Vietnam: What are the instructions on looking up the tariff schedules for imported goods (preferential import duty, import duty)?

Vietnam: What are the instructions on looking up the tariff schedules for imported goods?

To conduct a lookup of the tariff schedules for imported goods, individuals and organizations need to follow the following steps:

Step 1: Access the lookup system of tariff schedules for goods on the public service portal of the General Department of Customs at https://www.customs.gov.vn/index.jsp?pageId=24&id=NHAP_KHAU&name =Nh%E1%BA%ADp%20kh%E1%BA%A9u&cid=1201

Step 2: After accessing the lookup system of tariff schedules for goods of the General Department of Customs, the organization or individual selects the item Import.

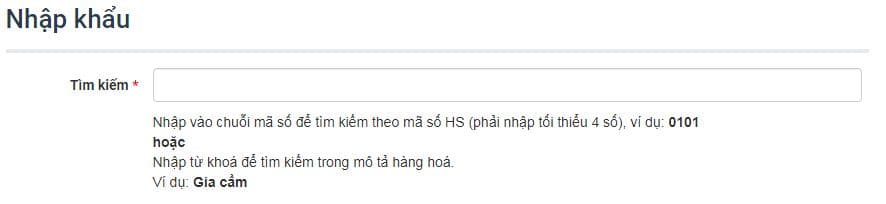

Step 3: At this point, the Search box will appear on the website interface. Organizations and individuals need to enter the search code string according to the HS code or the keyword describing the goods to conduct the search results.

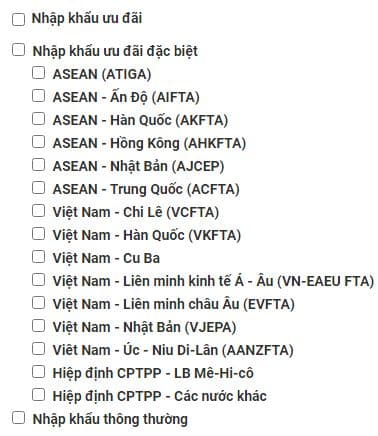

Step 4: After entering the keyword or HS code, the organization or individual determines which import tax rate they want to find (preferential import duty, special preferential import duty or import duty) and select that import tax category.

Step 5: Enter the capcha code displayed on the interface and select Search to see the results.

Above is a guide on how to look up the tariff schedules for imported goods today.

Vietnam: What are the instructions on looking up the tariff schedules for imported goods (preferential import duty, import duty)?

What are taxed goods in Vietnam?

Pursuant to Article 2 of the Law on Import and Export Duties 2016 stipulates as follows:

Taxed goods

1. Goods exported and imported through Vietnam’s border and border checkpoints.

2. Goods exported from the domestic market into free trade zones; goods imported from free trade zones into the domestic market.

3. Goods indirectly exported-imported; goods exported and imported by enterprises exercising their right to export, import, or distribute.

4. The following goods do not incur export and import duties:

a) Goods in transit;

b) Goods that are humanitarian aid or grant aid;

c) Goods exported from a free trade zone to abroad; goods imported from abroad to a free trade zone and used within such free trade zone; goods transported from one free trade zone to another;

d) Amounts of petroleum used as severance tax paid to the State upon its exportation.

5. The Government shall regulate this Article.

According to the above provisions, the following subjects are subject to import tax:

- Goods imported through Vietnam's border gates or borders

- Goods imported on the spot, goods imported by enterprises exercising the right to export.

In addition, the above regulation also stipulates the subjects that are not subject to import tax as follows:

- Goods in transit;

- Goods that are humanitarian aid or grant aid;

- Goods imported from abroad to a free trade zone and used within such free trade zone.

Who are the import taxpayers in Vietnam?

Pursuant to Article 3 of the Law on Import and Export Duties 2016 stipulates on import and export taxpayers as follows:

- Owners of exports and imports.

- Entrusted exporters and importers.

- People entering and leaving Vietnam carrying exports or imports, sending or receiving goods through Vietnam’s border and border checkpoints.

- Taxpayers’ guarantors and other entities authorized to pay tax on behalf of taxpayers, including:

+ Customs brokerage agents in case authorized by the taxpayer to pay export and import duties;

+ Providers of postal services or international express mail services paying tax on behalf of taxpayers;

+ Credit institutions or other organizations operating under the Law on credit institutions that provide guarantee or pay tax on behalf of taxpayers;

+ People authorized by goods owners in case goods are gifts of individuals; any luggage sent before or after its owner’s arrival or departure;

+ Any branch of an enterprise authorized to pay tax on its behalf;

+ Other people authorized to pay tax on behalf of taxpayers as prescribed by law.

- Any person who purchases or transports goods within the tax-free allowance applied to border residents which are sold domestically instead of being consumed or used for manufacture; foreign traders permitted to deal in exports and imports at bordering markets as prescribed by law.

- Owners of exports or imports that are initially tax-free but then taxed.

- Other cases prescribed by law.

LawNet