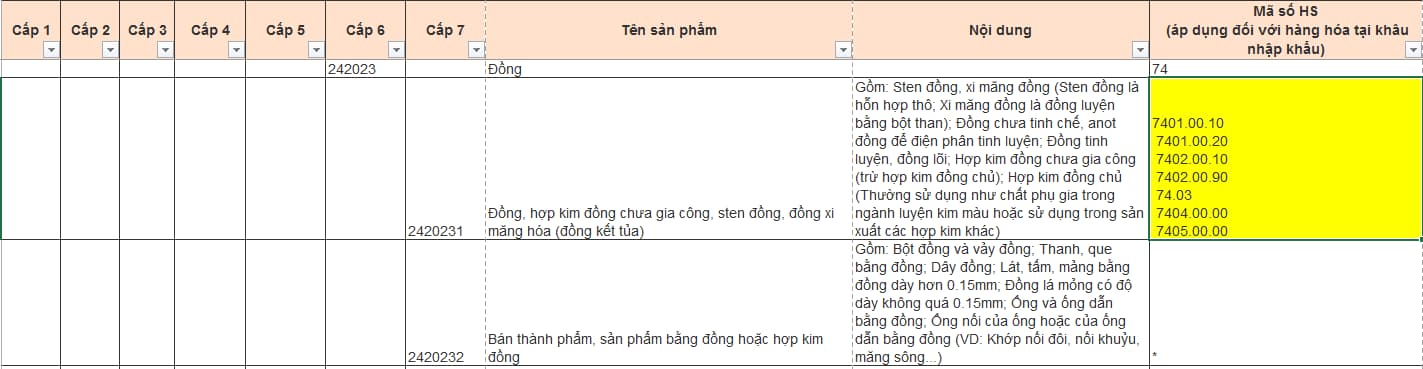

Based on the above business code, the business establishment finds the corresponding product code in Decision 43/2018/QD-TTg, then compares it with Appendix I attached to Decree 44/2023/ND-CP (column from Level 1 to Level 7):

- If it is in the list of industries not eligible for reduction, an invoice with the VAT rate of 10% will be issued.

- If not on the list not eligible for reduction, an invoice with the VAT rate of 8% will be issued.

Note:

- Appendix I promulgated together with Decree 44/2023/ND-CP is a part of the Appendix on the list and contents of the system of Vietnamese products promulgated together with Decision 43/2018/QD-TTg to be divided do 7 levels (from level 1 to level 7).

- Enterprises register business lines under the code level 4 based on the Vietnam Economic Sector System in Decision 27/2018/QD-TTg.

=> In addition to relying on the industry code level 4 on the business registration to look up, it is necessary to determine which goods or services are actually trading, then, look up the name or product code / HS code of the goods, services, then compare with the Appendix of Decree 44 to determine whether the product is eligible for VAT reduction or not.

How to determine goods eligible for VAT reduction in Vietnam in 2023 by HS code?

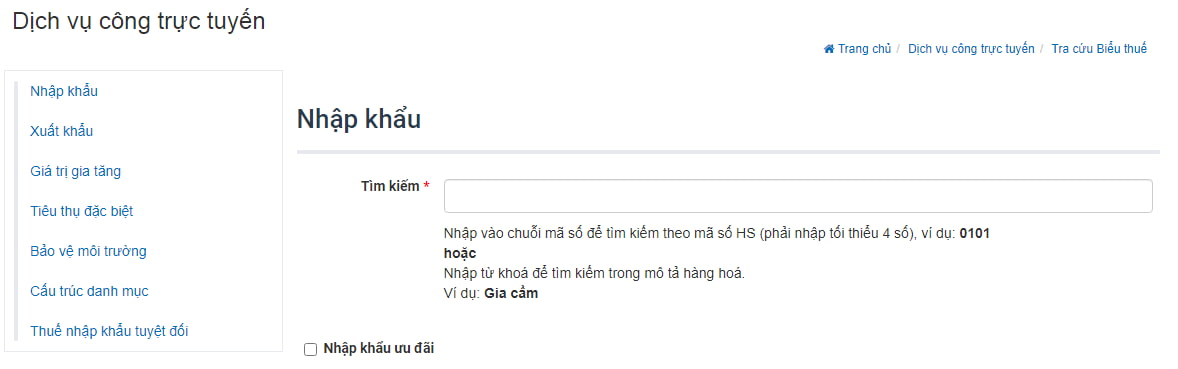

Based on the list of HS codes of goods and services when carrying out import procedures (on the customs declaration), the business establishment compares the HS codes in column 10 on the attached Appendices to determine whether goods and services are subject to VAT reduction.

HS codes can be looked up by:

Method 1: Search at the website of the General Department of Customs or search in the Appendix issued together with Circular 31/2022/TT-BTC.

The list of HS codes can be looked up from the website of the General Department of Customs by following the link: https://www.customs.gov.vn/ to look up the Tariff - HS Code.

Enter the code string to search by HS code (must enter at least 04 digits) or keyword to search in the goods description.

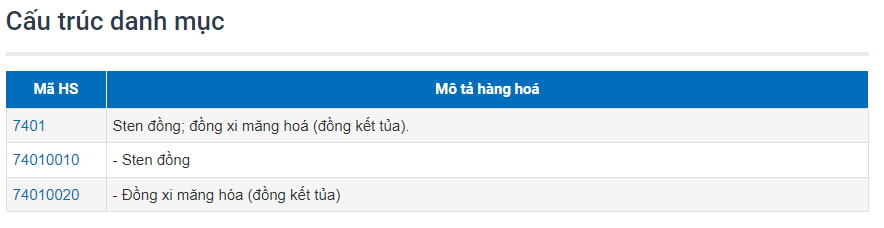

For example, a business establishment wants to import products that are Dong (with HS code 74010020).

Compare the results with Appendix I to Decree 44/2023/ND-CP:

- In case the detailed item has HS code 74010020 => compare it with column No. 10 of Appendix I attached to the Decree, this item is on the list of goods not eligible for a reduction in VAT rate of this item. ten%.

- In case of detailed goods with HS code 74010020 => compare with column No. 10 of Appendix I attached to the Decree, this item is not in the list of goods not eligible for reduction, and is entitled to a reduction of VAT to 8%.

Note: If the HS code specified in column 10 includes only Chapter 2 digits, or a group of 4 digits or 6 digits, the items with the 8-digit HS code in that Chapter or group are not eligible for tax reduction.

LawNet