Vietnam: What is an overseas supplier's electronic tax return? How to determine revenue generated in Vietnam to declare and calculate tax?

What is an overseas supplier's electronic tax return in Vietnam?

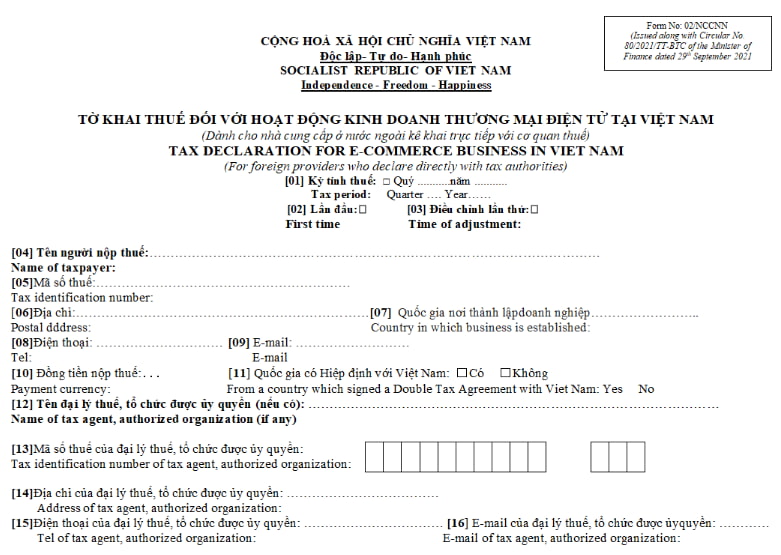

Electronic tax returns of overseas suppliers are specified in form No. 02/NCCNN issued together with Appendix I of Circular 80/2021 / TT-BTC as follows:

Download an external provider's e-tax return at: here

Vietnam: What is an overseas supplier's electronic tax return? How to determine revenue generated in Vietnam to declare and calculate tax?

How do overseas suppliers determine revenue generated in Vietnam to declare and calculate taxes in Vietnam?

Pursuant to Article 77 of Circular 80/2021/TT-BTC stipulating the contents of tax declaration and direct tax calculation of overseas suppliers as follows:

- Overseas suppliers make tax returns directly at the Portal of the General Department of Taxation, use electronic transaction authentication codes issued by tax authorities through the Portal of the General Department of Taxation and send electronic tax returns to the tax authorities directly managing them, as follows:

+ Tax return for overseas suppliers is a tax declared and paid quarterly.

+ Electronic tax declaration according to form No. 02/NCCNN issued together with Appendix I of Circular 80/2021/TT-BTC.

+ Overseas suppliers pay value-added tax and corporate income tax according to the method of ratio to revenue.

++ Value added tax revenue is the revenue received by overseas suppliers.

++ Corporate income tax revenue is revenue received by overseas suppliers.

+ The percentage to calculate value-added tax on revenue as prescribed at Point b Clause 2 Article 8 of the Government's Decree 209/2013/ND-CP dated 18/12/2013 detailing and guiding the implementation of a number of articles of the Law on Value Added Tax.

+ The percentage for calculating corporate income tax on revenue as prescribed in Clause 3 Article 11 of the Government's Decree 218/2013/ND-CP dated 26/12/2013 detailing and guiding the implementation of the Law on Corporate Income Tax.

- In case, after completing the tax declaration and payment procedures, the overseas supplier detects errors and errors, the declaration to adjust the amount of tax payable arising in Vietnam according to the form No. 02/NCCNN issued together with Appendix I of Circular 80/2021/TT-BTC.

Thus, overseas suppliers pay value-added tax and corporate income tax according to the proportional method on revenue.

In which, revenue arising in Vietnam is determined as follows:

Value added tax revenue is revenue received by overseas suppliers.

Corporate income tax revenue is revenue received by overseas suppliers.

How do overseas providers file tax returns in Vietnam?

Pursuant to Clause 3, Clause 4, Clause 5, Article 77 of Circular 80/2021 / TT-BTC stipulating the principle of determining revenue arising in Vietnam for tax declaration and calculation as follows:

First of all, the types of information used to determine transactions of organizations and individuals buying goods and services arising in Vietnam include:

+ Information related to the payment of organizations and individuals in Vietnam, such as credit card information based on bank identification number (BIN), bank account information or similar information that purchasing organizations and individuals use to pay with overseas suppliers.

+ Information about the status of residence of organizations (individuals) in Vietnam (payment address information, delivery address, home address or similar information that the purchasing organization declares to overseas suppliers).

+ Information about the access of organizations (individuals) in Vietnam, such as information about the national telephone area code of the SIM card, IP address, location of landline or similar information of the purchasing organization or individual.

- When determining a transaction arising in Vietnam for tax declaration and calculation, overseas suppliers shall do the following:

+ Use 02 non-contradictory information, including one information related to the payment of organizations (individuals) in Vietnam and one information about the status of residence or information about access of organizations and individuals in Vietnam mentioned above.

+ In case related to the payment of organizations or individuals cannot collect or contradict the remaining information, overseas suppliers are allowed to use 02 non-contradictory information including one information about residence status and one information about access of the organization, individuals in Vietnam.

At the same time, overseas suppliers use electronic transaction authentication codes directly issued by tax authorities to authenticate when declaring and adjusting.

- After the overseas supplier makes a tax declaration or adjustment declaration (if any), the tax authority directly issues and notifies the overseas supplier of the state budget payable identifier to serve as a basis for the overseas supplier to pay taxes.

- Foreign suppliers are responsible for storing information used to determine transactions of purchasing organizations and individuals arising in Vietnam as prescribed in Clause 3 of this Article for inspection and inspection by tax authorities. The storage complies with the relevant provisions of the Tax Administration Law 2019 of Vietnam.

In addition, in case an overseas supplier belongs to a country or territory that has signed a tax agreement with Vietnam, it shall carry out procedures for tax exemption and reduction under the Agreement on avoiding double taxation as prescribed in Article 62 of Circular 80/2021 / TT-BTC.

LawNet