Vietnam: What are the regulations on the salary and social insurance allocation table according to Circular 200 for corporate accountants?

- What is the purpose of the Salary and Social Insurance Allocation Form in Vietnam?

- What are the regulations on the form of salary and social insurance allocation table under Circular 200 for all enterprises in Vietnam?

- What are the regulations on the form of salary and social insurance allocation table under Circular 133 for small and medium-sized enterprises of Vietnam?

What is the purpose of the Salary and Social Insurance Allocation Form in Vietnam?

The form of the wage and social insurance allocation table is used to gather and distribute the actual wages payable (including wages, wages and allowances), social insurance, health insurance and trade union funds payable during the month to employers (CR 334, CR 335, CR 338 (3382, 3383, 3384, 3386).

Vietnam: What are the regulations on the salary and social insurance allocation table according to Circular 200 for corporate accountants?

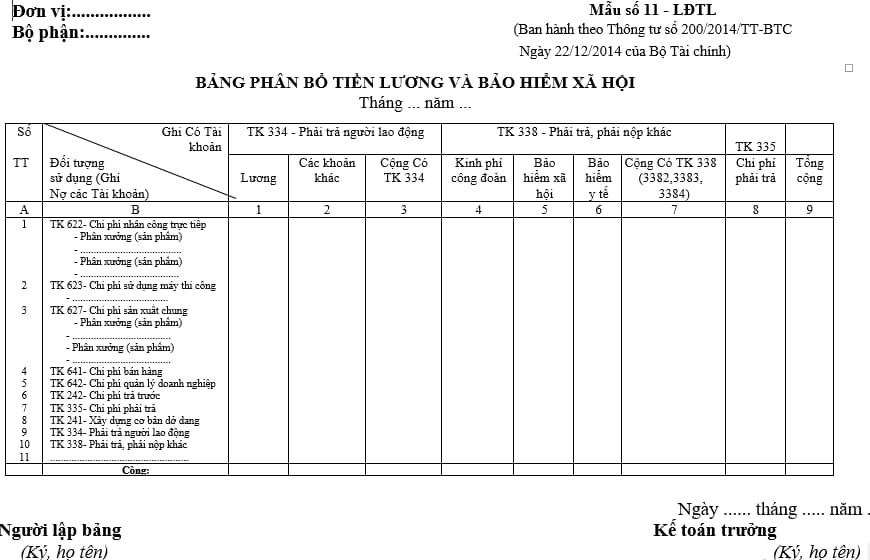

What are the regulations on the form of salary and social insurance allocation table under Circular 200 for all enterprises in Vietnam?

Currently, the form of salary allocation and social insurance for all types of enterprises is specified in Form 11-LĐTL issued together with Circular 200/2014/TT-BTC, specifically as follows:

Download the Form of salary allocation and social insurance according to Circular 200: here

Instructions for recording samples of salary allocation and social insurance according to Circular 200:

- The main structure and content of this distribution table includes vertical columns stating CR 334, CR 335, CR 338 (3382,3383,3384, 3386), horizontal lines reflecting wages, social insurance, health insurance, unemployment insurance, union funding charged to employers.

- Establishment basis:

+ Based on the tables of salary payment, night payment, overtime ... The accountant gathers and classifies documents by each object using the calculation of the amount to be recorded in this allocation table according to the appropriate lines of the column recorded CR 334 or CR 335.

+ Based on the deduction rate of social insurance, health insurance, unemployment insurance, trade union funds and the total amount of salary payable (according to current regulations) according to each user, calculate the amount to be deducted from social insurance, health insurance, unemployment insurance, trade union funds to write in the appropriate lines Cr. 338 (3382, 3383, 3384, 3386).

The data of this allocation table is used to record in statements, Diaries - Vouchers and related accounting books depending on the form of accounting applied in the unit (such as Ledger or Diary - CR 334, 338 ...), and is used to calculate the actual cost of products, service completed.

