Vietnam: Summary of 2023 value-added tax invoice templates? What should be noted about when to invoice VAT in 2023?

What is a value-added invoice in Vietnam?

Value-added invoices are defined in Clause 1 Article 8 of Decree 123/2020/ND-CP which can be understood as invoices for organizations filing value-added tax according to the deduction method used for activities:

- Domestic sale of goods or provision of services;

- Provision of international transport services;

- Export of goods to free trade zones and other cases considered as export of goods;

- Export of goods or provision of services in a foreign market.

Vietnam: Summary of 2023 value-added tax invoice templates? What should be noted about when to invoice VAT in 2023?

Summary of value added tax invoices in 2023 in Vietnam?

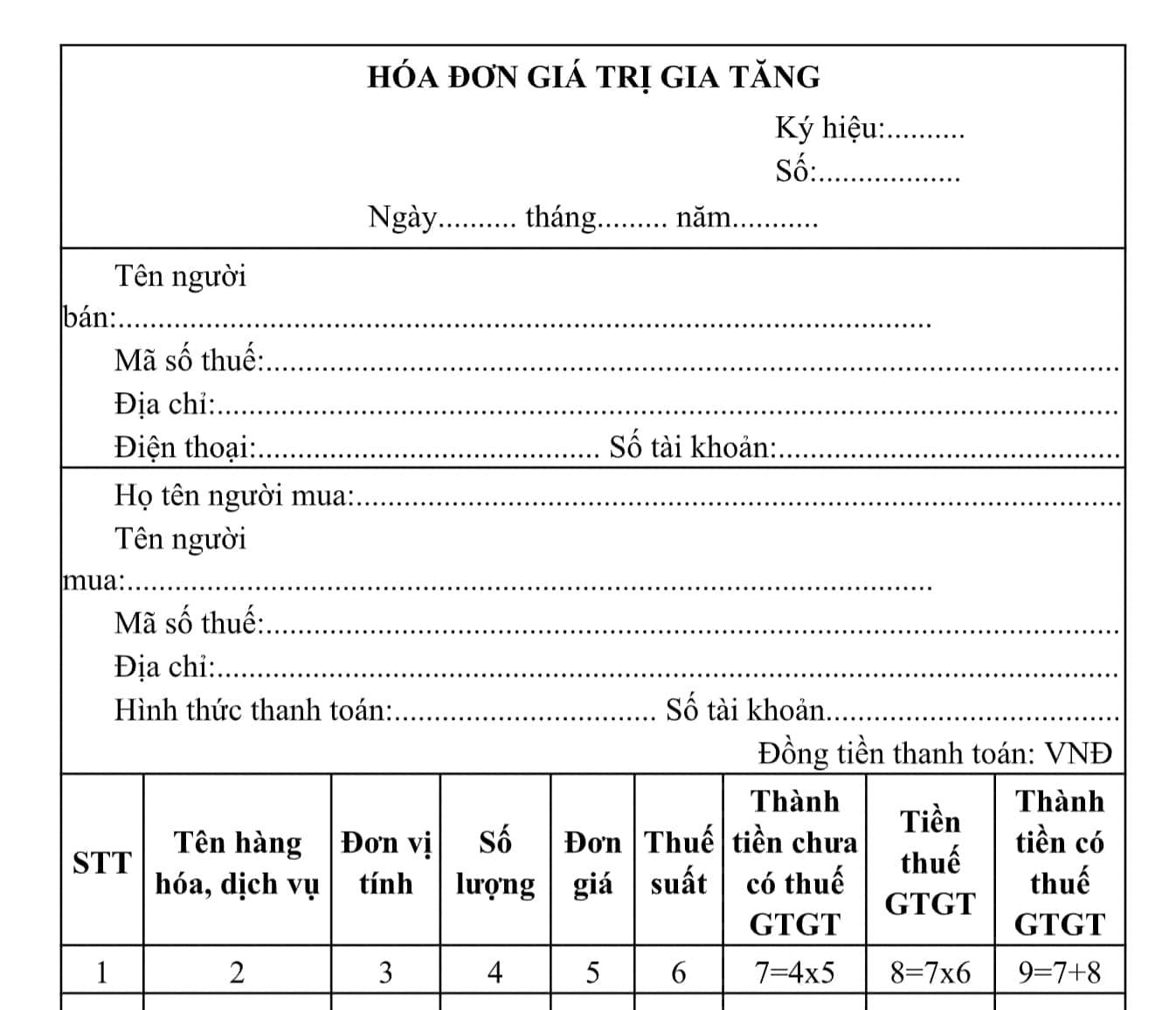

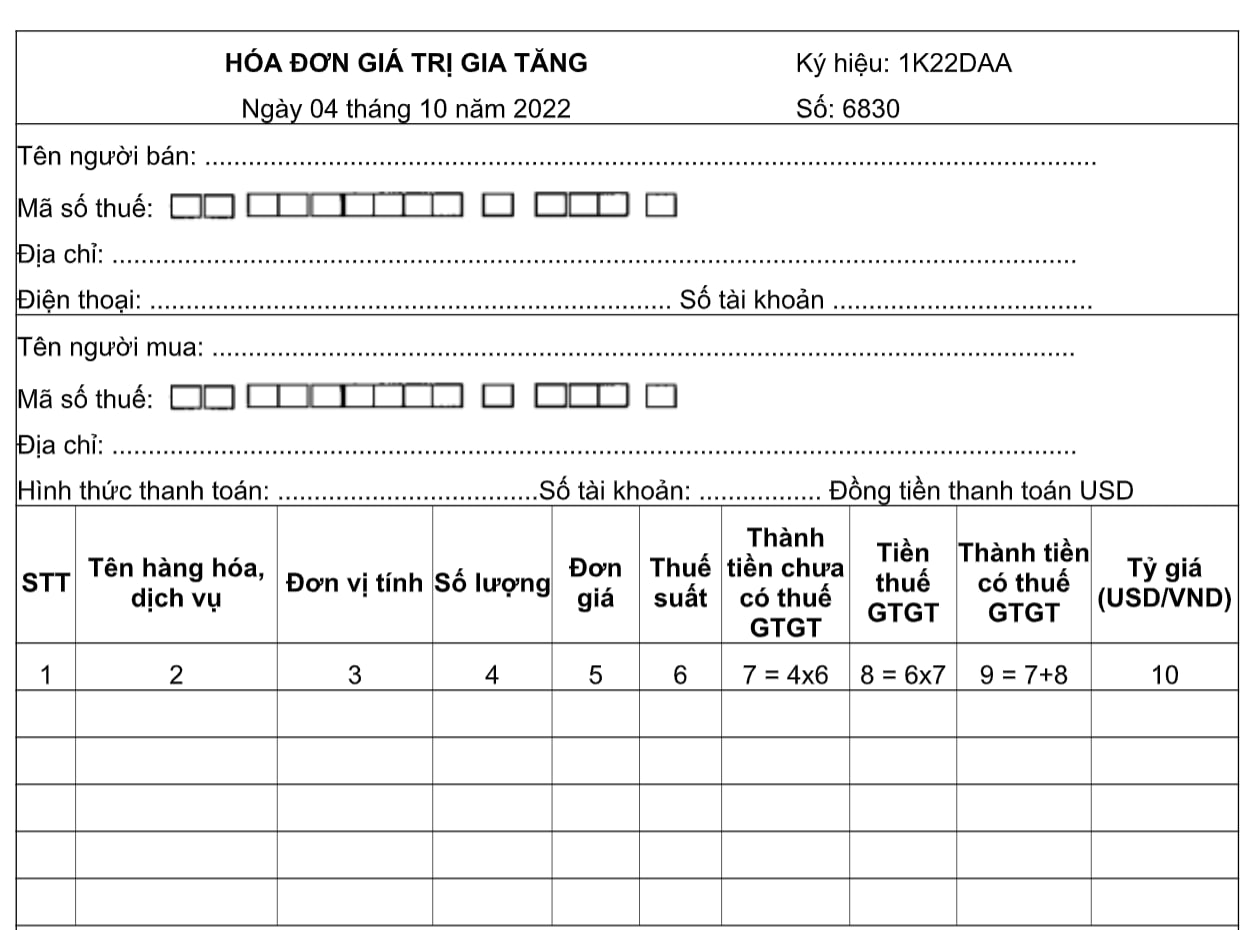

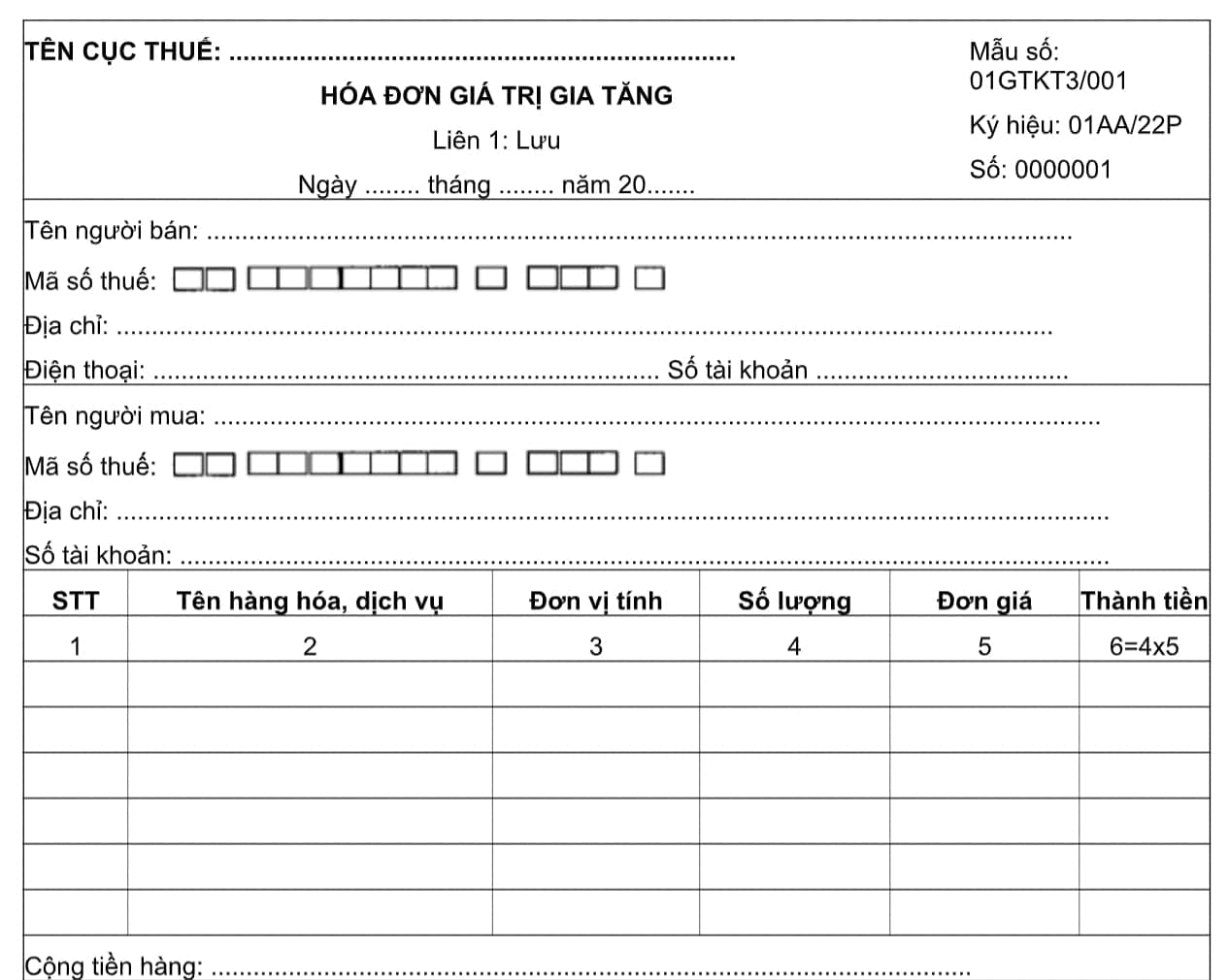

The value-added invoice form specified in Appendix II issued together with Circular 78/2021/TT-BTC and the Appendix issued together with Decree 123/2020/ND-CP includes:

