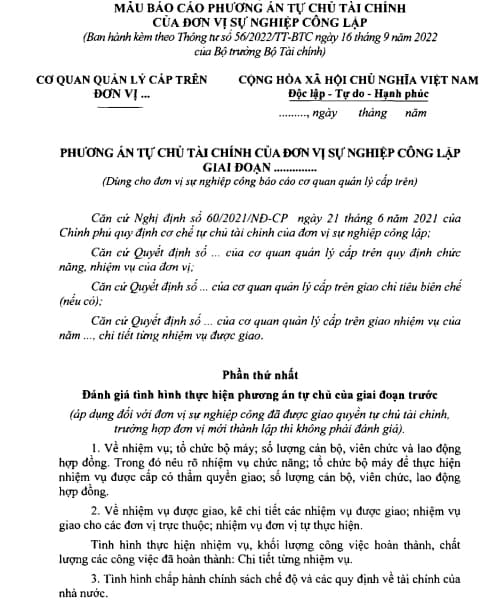

Vietnam: The latest form of financial autonomy plan of a public non-business unit in 2022 according to Circular 56/2022 / TT-BTC?

- Latest sample of report on financial autonomy plan of public non-business units in Vietnam 2022 according to Circular 56/2022 / TT-BTC?

- Determining the level of self-assurance of recurrent expenditures for public non-business units in the field of training and education in Vietnam?

- Determining the level of self-assurance of recurrent expenditure for public career units in the health sector in Vietnam?

Latest sample of report on financial autonomy plan of public non-business units in Vietnam 2022 according to Circular 56/2022 / TT-BTC?

Pursuant to the provisions of Appendix 2 issued together with Circular 56/2022 / TT-BTC, the form of reporting on the financial autonomy plan of the public non-business unit is as follows:

View details and download a sample of the public non-business unit's financial autonomy plan report: Here.

Vietnam: The latest form of financial autonomy plan of a public non-business unit in 2022 according to Circular 56/2022 / TT-BTC?

Determining the level of self-assurance of recurrent expenditures for public non-business units in the field of training and education in Vietnam?

Pursuant to the provisions of Article 5 of Circular 56/2022 / TT-BTC, the following provisions:

- Revenues determining the level of financial autonomy (A) of the unit are the total revenues specified at Point a, Clause 2, Article 4 of this Circular, including:

+ Tuition fee revenue sources as prescribed in Decree 81/2021/ND-CP on the mechanism of tuition collection and management for educational institutions under the national education system and policies on tuition fee exemption and reduction, support for study costs; service prices in the field of education and training;

+ The state budget shall provide compensation for vocational education and training institutions to implement the tuition fee exemption and reduction policy specified in Decree 81/2021/ND-CP (based on the actual number of people studying and expected to recruit new ones at the time of formulating the plan to determine the unit's self-assurance of recurrent expenditure);

+ Revenues from the provision of public career services on the list of state-funded public career services in the field of education, training and vocational education (including revenues from the state budget for ordering or bidding for the provision of public career services as prescribed).

- Expenditures determining the level of financial autonomy (B) of the unit are the total expenditures as prescribed at Point b Clause 2 Article 4 of Circular 56/2022 / TT-BTC.

In addition, a specific example of the determination of self-assurance of recurrent expenditures of public non-business units in the field of education, training and vocational education is in Section A of Appendix No. 1 issued together with Circular 56/2022 / TT-BTC.

See for example the determination of self-assurance of recurrent expenditures of public non-business units in the field of education, training and vocational education in: Section A of Appendix No. 1 issued together with Circular 56/2022 / TT-BTC

Determining the level of self-assurance of recurrent expenditure for public career units in the health sector in Vietnam?

According to the provisions of Article 6 of Circular 56/2022 / TT-BTC, public non-business units in the field of health - population determine the level of self-assurance of recurrent expenditures as prescribed in Article 4 of Circular 56/2022 / TT-BTC and the following provisions:

- Revenues determining the level of financial autonomy (A) of the unit are the total revenues specified at Point a, Clause 2, Article 4 of this Circular, including:

+ Revenue from medical examination and treatment services shall be paid by the Health Insurance Fund and from patients as prescribed;

+ Revenues from the provision of public career services on the list of state-funded public career services in the field of health and population (including revenues from the state budget for ordering or bidding for the provision of public career services as prescribed).

- Expenditures determining the level of financial autonomy (B) of the unit are the total expenditures as prescribed at Point b, Clause 2, Article 4 of this Circular.

Accordingly, a specific example of the determination of self-assurance of recurrent expenditures of public non-business units in the field of health and population is in Section B of Appendix No. 1 issued together with Circular 56/2022 / TT-BTC.

See for example the determination of self-assurance of recurrent expenditures of public non-business units in the field of health - population at: Section B of Appendix No. 1 issued together with Circular 56/2022 / TT-BTC.

LawNet