Vietnam: What is the deadline for submitting financial statements of 2023? What does the financial reporting system include currently?

What is the deadline for submitting financial statements of 2023 in Vietnam?

Under Article 109 of Circular 200/2014/TT-BTC and Clause 1, Article 80 of Circular 133/2016/TT-BTC, the deadline for submitting financial statements of 2023 in Vietnam for each enterprise is as follows:

(1) State-owned enterprises

- The accounting unit must submit annual financial statements at the latest 30 days from the end of the annual accounting period; It is at the latest 90 days for the parent companies, state-owned general companies;

For example: In case the 2023 accounting period (calendar year) of an enterprise is from January 1, 2023 to December 31, 2023, the deadline for submitting financial statements of 2023 is January 30, 2024 and March 30, 2024 (for parent companies and state corporations).

- Accounting unit-affiliated state-owned general companies submit annual financial statements to parent companies, and general companies under the time limit set by parent companies, and general companies.

(2) Other types of enterprises

- Accounting units being sole proprietorships and partnerships must submit annual financial statements at the latest 30 days from the end of annual accounting period; for other accounting units, the deadline for submission of annual financial statements is within 90 days;;

For example: In case the 2023 accounting period (calendar year) of an enterprise is from January 1, 2023 to December 31, 2023, the deadline for submitting financial statements for 2023 is January 30, 2024 (for sole proprietorships and partnerships) and March 30, 2024 (for other types of enterprises)

- Subordinate accounting unit submits annual financial statements to the superior accounting unit within the time limit given by the superior accounting units.

(3) Small and medium-sized enterprises

Every small and medium-sized enterprise shall prepare and send its financial statement within 90 days from the end of the fiscal years to relevant authorities.

For example: In case the enterprise's fiscal year according to the 2023 calendar year is from January 1, 2023 to December 31, 2023, the deadline for submitting financial statements for 2023 is March 30, 2024.

What does the financial reporting system in Vietnam include?

Under Clause 1, Article 100 of Circular 200/2014/TT-BTC, the financial reporting system in Vietnam includes:

- the Balance sheet | Form No B 01-DN |

- income statement | Form No B 02-DN |

- cash flow statement | Form No B 03-DN |

- Notes to the Financial Statements | Form No B 09-DN |

Note: Small and medium-sized enterprises that are accounting according to the Accounting Regime applicable to small and medium-sized enterprises can apply the provisions of Circular 200/2014/TT-BTC to make accounting consistent with their business characteristics and management requirements or apply the regulations in Circular 133/2016/TT-BTC.

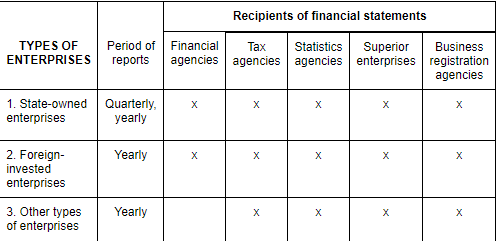

What are the recipients of the financial statements of 2023 in Vietnam?

Under Article 110 of Circular 200/2014/TT-BTC, recipients of financial statements in Vietnam are specified as follows:

- State-owned enterprises in central-affiliated cities and provinces must prepare and submit financial statements to the Service of Finance in central-affiliated cities and provinces. Central state-owned enterprises must submit financial statements to the Ministry of Finance (Department of Corporate Finance).

+ State-owned enterprises such as commercial banks, lottery companies, credit institutions, insurers, and securities trading companies must submit financial statements to the Ministry of Finance (Department of Banking and Finance or Administration of Insurance Supervision).

+ Securities trading companies and public companies must submit financial statements to the State Securities Commission and the Stock Exchange.

- Enterprises must submit financial statements to the supervisory tax authority in local. State-owned general companies must submit financial statements to the Ministry of Finance (General Department of Taxation).

- Enterprises with superior accounting units must submit financial statements to the superior accounting unit per the provisions of the superior accounting units.

- Enterprises required for financial audit by law must be audited prior to submission of financial statements in accordance with regulations. The financial statements of enterprises audited must be enclosed with the audit report when being submitted to State management agencies superior enterprises.

- The financial agency to which enterprises have foreign direct investment (FDI) must submit financial statements is the Service of Finance in central-affiliated cities and provinces where the enterprises register their main business office.

- State-owned enterprises owning 100% of the charter capital, in addition to the agencies where enterprises must submit financial statements as defined above, must also submit financial statements to the agencies, organizations assigned, decentralized to exercise rights of owners under Decree No. 99/2012 / ND-CP and documents amending, supplementing, replacing.

- Enterprises (including domestic enterprises and foreign-invested enterprises ) whose headquarters are in processing and exporting zones, industrial zones, and hi-tech zones must also submit annual financial statements to the management board of processing and exporting zones, industrial zones, and hi-tech zones if required.

Note: Circular 200/2014/TT-BTC promulgates accounting policies for enterprises in every business line and economic sector. Small and medium-sized enterprises applying the accounting policies for small and medium-sized enterprises may apply regulations in this Circular for accounting.

LawNet