Vietnam: What are the instructions for making tax declaration appendix for CIT paid overseas according to form 03-4/TNDN?

Vietnam: When will Form No. 03-4/TNDN be used?

In case there is corporate income tax in Vietnam already paid abroad, the taxpayer must additionally submit Appendix form No. 03-4/TNDN together with the CIT declaration form No. 03/TNDN specified in Appendix II enclosed herewith Circular 80/2021/TT-BTC.

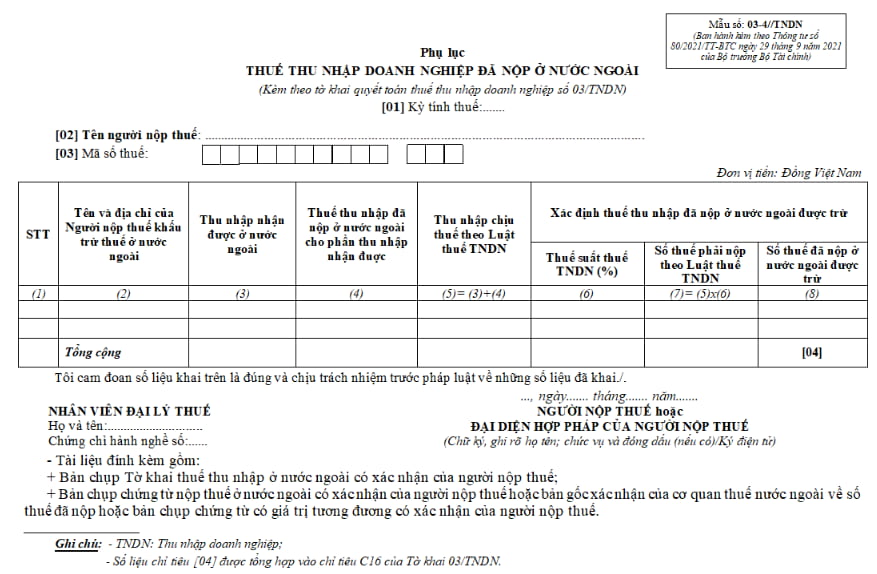

Form No. 03-4/TNDN has the following form:

Download form number 03-4/TNDN here: download

Vietnam: What are the instructions for making tax declaration appendix for CIT paid overseas according to form 03-4/TNDN?

Vietnam: What are the instructions for making tax declaration appendix for CIT paid overseas according to form 03-4/TNDN?

The deductible income tax amount is the amount of income tax actually paid abroad on the income distributed to a Vietnamese enterprise based on tax payment documents but does not exceed the income tax amount calculated according to the provisions of the Law on corporate income tax in 2008.

The amount of income tax that a Vietnamese enterprise investing abroad is exempted or reduced on the profits enjoyed from the investment project abroad according to the law of the country where the enterprise invests is also deductible when determining the CIT payable in Vietnam.

In case the income received from abroad has signed the Agreement on avoidance of double taxation with the Socialist Republic of Vietnam with other provisions on how to determine the deductible tax amount, the provisions of that Agreement shall apply.

Business establishments determine the amount of income tax already paid abroad to be deducted according to the specific contents in Appendix 03-4/TNDN issued together with the CIT finalization declaration.

Target [01]: Specify the year tax period in accordance with the tax period on declaration 03/TNDN.

Targets [02], [03]: Taxpayer's name and tax identification number match the information on declaration 03/TNDN. If taxpayers make an electronic tax declaration, the Etax system automatically supports displaying this information from the taxpayer's information declared on declaration 03/TNDN.

Column (1): The taxpayer writes the serial number according to each income received abroad.

Column (2): The taxpayer records the name and address of the Taxpayer withholding tax in a foreign country such as information on subsidiaries and affiliates in foreign countries.

Column (3): The taxpayer declares the income received abroad as the part of the income that the taxpayer actually received and remitted in the tax period.