Form No. 01/VAT Appendix issued together with Decree 123/2020/ND-CP:

Download Form No. 01/VAT here

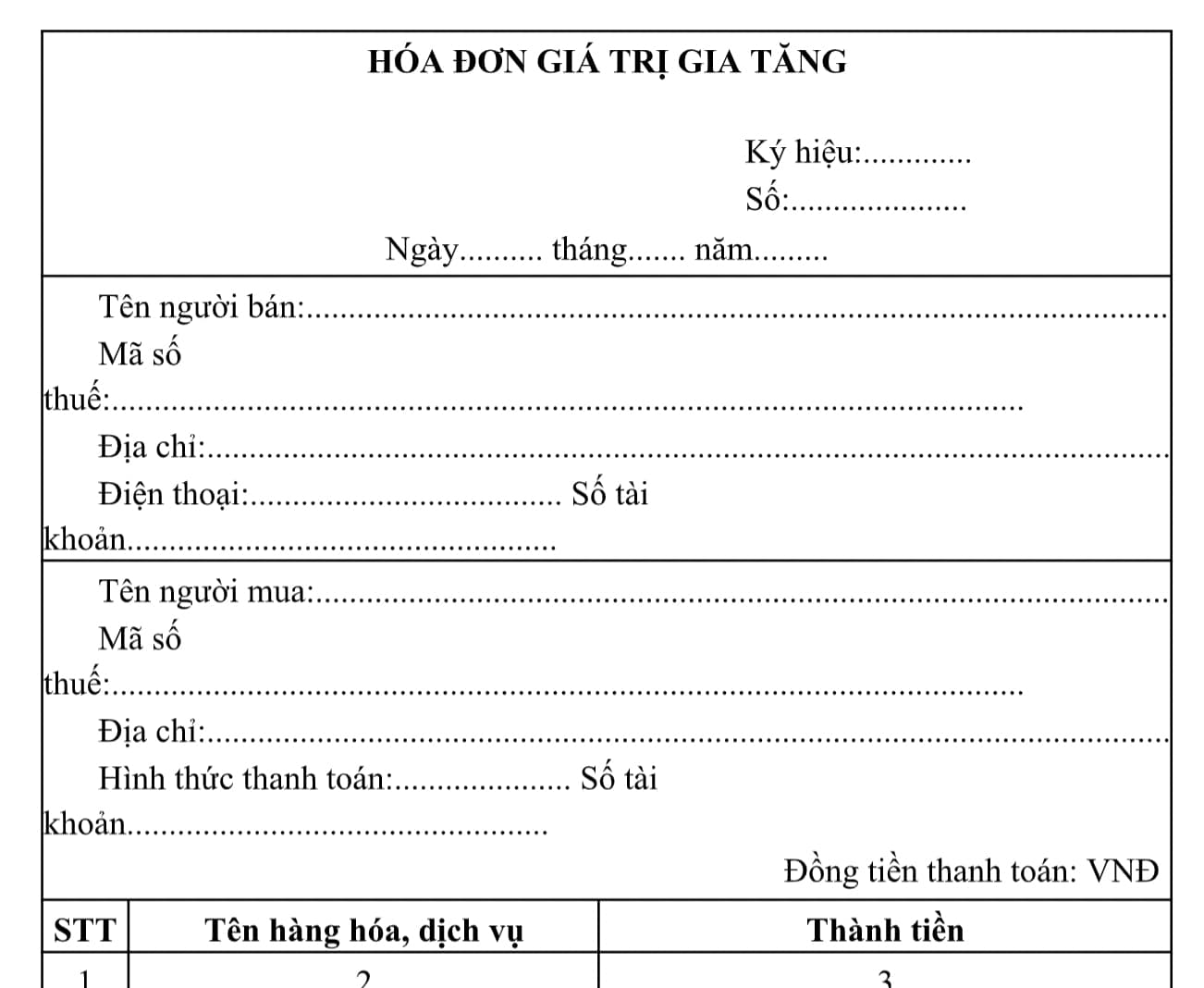

Form No. 01/VAT-DT Appendix issued