Vietnam: Form of minutes of liquidation of fixed assets for small and medium enterprises in 2022 (Form 02-TSCD)? How is the fixed asset tracking process carried out?

Form of fixed asset liquidation minutes for small and medium enterprises in 2022 of Vietnam?

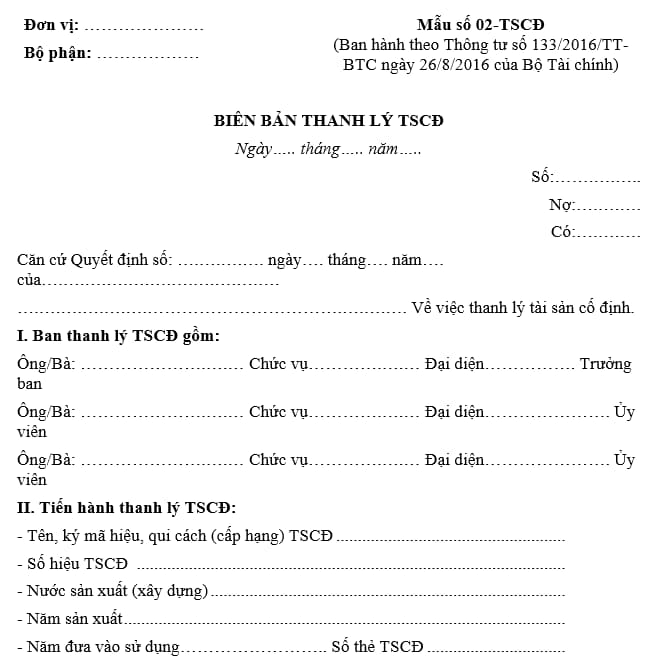

Pursuant to Appendix 3 issued together with Circular 133/2016 / TT-BTC stipulating the form of minutes of liquidation of fixed assets for small and medium enterprises according to form No. 02-TSCD as follows:

Download the full form of fixed asset liquidation minutes for small and medium enterprises: Here.

Vietnam: Form of minutes of liquidation of fixed assets for small and medium enterprises in 2022 (Form 02-TSCD)? How is the fixed asset tracking process carried out?

How to recognize fixed assets according to Vietnamese regulations?

Pursuant to Article 3 of Circular 45/2013/ TT-BTC stipulating standards and ways of identifying fixed assets as follows:

- Means of labor are the tangible assets with independent structure, or a system of many individual parts of assets linked to perform one or a certain number of functions and without any part, the system can not work, and if meet the following three criteria they shall be regarded as fixed assets:

a) It is certain to gain economic benefit in the future from the use of such asset;

b) Having the utilization time of over 01 year.

c) Primary price of assets must be determined reliably, and is valued at 30,000,000 (thirty million) dong or more.

In case a system includes many individual components of assets linked together, in which each component has different utilization time and without any component the entire system still perform its main operating function its main activity but due to requirements on management and use of fixed asset requiring separately managed asset division, each asset division if simultaneously satisfying three criteria of fixed assets shall be regarded as independent tangible fixed assets.

For animals working and / or giving products, then each of the animals simultaneously satisfying three criteria of fixed assets is regarded as tangible fixed.

For perennial orchards, each piece of garden, or trees simultaneously satisfying three criteria shall be regarded as a fixed tangible asset.

- Standards and identification of intangible assets:

All actual costs spent by enterprises simultaneously satisfyiing all three criteria specified in Clause 1 of this Article, without forming tangible fixed assets are regarded as intangible assets.

The expenses not simultaneously satisfying all three criteria specified in Clause 1, Article 3 of this Circular shall be recorded directly or gradually amortized into the business cost of enterprises.

As for costs incurred in the implementation phase recognized as intangible assets generated from the inside of enterprise if they simultaneously satisfy the following seven conditions:

a) Technical feasibility ensures the completion and put the intangible assets to the expected use or sale;

b) Enterprises intend to complete the intangible asset for use or sale;

c) Enterprises have the ability to use or sell these intangible assets;

d) These Intangible assets have to generate economic benefits in the future;

e) Having sufficient technical and financial resources and other resources to complete stages of deployment, sale or use of those intangible assets.

g) Being able to identify with certainty the full cost of the deployment phase to create such intangible assets;

h) It is estimated to have adequate standards on utilization time and value defined for intangible fixed assets.

- The cost of establishment of enterprise, cost of staff training, advertising cost incurred prior to the establishment of enterprise, cost of research stage, relocation, sale for possession and use of technical materials, patents, license of technology transfer, trade marks, business advantage that are not intangibles fixed assets but are amortized into business cost of enterprises in a maximum time not exceeding 3 years according regulations of Law on Enterprise Income Tax of Vietnam.

- For Joint-Stock companies converted from state-owned companies under the provisions of the Government’s Decrees issued before Decree No. 59/2011/ND-CP dated July 18, 2011 of the Government on the conversion of enterprises with 100% state capital into joint-stock companies, having business advantage included in the enterprise value when determining enterprise value for equitization by the method of assets and approved by the competent authority as prescribed, they shall perform the allocation of value of business advantage under provisions in Circular No. 138/2012/TT-BTC dated August 20, 2012 of the Ministry of Finance guiding the allocation of value of business advantage for Joint-Stock companies converted from state-owned companies.

How does the fixed asset tracking process work in Vietnam?

Pursuant to Point 1.8 Clause 1 Article 31 of Circular 133/2016 / TT-BTC stipulating the process of tracking fixed assets of small and medium enterprises as follows:

Tangible fixed assets must be specific in terms of category and location. To be specific:

- Tangible fixed assets include: houses, structures, machinery, equipment, transmission devices, management instruments, perennial plants, working animals, producing animals and other tangible fixed assets.

- Intangible fixed assets include: distribution rights, copyrights, patent, trademarks, software programs, licenses and franchises; other intangible fixed assets.

LawNet