Vietnam: How to calculate partial progressive tax on salary, wages and business income in 2022?

- Tax bases for individuals with salaries and wages according to the progressive tax method of Vietnam?

- How to calculate tax for individuals with salaries and wages according to the progressive tax method of Vietnam?

- How to calculate progressive tax by section for salary, wages and business income according to Vietnamese regulations?

Tax bases for individuals with salaries and wages according to the progressive tax method of Vietnam?

Pursuant to Clauses 1 and 2, Article 7 of Circular 111/2013/TT-BTC (amended by Clause 6, Article 25 of Circular 92/2015/TT-BTC) stipulating tax bases for individuals with salary, wages are

- Taxable income is determined by taxable income as guided in Article 8 of this Circular minus (-) the following deductions:

+ The deductions for family circumstances as guided in Clause 1, Article 9 of this Circular.

+ Payments for voluntary insurance and retirement funds as guided in Clause 2, Article 9 of this Circular.

+ Charitable, humanitarian and study promotion contributions as guided in Clause 3, Article 9 of this Circular.

- Tax

Personal income tax rates for incomes from business, salaries and wages are applied according to the partially progressive tax schedule specified in Article 22 of the Law on Personal Income Tax, specifically as follows:

How to calculate tax for individuals with salaries and wages according to the progressive tax method of Vietnam?

Pursuant to Clause 3, Article 7 of Circular 111/2013/TT-BTC (amended by Clause 6, Article 25 of Circular 92/2015/TT-BTC) stipulates the tax calculation method for individuals with salaries and wages according to regulations. The progressive tax calculation method is:

Personal income tax on income from salaries and wages is the total tax calculated by each income level. The tax amount calculated for each income tier is equal to the taxable income of the income tier multiplied (×) by the corresponding tax rate of that income tier.

For the convenience of calculation, the shortened calculation method can be applied according to Appendix No. 01/PL-TNCN issued together with this Circular.

Example 4: Mrs. C has a monthly income of 40 million dong and pays the insurance premiums: 7% social insurance, 1.5% health insurance on salary. Mrs. C takes care of 2 children under 18 years old, in the month Ms. C does not contribute to charity, humanitarian, or study promotion. Ms. C's personal income tax temporarily paid in the month is calculated as follows:

- Mrs. C's taxable income is VND 40 million.

- Mrs. C is entitled to the following deductions:

+ Personal deduction: 9 million VND

+ Family circumstances deduction for 02 dependents (2 children):

3.6 million dong × 2 = 7.2 million dong

+ Social insurance, health insurance:

40 million dong × (7% + 1.5%) = 3.4 million dong

Total deductions:

9 million VND + 7.2 million VND + 3.4 million VND = 19.6 million VND

- Mrs. C's taxable income is:

40 million dong - 19.6 million dong = 20.4 million dong

- Tax payable:

Method 1: The payable tax amount calculated according to each level of the Partial Progressive Tariff:

+ Level 1: taxable income up to VND 5 million, tax rate of 5%:

5 million dong × 5% = 0.25 million dong

+ Level 2: taxable income over VND 5 million to VND 10 million, tax rate of 10%:

(10 million VND - 5 million VND) × 10% = 0.5 million VND

+ Level 3: taxable income over VND 10 million to VND 18 million, tax rate of 15%:

(18 million dong - 10 million dong) × 15% = 1.2 million dong

+ Level 4: taxable income over VND 18 million to VND 32 million, tax rate of 20%:

(20.4 million VND - 18 million VND) × 20% = 0.48 million VND

- The total tax payable by Mrs. C in the month is:

0.25 million VND + 0.5 million VND + 1.2 million VND + 0.48 million VND = 2.43 million VND

Method 2: The payable tax amount is calculated by the abbreviated method:

Taxable income in the month of VND 20.4 million is a taxable income of level 4. The payable personal income tax amount is as follows:

20.4 million dong × 20% - 1.65 million dong = 2.43 million dong

Vietnam: How to calculate partial progressive tax on salary, wages and business income in 2022?

How to calculate progressive tax by section for salary, wages and business income according to Vietnamese regulations?

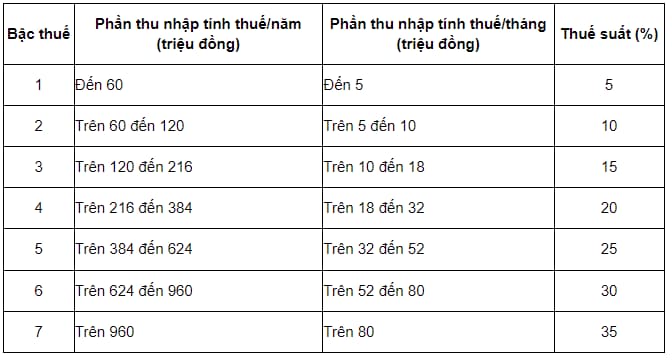

Pursuant to Appendix 01/PL-TNCN issued together with Circular 111/2013/TT-BTC stipulating the partial progressive tax calculation method, which is concretized according to the abbreviated tax schedule as follows:

.jpg)

LawNet