together with Decree 123/2020/ND-CP

Download Form No. 01/VAT here

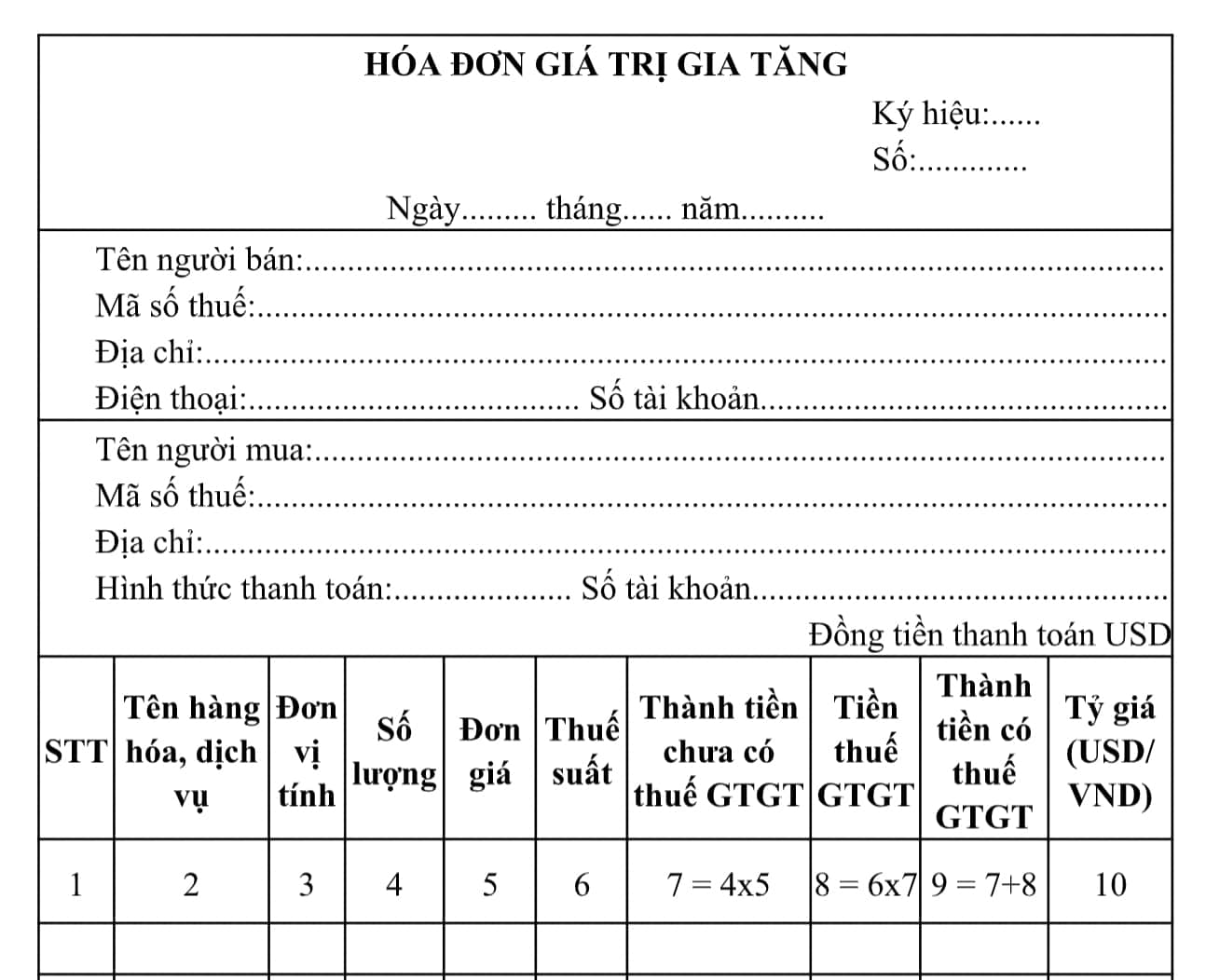

Form No. 01/VAT -NT Appendix issued together with Decree 123/2020/ND-CP:

