Vietnam: How is the value-added tax declaration form applicable to enterprises declaring tax according to the deduction method prescribed?

- How is the value-added tax declaration form applicable to enterprises declaring tax according to the deduction method prescribed in Vietnam?

- How to declare value-added tax declaration according to form 01 of Circular 80 of Vietnam?

- What does the value-added tax return for production and business activities under the deduction method include in Vietnam?

How is the value-added tax declaration form applicable to enterprises declaring tax according to the deduction method prescribed in Vietnam?

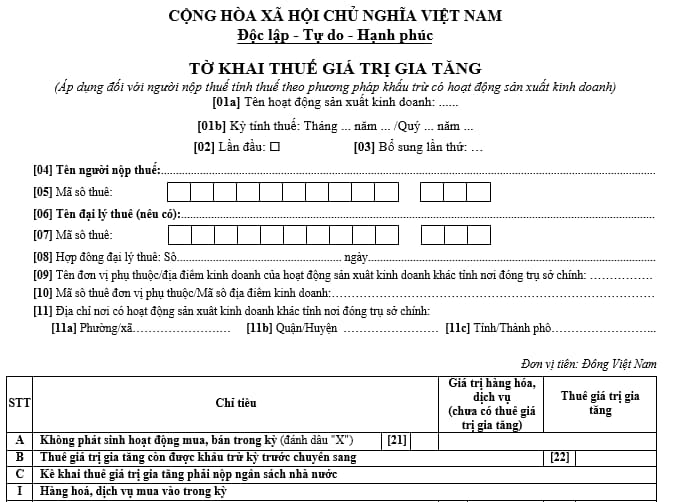

Currently, the value-added tax declaration form (applicable to taxpayers calculating tax according to the deduction method with production and business activities) is specified in Form 01/VAT issued together with Circular 80/2021 / TT-BTC as follows:

Download the Value Added Tax Return Form (applicable to taxpayers who calculate tax according to the deduction method with production and business activities): here.

Vietnam: How is the value-added tax declaration form applicable to enterprises declaring tax according to the deduction method prescribed?

How to declare value-added tax declaration according to form 01 of Circular 80 of Vietnam?

Pursuant to Form 01/VAT issued together with Circular 80/2021/TT-BTC, the value-added tax declaration (applicable to taxpayers calculating tax according to the deduction method with production and business activities) is guided to prepare as follows:

- Target [01a]: The taxpayer chooses one of the following activities:

+ Normal production and business activities

+ Lottery activities, computer lottery

+ Oil and gas exploration and exploitation activities

+ Investment projects on infrastructure, houses for transfer other than in the province where the head office is located

+ Power generation plants in other provinces where the head office is located.

- Targets [09], [10], [11]: Declare information of dependent units, business locations located in localities other than the provinces where the head office is located, for the cases specified at Points b and c, Clause 1, Article 11 of the Government's Decree No. 126/2020/ND-CP dated October 19, 2020.

In case there are many dependent units, business locations located in many districts managed by the Tax Department, select 1 representative unit to declare in this indicator. In case there are many dependent units and business locations located in many districts managed by the Regional Tax Department, select 1 unit representing the district managed by the Regional Tax Department to declare in this indicator.

- Target [32a]: Declare the value of goods and services in cases where the value-added tax is not declared and charged in accordance with the law on value-added tax.

- Target [37] and [38]: Declare according to the amount of tax deducted adjusted up/down at target II on the Supplementary Declaration. Particularly, in case the tax authority or competent agency has issued a conclusion or decision on tax treatment with corresponding adjustments to the previous tax periods, the tax declaration in the tax return of the tax period receives the conclusion and decision on tax processing (not having to declare additional tax returns).

- Target [39a]: Declare the amount of VAT that is still deducted without the request for refund of the investment project transferred to the taxpayer to continue withholding (is the amount of VAT that is still deducted, not eligible for refund, non-refundable that the taxpayer has separately declared the tax return of the investment project) when the investment project comes into operation or the VAT amount is still deducted unless otherwise requested to complete the production and business activities of the dependent entity upon the termination of operation,...

- Target [40b]: Declare the total amount of tax declared in indicators [28a] and [28b] of Declaration Form No. 02/VAT.

What does the value-added tax return for production and business activities under the deduction method include in Vietnam?

Pursuant to Subsection 2.1 Section 2 of Appendix I promulgated together with Decree 126/2020/ND-CP, there are regulations on value-added tax returns for production and business activities under the deduction method including:

- Value added tax return (applicable to taxpayers who calculate tax according to the method - deduction with production and business activities)

- Appendix of the allocation table of value-added tax payable to localities where revenues are enjoyed for hydropower production

- Appendix to the allocation table of value-added tax payable to localities where revenues are enjoyed for computer lottery business

- Appendix of value-added tax allocation table payable to the locality where the revenue source is entitled (except hydropower production, computer lottery business)

- Temporary value-added tax declaration on revenue (applicable to taxpayers who calculate tax by deduction method with real estate construction and transfer activities in a provincial-level area other than the one where the head office is located but do not establish a dependent unit, business location)

LawNet