Vietnam: What are the guidelines for authenticating OTP for Single sign-on control with VSSID application according to Official Dispatch 836/BHXH-CNTT?

- Vietnam: What are the guidelines for authenticating OTP for Single sign-on control with VSSID application according to Official Dispatch 836/BHXH-CNTT?

- Who are the participants of compulsory social insurance in Vietnam?

- What are the levels and methods of payment by employees covered by compulsory social insurance in Vietnam?

Vietnam: What are the guidelines for authenticating OTP for Single sign-on control with VSSID application according to Official Dispatch 836/BHXH-CNTT?

On March 26, 2024, the Vietnam Social Security (BHXH) issued Official Dispatch 836/BHXH-CNTT 2024 to provide guidance on implementing OTP authentication for Single sign-on (SSO) control.

Pursuant to the Appendix accompanying Official Dispatch 836/BHXH-CNTT 2024, the OTP authentication instructions are as follows:

(1) Check information on the I-AM system

Step 1: Log in to https://user.baohiemxahoi.gov.vn

Step 2: Check the social security number in the Account Information section.

(2) Upgrade VssID software to version 1.6.8

The minimum version of the VssID application should be 1.6.8 (for iOS devices, update from the App Store; for Android devices, update from Google Play).

(3) How to receive OTP code from VssID

Step 1: Log in to the SSO system with your account and password.

Step 2: After successful login in Step 1, the system will automatically switch to the OTP code input screen.

Step 3: On your phone, the VssID app will display a notification.

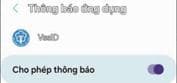

In case the notification is not displayed, you can still log in to VssID to retrieve the OTP code after successfully logging in to Step 1 and the OTP input screen is displayed. If you want the notification to be displayed, you need to grant permission for app notifications in your phone settings.

Step 4: SSO authentication code screen.

If you accidentally close the SSO authentication code screen without memorizing it, you can log out of VssID and log in again to display the information (note: the OTP is valid for 2 minutes).

Step 5: The user enters the OTP code on the OTP input screen of the SSO system in Step 2.

Vietnam: What are the guidelines for authenticating OTP for Single sign-on control with VSSID application according to Official Dispatch 836/BHXH-CNTT?

Who are the participants of compulsory social insurance in Vietnam?

Pursuant to the provisions of Article 2 of the Law on Social Insurance 2014, participants of compulsory social insurance include:

(1) Employees:

- Employees being Vietnamese citizens shall be covered by compulsory social insurance, including:

+ Persons working under indefinite-term labor contracts, definite-term labor contracts, seasonal labor contracts or contracts for given jobs with a term of between full 3 months and under 12 months, including also labor contracts signed between employers and at-law representatives of persons aged under 15 years in accordance with the labor law;

+ Persons working under labor contracts with a term of between full 1 month and under 3 months;

+ Cadres, civil servants and public employees;

+ Defense workers, public security workers and persons doing other jobs in cipher organizations;

+ Officers and professional army men of the people's army; officers and professional non-commissioned officers and officers and technical non- commissioned officers of the people's public security; and persons engaged in cipher work and enjoying salaries like army men;

+ Non-commissioned officers and soldiers of the people’s army; non- commissioned officers and soldiers on definite-term service in the people’s public security; army, public security and cipher cadets who are entitled to cost- of-living allowance;

+ Vietnamese guest workers defined in the Law on Vietnamese Guest Workers;

+ Salaried managers of enterprises and cooperatives;

+ Part-time staffs in communes, wards and townships.

- Employees who are foreign citizens working in Vietnam with work permits or practice certificates or practice licences granted by competent Vietnamese agencies shall be covered by compulsory social insurance under the Government’s regulations.

(2) Employers:

Employers covered by compulsory social insurance include:

- State agencies, non-business units and people's armed forces units;

- Political organizations, socio-political organizations, socio-politico-professional organizations, socio-professional organizations and other social organizations;

- Foreign agencies and organizations, and international organizations operating in the Vietnamese territory;

- Enterprises, cooperatives, individual business households, cooperative groups, and other organizations and individuals that hire or employ employees under labor contracts.

What are the levels and methods of payment by employees covered by compulsory social insurance in Vietnam?

Pursuant to the provisions of Article 85 of the Law on Social Insurance 2014, the levels and methods of payment by employees covered by compulsory social insurance are as follows:

- Employees defined at Points a, b, c, d, dd and h, Clause 1, Article 2 of Law on Social Insurance 2014 shall monthly pay 8% of their monthly salary to the retirement and survivorship allowance fund.

Employees defined at Point i, Clause 1, Article 2 of Law on Social Insurance 2014 shall monthly pay an amount equal to 8% of the statutory pay rate to the retirement and survivorship allowance fund.

- For employees defined at Point g, Clause 1, Article 2 of Law on Social Insurance 2014, the levels and methods of payment are specified as follows:

+ The monthly level of payment to the retirement and survivorship allowance fund must equal 22% of employees’ monthly salary on which social insurance premiums are based before they go abroad to work, for employees who have paid compulsory social insurance premiums in a certain period; 22% of 2 times the statutory pay rate, for employees who are not yet covered by compulsory social insurance or who have paid compulsory social insurance premiums and have already received a lump-sum social insurance allowance.

+ Payment shall be made once every 3 months, every 6 months or every 12 months or in a lump sum within the time limit stated in the contracts on sending of employees to work abroad. Employees may make payment directly to social insurance agencies of localities where they reside before going abroad or via enterprises or non-business organizations that have sent them to work abroad.

In case the payment is made via enterprises or non-business organizations that have sent employees to work abroad, these enterprises or organizations shall collect and pay social insurance premiums for employees and register the method of payment with social insurance agencies.

Employees who have their contracts extended or sign new contracts in the host countries shall pay social insurance premiums according to the method specified in this Article or shall retrospectively pay social insurance premiums to social insurance agencies after they repatriate.

- Employees who neither work nor receive salary for 14 working days or more in a month are not required to pay social insurance premiums in that month. This period shall not be counted for enjoyment of social insurance benefits, except cases of maternity leave.

- An employee defined at Point a or b, Clause 1, Article 2 of Law on Social Insurance 2014 who signs labor contracts with many employers shall only pay social insurance premiums under Clause 1 of Article 85 of Law on Social Insurance 2014 for the first-signed labor contract.

- Employees who enjoy product-based or piecework-based salaries at enterprises, cooperatives, individual business households or cooperative groups engaged in the fields of agriculture, forestry, fishery or salt making shall pay monthly social insurance premiums at the levels specified in Clause 1 of Article 85 of Law on Social Insurance 2014; payment may be made every month, every 3 months or every 6 months.

- The determination of the period of social insurance premium payment for enjoyment of pension and monthly survivorship allowance must adhere to the principle that one year has full 12 months; an employee who satisfies the age requirement for pension enjoyment but whose period of social insurance premium payment is short of 6 months at most may pay a lump-sum amount for these months with the monthly premium equal to the total premiums paid by him/her and his/her employer to the retirement and survivorship allowance fund, based on the monthly salary on which social insurance premiums were based before he/she ceases working.

- The calculation of periods of social insurance premium payment with odd months for enjoyment of the retirement and survivorship allowance benefits must be as follows:

+ A period of between 1 month to 6 months shall be counted as half year;

+ A period of between 7 months to 12 months shall be counted as one year.

Thư Viện Pháp Luật