Download Form No. 01/VAT NT here

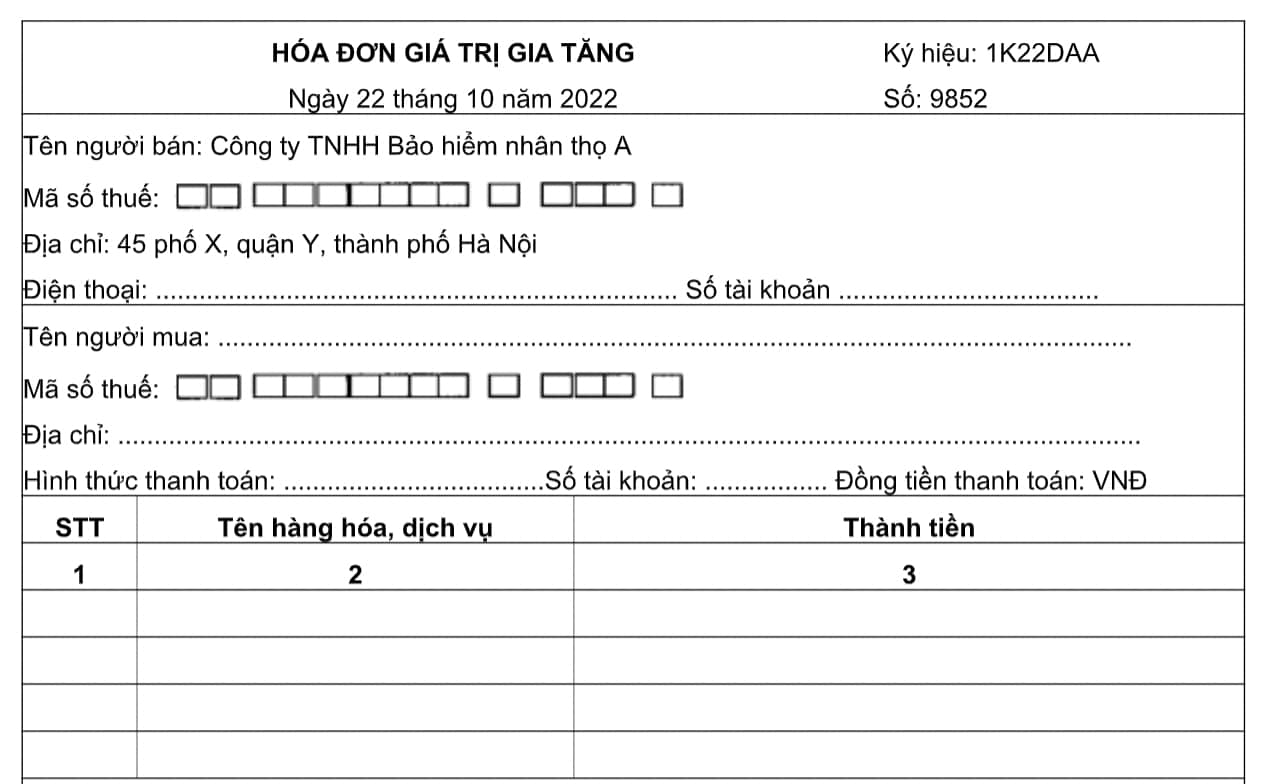

- Value-added e-invoices (used for some specific organizations and enterprises) according to the reference form No. 3 specified in Appendix II issued together with Circular 78/2021 / TT-BTC:

Download the value-added e-invoice reference form here

- Value-added e-invoices (used for some specific organizations and enterprises collected in foreign currency) according to reference form No. 4 specified in Appendix II issued together with Circular 78/2021 / TT-BTC:

Download the value-added e-invoice reference form here

- Value-added invoices issued by the Tax Department according to the reference form No. 6 specified in Appendix II issued together with Circular 78/2021 / TT-BTC:

Download the value-added e-invoice reference form here

How is the 2023 VAT invoice determined in Vietnam?

