Vietnam: What is the partial progressive tax schedule and the full tariff of personal income tax in 2023 for resident individuals?

- Will personal income tax rates increase in Vietnam, 2023?

- What is the partial progressive tariff of personal income tax in Vietnam, 2023?

- What is the total tariff of personal income tax in Vietnam, 2023?

- Can non-resident individuals with income from wages and wages be charged PIT with a partial progressive tariff in Vietnam?

- How is the resident individual subject to the partial progressive tariff determined in Vietnam?

Will personal income tax rates increase in Vietnam, 2023?

Based on the current personal income tax calculation formula, it is based on personal taxable income and tax rates. Currently, the partial progressive tax schedule and the full tax schedule of personal income tax 2023 have not been amended by any new regulations compared to 2022.

Therefore, up to now, because the tax schedules applied in 2023 have not changed, whether the personal income tax rate in 2023 will increase or not depends on the taxable income of each individual.

In particular, it is noted that for cadres, civil servants and public employees from 01/7/2023, the salary will be increased due to the increase in base salary to 1.8 million VND/month. Therefore, the taxpayer's salary in this case increases, leading to an increase in taxable income and now the personal income tax rate in 2023 will also increase.

Vietnam: What is the partial progressive tax schedule and the full tariff of personal income tax in 2023 for resident individuals?

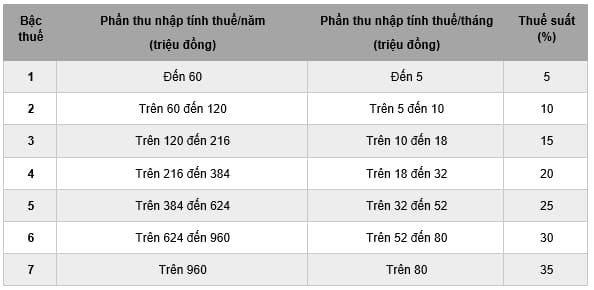

What is the partial progressive tariff of personal income tax in Vietnam, 2023?

Pursuant to Article 22 of the Law on Personal Income Tax 2007 of Vietnam, the partial progressive tax schedule is prescribed as follows:

Note: Partial progressive tax schedule is applied to taxable income on income from business, salary, wages:

Pursuant to Clause 1, Article 21 of the Law on Personal Income Tax 2007 of Vietnam as amended by Clause 5, Article 1 of the Amended Law on Personal Income Tax 2012, taxable income for income from business, wages and wages shall be determined by the total taxable income specified in Article 10 of the Law on Personal Income Tax 2007 of Vietnam (amended by Clause 4, Article 2 of the Vietnam Law on Personal Incom Tax amended 2014) and Article 11 of the Law on Personal Income Tax 2007 of Vietnam minus contributions to social insurance, health insurance, unemployment insurance, professional liability insurance for some industries and professions subject to compulsory insurance, voluntary pension fund, deductions

What is the total tariff of personal income tax in Vietnam, 2023?

Pursuant to Article 23 of the Law on Personal Income Tax 2007 of Vietnam (amending Clause 7, Article 2 of the Law on Taxation amended 2014) The full tax schedule is prescribed as follows:

Note: The full tax schedule applies to taxable income specified in Clause 2, Article 21 of the Law on Personal Income Tax 2007 of Vietnam, specifically including:

Taxable income for income from capital investment, capital transfer, real estate transfer, winning, royalties, franchises, inheritances, gifts are taxable income in accordance with the Law on Personal Income Tax 2007 of Vietnam.

Can non-resident individuals with income from wages and wages be charged PIT with a partial progressive tariff in Vietnam?

Pursuant to Chapter 2 of the Law on Personal Income Tax 2007 of Vietnam, specifically Article 22 of the Law on Personal Income Tax 2007 of Vietnam, the partial progressive tax schedule shall only be applied to resident individuals.

As for non-resident individuals, pursuant to Article 26 of the Law on Personal Income Tax 2007 of Vietnam, there are provisions on how PIT is calculated for income from wages and wages as follows:

Article 26. Tax on incomes from salaries or wages

1. Tax on income from salary or wage of a non-resident is determined to be equal to his/her income from salary or wage specified in Clause 2 of this Article multiplied by the tax rate of 20%.

2. Taxable income from salary or wage of a non-resident is the total of salary or wage amounts received by a non-resident for job performance in Vietnam, regardless of income payers.

Accordingly, tax on income from wages and wages of non-resident individuals is determined by taxable income from wages and workers' wages at a tax rate of 20%. Which is not calculated by partial progressive tariffs as for resident individuals.

How is the resident individual subject to the partial progressive tariff determined in Vietnam?

Pursuant to Clause 1, Article 1 of Circular 111/2013/TT-BTC, a resident individual is a person who satisfies one of the following conditions:

A resident is a person that meets one of the conditions below:

- He/she has been present in Vietnam for at least 183 days in a calendar year or for 12 consecutive months from the first day of his/her presence in Vietnam (the date of arrival and date of departure are considered 01 day). The date of arrival and date of departure depends on the certification of the immigration agency on the passport (or laissez-passers) when that person enters and leaves Vietnam. If the person enters and leaves Vietnam within one day, it will be considered a day of residence.

A person in Vietnam defined in this Point is the presence of that person in Vietnam’s territory.

- He/she has a regular residence in Vietnam in one of the following cases:

+ He/she has a regular residence according to regulations of law on residence:

+ For Vietnamese citizens: a place where that person regularly, stably and indefinitely lives and has been registered as a permanent residence as prescribed by regulations of law on residence.

+ For foreigners: the permanent residence written in the permanent residence card or the temporary residence when applying for the temporary residence card issued by a competent authority affiliated to the Ministry of Public Security.

+ He/she rents a house in Vietnam according to regulations of law on housing under a contract that has a term of at least 183 days in the tax year. To be specific:

+ A person who has no regular residence defined in Point b.1 Clause 1 of this Article will be considered a resident if he/she has a total house lease period of at least 183 days in the tax year under various lease contracts, even if a he/she rents houses in different locations.

+ The rented houses can be hotels, guesthouses, motels, offices, etc. whether they are rented by the person or their employer.

If the person has a regular residence in Vietnam according to this Clause but his/her actual presence in Vietnam is shorter than 183 days in the tax year and he/she fails to prove his or her residence in any country, that person will be considered a resident of Vietnam.

The residency in another country shall be proved by the Certificate of residence. If the person is a citizen of a country or territory that has signed a tax agreement with Vietnam and does not issue the Certificate of residence, that person shall present a photocopy of the passport to prove the period of residence.

LawNet