Vietnam: What are the regulations on the fund inventory form used for VND and for foreign currencies and gold currencies under Circular 200?

- What types of fund inventory are there under Circular 200? What is the purpose of a fund inventory for a business in Vietnam?

- Sample fund inventory for VND and instructions on how to record according to Circular 200 in Vietnam?

- Sample inventory of funds used for foreign currency, gold currencies and instructions on how to record according to Circular 200 of Vietnam?

What types of fund inventory are there under Circular 200? What is the purpose of a fund inventory for a business in Vietnam?

Currently, there are two Forms of fund inventory for enterprises according to Circular 200: the inventory of funds used for VND and the inventory of funds used for foreign currencies and gold currencies. Where:

- The purpose of the fund inventory used for VND is: The fund inventory is to confirm the actual fund balance in VND and the surplus and deficiency compared to the fund book on the basis of which to strengthen fund management and serve as a basis for attributing material responsibility, recording accounting for differences.

- Purpose of inventory of funds used for foreign currency, gold currency: Minutes to confirm foreign currency, gold currency, ... Actual fund inventory and excess and deficiency compared to the fund book on the basis of which fund management is strengthened and as a basis for attributing material responsibility and accounting books for discrepancies.

Vietnam: What are the regulations on the fund inventory form used for VND and for foreign currencies and gold currencies under Circular 200?

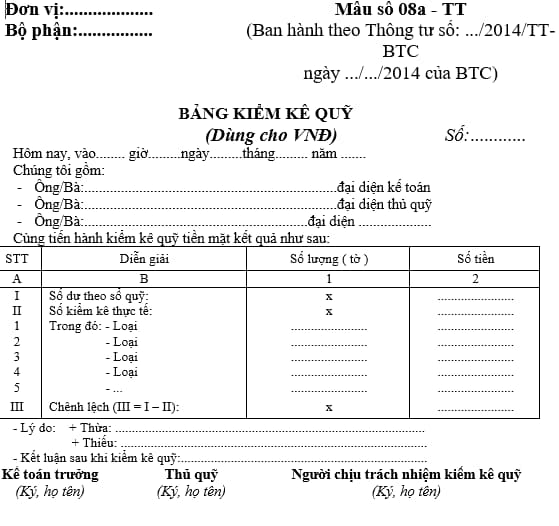

Sample fund inventory for VND and instructions on how to record according to Circular 200 in Vietnam?

Currently, the Inventory of funds for VND is specified in Form 08a-TT issued together with Circular 200/2014/TT-BTC:

Download the Fund Inventory Form for VND according to Circular 200: here

Instructions for recording an inventory of funds for use in VND according to Circular 200:

- The upper left corner of the Cash Fund Inventory Record must clearly state the name of the unit (or stamped), department.

- The inventory of funds shall be conducted periodically at the end of the month, at the end of the quarter, at the end of the year or when necessary, unscheduled inventory or upon handover of funds. When conducting an inventory, an Inventory Board must be established, of which the treasurer and cash accountant or payment accountant are members. The minutes of fund inventory must clearly state the voucher number and the time of inventory (.... hour..... day..... month..... year.....). Before taking inventory of funds, the treasurer must record all receipts and checks and calculate the balance of funds up to the time of inventory.

- When conducting an inventory, a separate inventory of each currency in the fund must be conducted.

- Line "Balance by fund book": Based on the inventory on the fund book at the date and time of adding the fund inventory to record in column 2.

- "Actual inventory" line: Based on the actual inventory to write down each currency in column 1 and calculate the total amount to write in column 2.

- Spread Line: Record the excess or missing difference between the balance in the treasury book and the actual inventory.

- On the fund inventory, it is necessary to identify and clearly state the cause of excess or lack of funds, with comments and recommendations of the Inventory Board. The fund inventory must be signed by the treasurer, the head of the inventory committee and the chief accountant. Any fund discrepancies must be reported to the director of the business for consideration.

- The fund inventory is prepared by the fund inventory board in 2 copies:

+ 1 copy saved at the cashier.

+ 1 copy saved in cash fund accounting or payment accounting.

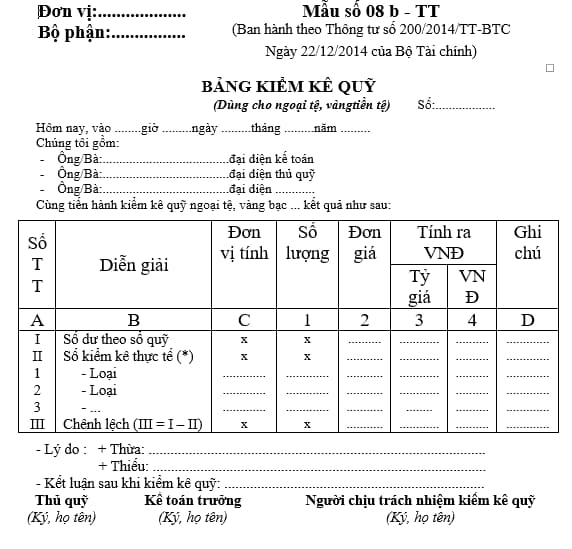

Sample inventory of funds used for foreign currency, gold currencies and instructions on how to record according to Circular 200 of Vietnam?

Currently, the Form of inventory of funds for use in foreign currencies in Vietnam and gold currencies is specified in Form 08a-TT issued together with Circular 200/2014/TT-BTC:

Download the Fund Inventory Template for foreign currencies, gold currencies according to Circular 200: here

Instructions for recording an inventory of funds intended for use in foreign currencies in Vietnam and gold currencies according to Circular 200:

- The upper left corner inscribes the name of the unit or department. The inventory of funds is conducted periodically at the end of the month, at the end of the quarter, at the end of the year or when necessary, unscheduled inventory or upon handover of funds. When conducting an inventory, an inventory board must be established, of which the treasurer and fund accountant are members.

- The fund inventory record must clearly state the voucher number and the time of inventory (... hour..... day..... month..... year.....). Before taking inventory of funds, the treasurer must record all receipts and checks and calculate the balance of funds up to the time of inventory.

- When conducting an inventory, a separate inventory of each currency in the fund must be conducted such as: Foreign currency, gold, currency ...

- Line "Balance according to the fund book": Based on the fund book at the date and time of the fund inventory to record in columns 2 and 4.

- Line "Actual inventory": Based on the actual inventory to record each type of foreign currency, gold currency ...

- Spread Line: Record the excess or missing difference between the balance in the treasury book and the actual inventory.

On the Fund Inventory, it is necessary to identify and clearly state the causes of excess or lack of funds, with comments and recommendations of the Inventory Board. The fund inventory must bear the signatures (full name) of the treasurer, head of the inventory department and chief accountant. Any fund discrepancies must be reported to the director of the business for consideration.

- The fund inventory is prepared by the fund inventory board in 2 copies:

+ 1 copy saved at the cashier

+ 1 copy saved in the fund accountant.

LawNet