Pursuant to Clause 1, Clause 2, Article 9 of Decree 123/2020/ND-CP, the time of invoicing for the sale of goods and the provision of services is clearly specified as follows:

When to issue an invoice when selling goods

Invoices for sale of goods (including the sale of state-owned property, property confiscated and put into state fund, and the sale of national reserve goods) shall be issued when the right to own or use goods is transferred to buys, whether the payment of the invoiced amount is made or not.

When to issue an invoice when providing services

Invoices for provision of services shall be issued upon completion of the provision of services, whether the payment of the invoiced amount is made or not. In case a service is provided with payments collected in advanced or during the provision of that service, an invoice shall be issued when each payment is collected (excluding payments of deposited amounts or advance payments which are made to ensure the execution of contracts for provision of accounting, audit, financial consulting or taxation services; valuation services; technical survey and design services; supervision consulting services; investment construction project formulation services).

Note: In case of multiple deliveries or handover of each item or service stage, each delivery or handover must be invoiced for the volume and value of goods and services delivered accordingly.

When to invoice in some specific cases

According to the provisions of Clause 4 Article 9 of Decree 123/2020/ND-CP as follows:

(1) In case of providing services in large quantities, arising frequently, it is necessary to have time to check data between service providers and customers and partners:

Invoicing time is the time to complete the data reconciliation between the parties but no later than 07 days of the month after the month in which the service is provided or no more than 07 days from the end of the convention period.

The conventional period to serve as a basis for calculating the quantity of goods and services provided is based on the agreement between the seller of goods and the provider of services and the buyer.

(2) For telecommunications services:

Invoicing time is the time to complete the reconciliation of data on service charges under economic contracts between service providers but no later than 2 months from the month in which the connection service charge is incurred.

In case of providing telecommunications services (including value-added telecommunications services) through selling prepaid cards, collecting network connection charges when customers register to use the service, but customers do not require VAT invoices or do not provide names and addresses, Tax code:

At the end of each day or periodically in the month, the service provider makes a VAT invoice to record the total revenue generated by each service the buyer does not take the invoice or does not provide the name, address, tax code.

(3) For construction and installation activities:

The time of invoicing is the time of acceptance, handover of works, work items, construction volume, installation completed, regardless of whether money has been collected or not collected.

(4) For organizations doing real estate business, building infrastructure, building houses for sale or transfer, the time of invoicing is specified on a case-by-case basis as follows:

- Have not transferred ownership or use rights: If the collection is carried out according to the project implementation schedule or the collection schedule stated in the contract, the time of invoicing is the date of collection or according to the payment agreement in the contract.

- Transferred ownership, right to use: The time of invoicing the time of transfer of ownership or right to use goods to the buyer, regardless of whether money has been collected or has not been collected.

(5) For business organizations purchasing air transport services exported through websites and e-commerce systems:

The time of invoicing is made according to international practices no later than 05 days from the date of issuance of air transport service documents on the website system and e-commerce system.

(6) For the exploration, exploitation and processing of crude oil:

- The time of invoicing for the sale of crude oil, condensate, products processed from crude oil (including product offtake activities as committed by the Government) is the time when the buyer and seller determine the official selling price, regardless of whether the money has been collected or not collected.

- For the sale of natural gas, companion gas, coal gas is transferred by gas pipeline to the buyer:

The time of invoicing is the time when the buyer and seller determine the monthly delivery volume of gas but no later than 07 days from the date the seller sends the monthly delivery notice.

