Vietnam: Form of corporate income tax finalization declaration according to Circular 80? How to record Form 03/CIT according to Circular 80/2021/TT-BTC?

What is the latest corporate income tax finalization form recently in Vietnam?

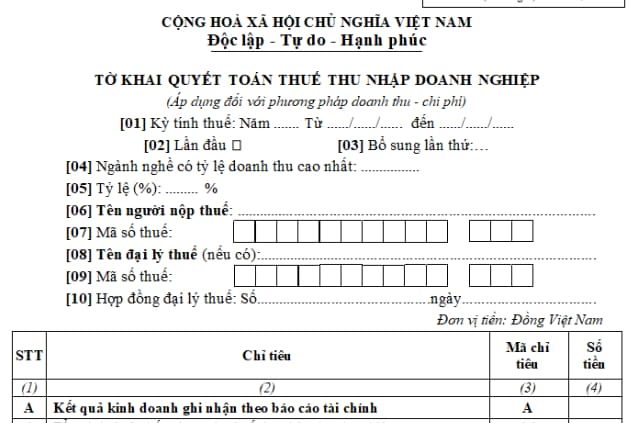

Pursuant to the Corporate Income Tax Finalization Form applied to the current revenue-expense method specified in Form 03/CIT in Section VI of Appendix II issued together with Circular 80/2021/TT-BTC, as follows:

Download the Corporate Income Tax Finalization Form applicable to the revenue-expense method: here

Vietnam: Form of corporate income tax finalization declaration according to Circular 80? How to record Form 03/CIT according to Circular 80/2021/TT-BTC?

How to record Form 03/CIT when finalizing corporate income tax in Vietnam?

Based on the corporate income tax finalization declaration form applicable to the above-mentioned revenue method, the acronyms and symbols guiding the implementation are as follows:

- CIT: Corporate income; Real estate: Real estate;

- Target G1, G3: Taxpayers declare the amount of CIT overpaid in the previous period to be offset with the amount of CIT payable this period.

- Target D11, G2, G4, G5: Taxpayers declare the amount of CIT temporarily paid to the state budget up to the deadline for submitting the finalization declaration. For example, if a taxpayer has a tax period from 01/01/2021 to 31/12/2021, the amount of CIT temporarily paid during the year is the amount of CIT paid for the tax period in 2021 from 01/01/2021 to 31/3/2022.

- In case the taxpayer is a lottery enterprise with production and business activities other than the lottery business, the taxpayer shall declare the amount of CIT payable of the lottery business in the E1 target, the amount of CIT payable by other production and business activities in the E2 target, E3.

- Criteria E, G: NNT does not declare the amount of CIT payable or temporarily paid of activities entitled to incentives other than the province has declared separately.

- Target E4, G5, H3: Taxpayers declare the amount of CIT payable, temporarily paid of infrastructure transfer activities, houses handed over this period and collect advance money from customers according to schedule (including the amount collected in previous and this period).

How is corporate income tax finalization for dependent units and business locations being production facilities carried out in Vietnam?

Pursuant to section c.2 Point c Clause 3 Article 17 of Circular 80/2021 / TT-BTC stipulating the finalization of corporate income tax for dependent units, business locations are production establishments

Accordingly, these grassroots units shall finalize corporate income tax according to the following provisions:

- Taxpayers declare corporate income tax finalization for all production and business activities according to form No. 03/CIT.

And submit an appendix to the allocation table of corporate income tax payable to localities where revenues are enjoyed for production facilities according to form No. 03-8/CIT to the directly managing tax authority;

At the same time, pay the amount of tax allocated to each province where the production facility is located as prescribed in Clause 4 Article 12 of Circular 80/2021 / TT-BTC

- Particularly for activities entitled to corporate income tax incentives, taxpayers shall declare tax finalization according to form No. 03/CIT issued together with Appendix II of this Circular at the directly managing tax authority, determine the amount of corporate income tax payable of activities entitled to corporate income tax incentives according to form No. 03-3A/CIT, 03-3B/CIT, 03-3C/CIT, 03-3D/CIT and pay at the tax office where there is a unit entitled to incentives other provinces and tax authorities directly managing it.

- In case the amount of tax temporarily paid quarterly is less than the amount of tax payable allocated to each province according to tax finalization, the taxpayer must pay the missing tax amount for each province.

- In case the amount of tax temporarily paid quarterly is greater than the amount of tax allocated to each province, it shall be determined as the amount of tax overpaid and handled according to the provisions of Article 60 of the Vietnam Law on Tax Administration 2019 and Article 25 of Circular 80/2021 / TT-BTC.

LawNet