Vietnam: What are the required documents and procedures for exemption from late tax payment interest? What are the cases in which tax late payment interest shall not be charged?

- What is the application form for exemption from late tax payment interest in Vietnam?

- What does the application for exemption from late tax payment interest in Vietnam include?

- What are the procedures for exemption from late tax payment interest in Vietnam?

- What are the cases in which tax late payment interest shall not be charged in Vietnam?

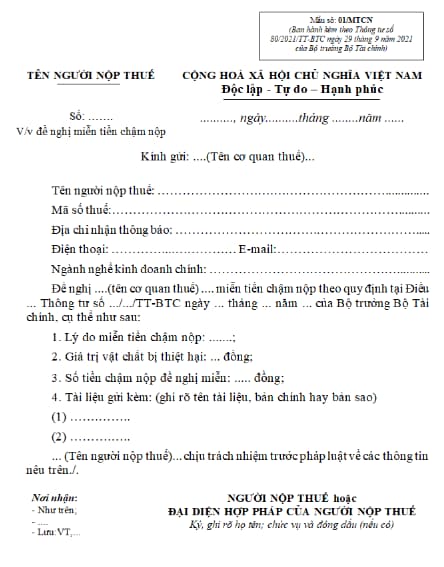

What is the application form for exemption from late tax payment interest in Vietnam?

The current application form for exemption from late tax payment interest in Vietnam is Form No. 01/MTCN issued with Circular 80/2021/TT-BTC.

Download the application form for exemption from late tax payment interest in Vietnam - Form No. 01/MTCN: here

What does the application for exemption from late tax payment interest in Vietnam include?

The application for exemption from late tax payment interest in Vietnam is specified in Clause 2, Article 23 of Circular 80/2021/TT-BTC. The application includes:

- In case of a natural disaster, epidemic, conflagration or accident, the application shall contain:

+ The application form for exemption from late tax payment interest made in Form No. 01/MTCN in Appendix I of Circular 80/2021/TT-BTC;

- Documents issued by competent authorities confirming the time, location of the natural disaster, epidemic, conflagration or accident (original copies or copies certified by the taxpayer);

- Documents determining physical damage issued by a financial authority or an independent assessing authority (original copies or certified true copies);

- Documents (original copies or copies certified by the taxpayer) attributing responsibility of specific organizations and individuals for paying compensation (if any);

- Documents (original copies or copies certified by the taxpayer) relevant to payment of compensation (if any).

- In other force majeure events specified in Clause 1 Article 3 of Decree No. 126/2020/ND-CP, the application includes:

- The application form for exemption from late tax payment interest made in Form No. 01/MTCN in Appendix I of Circular 80/2021/TT-BTC;

- Documents determining physical damage issued by a financial authority or an independent assessing authority (original copies or certified true copies) inflicted by the war, riot, or strike that caused the taxpayer to suspend or terminate business operation;

- Documents proving that the taxpayer does not subjectively cause the risk and that the taxpayer is not financially capable of making payment to state budget if that is the case (original copies or certified true copies).

- Documents (original copies or copies certified by the taxpayer) relevant to insurance payout provided by the insurer (if any).

What are the procedures for exemption from late tax payment interest in Vietnam?

According to the provisions of Clause 8, Article 59 of the Law on Tax Administration 2019, and Article 23 of Circular 80/2021/TT-BTC, the steps for processing applications for exemption from late tax payment interest in Vietnam are as follows:

Step 1: Submit the application

The taxpayer shall prepare the application for exemption of late payment interest and send it to the state budget revenue-managing tax authority.

Step 2: Process the application

- In case the application for exemption of late payment interest is not satisfactory, within 03 working days from the receipt of the application, the tax authority shall send a notification to the taxpayer and request the taxpayer to provide explanation or supplement the application.

- In case the application for exemption of late payment interest is satisfactory, within 10 working days from the receipt of the application, the tax authority shall decide whether to send a notification of exempted late payment interest if the taxpayer is eligible or send a notification of rejected application if the taxpayer is not eligible.

What are the cases in which tax late payment interest shall not be charged in Vietnam?

Under the provisions of Clause 5, Article 59 of the Law on Tax Administration 2019, tax late payment interest shall not be charged in the following cases:

+ The taxpayer provides goods/services which are covered by state budget, including sub-contractors in the contract with the investor, and are directly paid for by the investor. If such goods/services are not yet to be paid for, late payment interest will not be charged.

The outstanding tax exempt from late payment interest is the tax on the amount that is yet to be paid by state budget;

- In the following cases, late payment interest shall not be charged pending the analysis result, official price, actual payment or additional customs value:

+ Goods that need to under analysis to determine tax payable, goods without official prices when the customs declaration is registered; goods for which the payment;

+ Goods for which payments and added amounts to the customs value are unknown when the customs declaration is registered;

LawNet