Column (4): The taxpayer declares the amount of income tax paid abroad corresponding to the income received declared in column (3).

Column (5): The taxpayer declares taxable income according to the Law on CIT. Column criteria (5) = column (3) + column (4).

Column (6): The taxpayer declares the CIT rate of 20%.

Column (7): The taxpayer declares the payable CIT amount according to the Law on CIT (7) = (5) x (6).

Column (8): The taxpayer declares the amount of CIT paid overseas to be deducted in the tax period. The amount of CIT paid overseas that can be deducted must not exceed the amount of CIT payable under the CIT Law determined in column (7). The total of column (8) = indicator [04] is aggregated to indicator [C16] on declaration 03/TNDN.

Is corporate income tax in Vietnam deductible?

Pursuant to Article 48 of Circular 205/2013/TT-BTC mentioned as follows:

In case a resident of Vietnam has income and has paid tax in the Contracting State to an Agreement concluded with Vietnam, if in the Agreement, Vietnam commits to tax withholding measures, when this resident declare income tax in Vietnam, such income shall be included in the taxable income in Vietnam in accordance with the provisions of the tax laws in force in Vietnam and the tax paid in the Contracting State will be deducted from tax payable in Vietnam.

Tax deductions are made according to the following principles:

- The tax paid in a Contracting State to be deducted is the tax provided for in the Agreement;

- The tax withheld does not exceed the tax payable in Vietnam on income from the Contracting State in accordance with the current tax laws in Vietnam, but it is also not allowed to withhold or refund the higher paid tax amount in another country;

- The tax paid in the Contracting State to be deductible is the tax incurred during the tax year in Vietnam.

At the same time, based on Clause 1, Article 3 of Circular 78/2014/TT-BTC (amended and supplemented with Article 1 of Circular 96/2015/TT-BTC) guiding the deduction of CIT as follows:

- In case an income earned from an overseas project has incurred CIT (or a similar tax) overseas, the Vietnamese ODI enterprise may deduct the tax paid by the enterprise overseas or by the foreign partner (including tax on dividends) from the amount of CIT payable in Vietnam.

Nevertheless, the deducted tax must not exceed the amount of CIT calculated under the Law on CIT of Vietnam. Reduction or exemption of CIT on profit from the overseas project under the host country’s law will also be deducted from the amount of CIT payable in Vietnam.

Pursuant to Article 4 of Circular 96/2015/TT-BTC amending and supplementing Article 6 of Circular 96/2015/TT-BTC guiding corporate income tax, stipulating deductible and non-deductible expenses when determining taxable income:

...

1. Except for the non-deductible expenses prescribed in Clause 2 of this Article, every expense is deductible if all of these following conditions are satisfied:

a) The actual expense incurred is related to the enterprise’s business operation.

b) There are sufficient and valid invoices and proof for the expense under the regulations of the law.

c) There is proof of non-cash payment for each invoice for purchase of goods/ services of VND 20 million or over (including VAT).

…

2. The expenses below are not deductible when calculating taxable income:

…

2.37. Input VAT that has been deducted or refunded; input VAT of fixed assets being cars for the transport of 9 persons or fewer that exceeds the deductible limit prescribed in legislative documents on VAT; CIT other than CIT paid by the enterprise on behalf of the foreign contractor under the main contract which stipulates that the revenue earned by the foreign contractor and sub-contractors is exclusive of CIT; personal income tax unless the employment contract states that employees’ salaries are exclusive of personal income tax

Accordingly, when the enterprise has been subject to corporate income tax (or a tax of a similar nature to corporate income tax) abroad, based on the dossiers and documents proving the paid income tax amount overseas and deducted from the CIT payable in Vietnam corresponding to the revenue recorded in Vietnam.

In case the enterprise cannot determine the amount of CIT paid overseas to be deductible in Vietnam, the entire CIT amount paid abroad is determined to be a non-deductible expense when determining taxable income.

LawNet