Vietnam: When is the notice of expected tax rate and notice of tax payment sent to business households and business individuals?

- Form of notice of expected revenue, securities tax rate for business households and business individuals is regulated in Vietnam?

- When does the Tax Department send each household a notice of expected revenue and tax rates in Vietnam?

- When is the notice of tax payment sent to business households and individuals paying taxes in the form of securities in Vietnam?

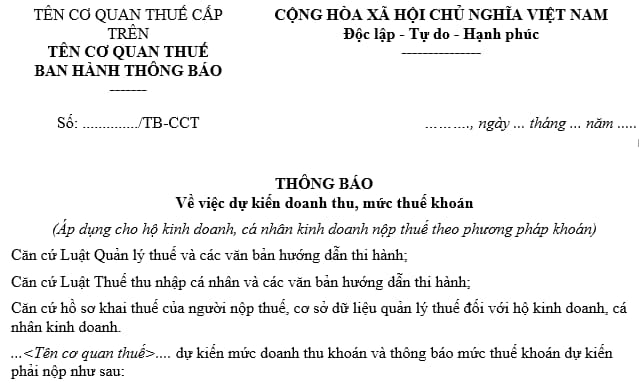

Form of notice of expected revenue, securities tax rate for business households and business individuals is regulated in Vietnam?

Currently, the notification form on the expected revenue and tax rate for business households and individuals is specified in form No. 01/TBTDK-CNKD issued together with Circular 40/2021/TT-BTC as follows:

Download the notice form about the expected revenue, and securities tax rate for business households and individuals: Here.

Vietnam: When is the notice of expected tax rate and notice of tax payment sent to business households and business individuals?

When does the Tax Department send each household a notice of expected revenue and tax rates in Vietnam?

Pursuant to Point c, Clause 5, Article 13 of Circular 40/2021/TT-BTC stipulates as follows:

Article 13. Tax administration of fixed tax payers

…

5. First information disclosure

The tax authority shall disclose information for the first time to obtain opinions about the estimated revenue and fixed tax. The following documents shall be disclosed: The list of household businesses and individual businesses exempt from VAT or PIT; the list of fixed tax payers. First information disclosure shall be carried out as follows:

…

c) By December 20 every year, the sub-department of taxation shall send to each fixed tax payer the notice of estimated revenue and tax (Form No. 01/TBTDK-CNKD) together with the information sheet (Form No. 01/CKTT-CNKD) which must specify the time and address for receiving feedbacks (if any) from the taxpayer by December 31. The notice shall be sent to the taxpayer (bearing the taxpayer’s signature confirming the receipt of the notice) or by express mail. The information sheet shall be sent to the fixed tax payers in the area, including individuals who have to pay tax and individuals who do not have to pay tax. For markets, streets, neighborhoods that have not more than 200 fixed tax payers, the sub-department of taxation shall print out the information sheets and hand them out to all fixed tax payers in the area. For markets, streets, neighborhoods that have more than 200 fixed tax payers, the sub-department of taxation shall print out the information sheets and hand them out to not more than fixed tax payers in the area. For markets that have more than 200 fixed tax payers, the sub-department of taxation shall print and hand out the information sheet according to their business lines. In case the tax authority has published the information sheet on its website, the sending of Form No. 01/CKTT-CNKD and Form No. 01/TBTDK-CNKD is not required.

Accordingly, no later than December 20 of each year, the Tax Department shall send to each household a notice of expected revenue and tax rates.

Notices are sent directly to households or sent notices by post in the form of secured delivery. The disclosure table of information expected to be sent to households is made according to the area, including individuals subject to tax payment and individuals subject to non-tax payment.

When is the notice of tax payment sent to business households and individuals paying taxes in the form of securities in Vietnam?

Pursuant to Point a, Clause 8, Article 13 of Circular 40/2021/TT-BTC, there are the following provisions on the time limit for sending notices of tax payment to business households and individuals as follows:

- The tax authority shall send the tax notice (Form No. 01/TB-CNKD enclosed with Decree No. 126/2020/ND-CP) together with the information sheet (Form No. 01/CKTT-CNKD enclosed herewith) to the fixed tax payers (whether they have to pay tax or not) by January 20 every year. The notice shall be sent directly to the taxpayer (bearing signature of the taxpayer to confirm the receipt) or by express mail.

- The official information sheet shall be sent to the fixed tax payers in the area, whether they have to pay tax or not. For markets, streets, neighborhoods that have not more than 200 fixed tax payers, the sub-department of taxation shall print out the information sheets and hand them out to all fixed tax payers in the area. For markets, streets, neighborhoods that have more than 200 fixed tax payers, the sub-department of taxation shall print out the information sheets and hand them out to not more than fixed tax payers in the area. For markets that have more than 200 fixed tax payers, the sub-department of taxation shall print and hand out the information sheet according to their business lines. In case the tax authority has published the information sheet on its website, the sending of Form No. 01/CKTT-CNKD and Form No. 01/TBTDK-CNKD is not required.

- In case the tax authority issues a notice on changes to the fixed tax as instructed by Point b Clause 3 of this Article, the notice shall be issued by the 20th of the month succeeding the month in which tax is changed.

- For new businesses, the tax authority shall send the tax notice (Form No. 01/TB-CNKD enclosed with Decree No. 126/2020/ND-CP) to the taxpayer before the 20th of the month succeeding the month in which tax is incurred.

LawNet