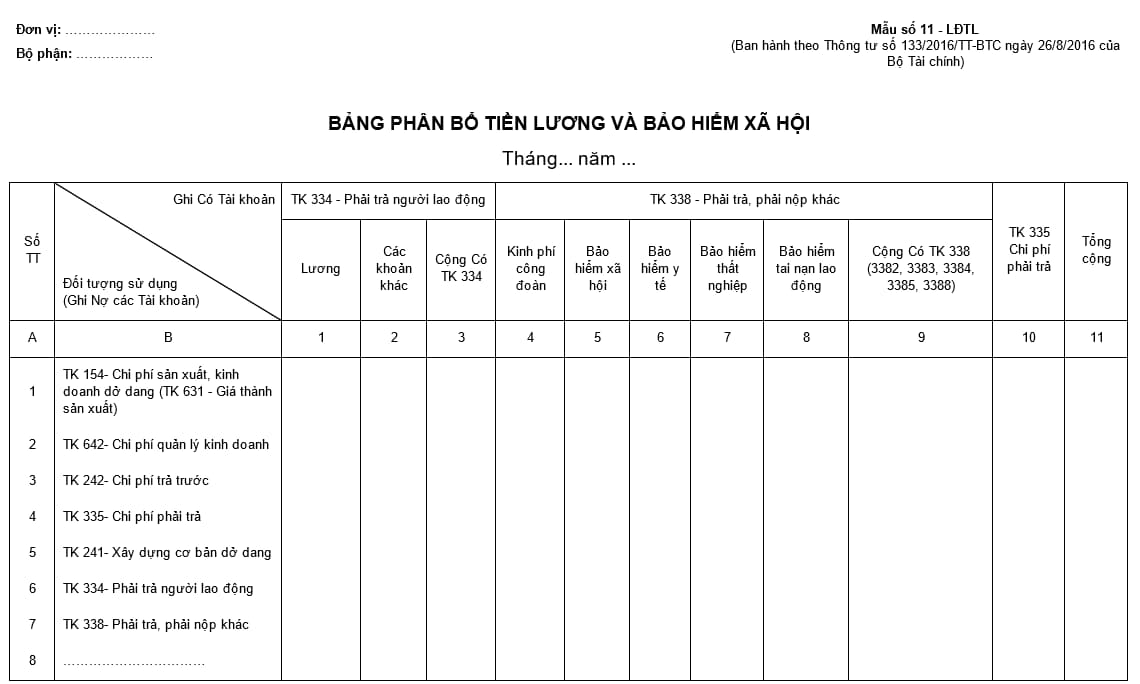

What are the regulations on the form of salary and social insurance allocation table under Circular 133 for small and medium-sized enterprises of Vietnam?

Currently, the form of salary allocation and social insurance according to Circular 133 for small and medium-sized enterprises of Vietnam is specified in Form 11-LĐTL issued together with Circular 133/2016/TT-BTC, specifically as follows:

Download the Form of salary allocation and social insurance according to Circular 133 for small and medium-sized enterprises: here

Instructions for recording samples of salary and social insurance allocation tables according to Circular 133:

- The main structure and content of this distribution table includes vertical columns indicating CR 334, CR 335, CR 338 (3382, 3383, 3384, 3385, 3888), horizontal lines reflecting wages, social insurance, health insurance, occupational accident insurance, trade union funding charged to employers.

- Establishment basis:

+ Based on the tables of salary payment, night payment, overtime ... The accountant gathers and classifies documents by each object using the calculation of the amount to be recorded in this allocation table according to the appropriate lines of the column recorded CR 334 or CR 335.

+ Based on the deduction rate of social insurance, health insurance, unemployment insurance, trade union funds and the total salary payable (according to current regulations) according to each user, calculate the amount to be deducted from social insurance, health insurance, unemployment insurance, occupational accident insurance, union funds to record in the appropriate lines CR 338 (3382, 3383, 3384, 3385, 3388).

The data of this allocation table is used to record in statements and related accounting books depending on the form of accounting applied in the unit (such as Ledger or Diary - CR 334, 338 ...), and is used to calculate the actual cost of products, service completed.

LawNet