Vietnam: How to register to use e-invoices according to the tax calculation method each time it is generated without applying for every time?

- Issue an invoice each time it is incurred and the method of tax calculation each time it is incurred according to Vietnamese regulations?

- How to register to use e-invoices without having to apply for individual issuance each time in Vietnam?

- The current form of registration form for using electronic invoices of Vietnam?

Issue an invoice each time it is incurred and the method of tax calculation each time it is incurred according to Vietnamese regulations?

Pursuant to Clause 5, Article 3 of Circular 40/2021/TT-BTC, which defines "The method of tax declaration according to each time it is incurred" is the method of tax declaration and tax calculation according to the ratio on the actual revenue each time it is incurred.

Pursuant to Article 6 of Circular 40/2021/TT-BTC stipulating the tax calculation method applicable to business individuals who pay tax each time it is incurred.

- The method of tax declaration according to each time it is incurred is applicable to individuals who do business infrequently and do not have a fixed business location. Irregular business is determined depending on the characteristics of production and business activities of each field and industry and is determined by individuals to choose a tax declaration method according to the guidance in this Circular. A fixed business location is a place where an individual conducts production and business activities, such as a transaction location, store, shop, factory, warehouse, wharf, yard, or other similar location.

- Business individuals pay tax on each occasion, including:

+ Individuals doing mobile business;

+ Individuals who are private construction contractors;

+ Individuals transfer the Vietnamese national internet domain name “.vn”;

+ Individuals earning income from digital information content products and services if they do not choose to pay tax according to the declaration method.

- Business individuals that pay tax upon each time they are incurred are not required to comply with the accounting regime but must store invoices, vouchers, contracts, and documents proving lawful goods and services and present the tax return file for each time it is incurred.

- Business individuals that pay tax on each occasion shall declare tax when there is a taxable revenue.

Vietnam: How to register to use e-invoices according to the tax calculation method each time it is generated without applying for every time?

How to register to use e-invoices without having to apply for individual issuance each time in Vietnam?

Business households and individuals that pay flat tax, if they wish to get invoices delivered to customers, shall be issued an electronic invoice with the tax authority's code by the tax authority for each time they arise and must pay tax before the tax authority.

In case business households and individuals want to register for the use of e-invoices with tax authorities' codes, they must choose to pay tax according to the declaration method and comply with the accounting regime prescribed in Circular 88/2021/TT-BTC and register for the use of e-invoices as prescribed in Decree 123/2020/ND-CP (send the declaration of registration to use e-invoices according to Form No. 01/DKTD-HDĐT to the agency). tax through e-invoice service providers).

When the declaring household is approved by the tax authority to use the electronic invoice with the tax authority's code, it may use the electronic invoice with the tax authority's code and must destroy the purchased invoice from the tax authorities.

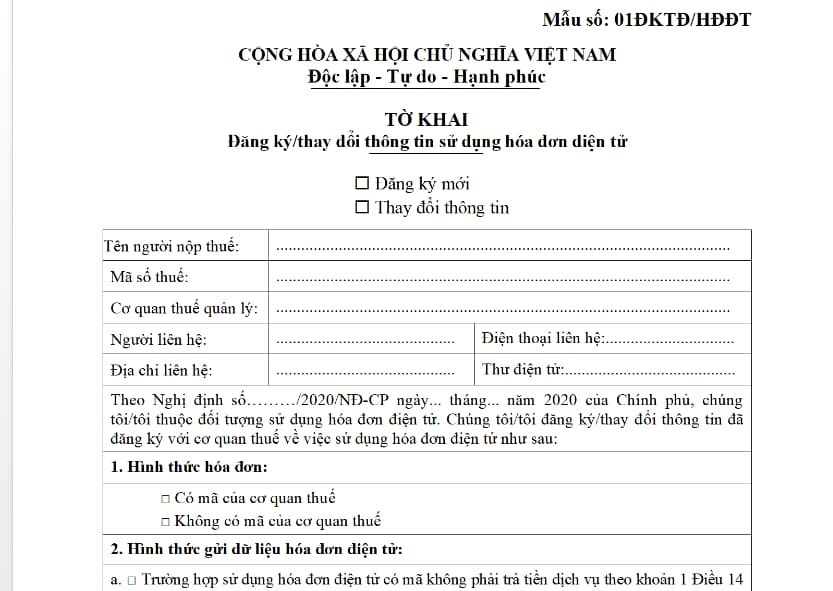

The current form of registration form for using electronic invoices of Vietnam?

Pursuant to Appendix IA issued together with Decree 123/2020/ND-CP stipulating the form of registration declaration for the use of e-invoices, made according to form No. 01/DKTD-HDDT Appendix IA:

Download the registration form for using e-invoices: Click here.

LawNet