Vietnam: How to register for an e-tax transaction account on Canhan.gdt.gov.vn in 2024? What entities are eligible to apply for an e-tax transaction account in Vietnam?

Vietnam: How to register for an e-tax transaction account on Canhan.gdt.gov.vn in 2024?

Below is a guide to register for an individual e-tax transaction account:

Step 1: Access the website at https://canhan.gdt.gov.vn.

Step 2: Taxpayers click on "Register."

Step 3: Taxpayers enter their Tax Identification Number and confirmation code. Select "Individual" and click on "Register."

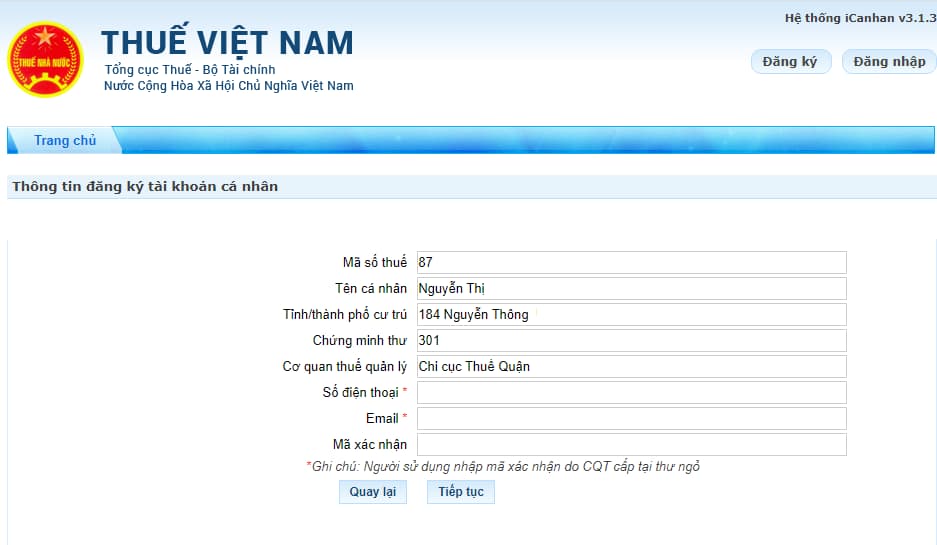

Step 4:

On the screen, the system automatically fills in the following information: Tax Identification Number, Individual Name, Residential Address, ID Card/Passport, Tax Authority, and does not allow editing.

- Taxpayers must fill in the remaining information:

+ Phone number;

+ Email address;

+ Confirmation code: Leave blank if you have not received a confirmation code from the tax authority. If you have received a confirmation code, it is mandatory to enter it.

Then click on "Next."

Step 5: The system displays the "Registration for Electronic Tax Transactions with Tax Authority" form. Taxpayers review the information and click on "Complete Registration."

Step 6:

- If taxpayers have a confirmation code from the tax authority: The system notifies the completion of registration and sends a notification to the registered email address. It also sends the login password to the registered phone number.

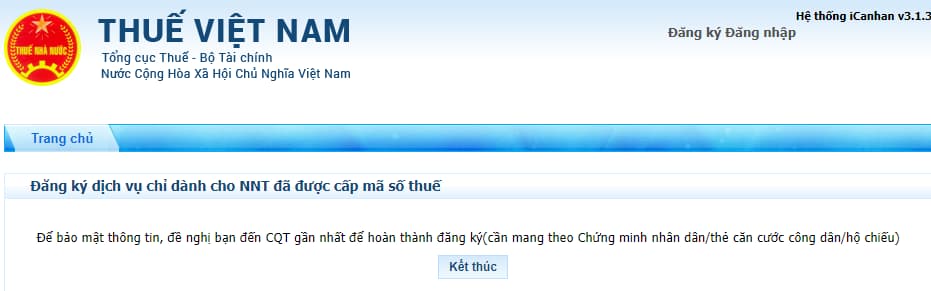

- If taxpayers do not have a confirmation code from the tax authority: The system provides a notification stating, "For information security, please visit the nearest tax authority to complete the registration (bring your ID card/citizen ID card/passport)."

Then select "Finish."

Vietnam: How to register for an e-tax transaction account on Canhan.gdt.gov.vn in 2024? What entities are eligible to apply for an e-tax transaction account in Vietnam? (Image from the Internet)

What entities are eligible to apply for an e-tax transaction account in Vietnam?

Pursuant to the provisions in Point a, Clause 1, Article 10 of Circular 19/2021/TT-BTC:

Registration of e-tax transactions

1. Apply for an e-tax transaction account with a tax authority through the GDT’s web portal

a) The taxpayer that is an authority, organization or individual that has been issued with a digital certificate or an individual that has not had a digital certificate but has had a TIN is entitled to apply for an e-tax transaction account with a tax authority.

...

Thus, the taxpayer that is an authority, organization or individual that has been issued with a digital certificate or an individual that has not had a digital certificate but has had a TIN is entitled to apply for an e-tax transaction account with a tax authority.

How does a taxpayer register to change and supplement e-transaction information in Vietnam?

Pursuant to the provisions of Article 11 of Circular 19/2021/TT-BTC, taxpayers register to change and supplement e-transaction information as follows:

Case 1:

If any taxpayer that has been issued with an e-tax transaction account as prescribed in Article 10 of this Circular wishes to make any change or addition to the information registered for e-tax transactions with the tax authority, such taxpayer shall sufficiently and promptly update such information. The taxpayer shall access the GDT’s web portal to update the change or addition to the information registered for e-tax transactions with the tax authority (Form No. 02/ĐK-TĐT enclosed herewith), e-sign and send it to the GDT’s web portal.

Within 15 minutes from the receipt of information about change or addition, the GDT’s web portal shall send the taxpayer a notification (Form No. 03/TB-TĐT enclosed herewith) of acceptance or non-acceptance of the information about the change or addition.

Case 2: If any taxpayer that has registered transactions with the tax authority by electronic means through the web portal of a competent authority wishes to make any change or addition to the registered information, such taxpayer shall comply with regulations of the competent authority

Case 3: If any taxpayer that has been issued with an e-tax transaction account through a T-VAN service provider as prescribed in Article 42 of Circular 19/2021/TT-BTC wishes to make any change or addition to the information registered for e-tax transactions, such taxpayer shall comply with the regulations set out in Article 43 of Circular 19/2021/TT-BTC.

Case 4: Information about change or addition to the transaction account for e-tax payment at the bank or IPSP shall be registered by the taxpayer with the bank or IPSP where the taxpayer opens their account as prescribed in Clause 5 Article 10 of Circular 19/2021/TT-BTC.

Case 5: Taxpayers shall register change of any e-tax transaction method as prescribed Clause 4 Article 4 of Circular 19/2021/TT-BTC and regulations set out in Article 11 of Circular 19/2021/TT-BTC.

LawNet