- In case the guarantee agreement and the Government's commitment have other provisions on the time of invoicing, it shall comply with the provisions of the guarantee agreement and the Government's commitment.

(7) The retail trade and food service business is based on the model of a direct-to-consumer store system, but the accounting of all business activities is carried out at the head office (the head office directly signs contracts for the purchase and sale of goods, services with printed vouchers for customers, voucher data stored on the system and customers do not need to receive electronic invoices:

At the end of the day, the business base on information from the Voucher to synthesize electronic invoicing for transactions of selling goods and providing food and drink during the day.

In case the customer requests e-invoicing, the e-invoicing business shall deliver it to the customer.

(8) For the sale of electricity by power generation companies in the electricity market, the time of e-invoicing shall be determined based on the time of reconciliation of payment data between the operator of the electricity system and the electricity market, the power generation unit and the electricity purchase unit according to the regulations of the Ministry of Industry and Trade or the electricity purchase contract has been The Ministry of Industry and Trade guides and approves.

The latest date of invoicing is the last day of the tax declaration and payment deadline for the month in which tax obligations arise in accordance with tax law.

Particularly for electricity sales of power generation companies with the Government's guarantee commitment on the time of payment, the time of e-invoicing is based on the Government's guarantee, guidance and approval of the Ministry of Industry and Trade and power purchase contracts signed between the buyer and the seller.

(9) The time of e-invoicing for the sale of gasoline at retail outlets to customers is the time of the end of the sale of gasoline by each sale.

Sellers must ensure adequate storage of e-invoices in case of selling gasoline to customers who are non-business individuals or business individuals and ensure that they can look up when requested by competent authorities.

(10) In the case of providing air transport services or insurance services through agents, the time of invoicing is the time to complete the data reconciliation between the parties but not later than the 10th day of the month after the month in which it arose.

(11) In case of providing banking, securities, insurance, money transfer services via e-wallets, decommissioning and power supply services of electricity distribution units to buyers who are non-business individuals (or business individuals) but do not have the need to collect invoices, at the end of the day or at the end of the month, the unit shall issue a total invoice based on information Details of each transaction arising during the day and month at the unit's data management system.

The service provider must be responsible for the accuracy of the content of transaction information and provide a summary table detailing the service provided when requested by the competent authority.

If the customer requests an invoice for each transaction, the service provider must issue an invoice for delivery to the customer.

(12) Business of transporting passengers by taxi using billing software in accordance with the provisions of law, the time of invoicing is as follows:

- At the end of the trip, enterprises and cooperatives doing business of transporting passengers by taxi using payment software send the information of the trip to customers and send it to the tax office in the data format of the tax authority.

The information includes the name of the transport business unit, the vehicle control plate, the distance of the trip (in kilometers) and the total amount paid by the passenger.

- In case the customer takes an e-invoice, the customer updates or sends the complete information (name, address, tax code) to the software or service provider.

Based on the information sent or updated by customers, enterprises and cooperatives doing business of transporting passengers by taxi using billing software send invoices of the trip to customers, and at the same time transfer invoice data to tax authorities.

(13) For medical establishments providing medical examination and treatment services that use medical examination and treatment management software and hospital fee management, each medical examination and treatment transaction and the implementation of photographic, screening and testing services with printed receipts (collecting hospital fees or examination fees, tests) and stored on information technology systems:

- If customers (medical examiners) do not need to collect invoices, at the end of the day, the medical establishment shall base on medical examination and treatment information and information from the receipt to compile electronic invoices for medical services performed during the day.

- If the customer requests e-invoicing, the medical facility shall issue an electronic invoice to the customer.

(14) For the collection of tolls for road use services in electronic form, the date of electronic invoicing is the day the vehicle passes through the toll booth.

In case a customer using the road toll service in the form of electronic toll does not stop having one or more vehicles using the same service several times a month, the service provider may issue an e-invoice periodically, the date of e-invoicing is at least the last day of the month in which the toll service arises.

The content of the invoice lists details each turn of vehicles passing through the toll booths, including the time the vehicle passes through the station, the road use fee price of each turn.

LawNet