Sample reporting on the use of invoices for business households applied from July 1, 2022 in Vietnam? Is there a penalty for late submission of the invoice usage report?

In which cases must report the use of invoices to business households in Vietnam?

According to Article 29 of Decree 123/2020/ND-CP stipulating invoices, vouchers stipulate reports on the use of invoices for business households:

“Article 29. Reporting on use of printed invoices purchased from tax authorities and list of invoices used during a period

1. Every quarter, enterprises, business entities, household or individual businesses that bought invoices from tax authorities shall submit reports on their use of invoices and lists of invoices used during the period to their supervisory tax authorities.

Reports on use of invoices shall be submitted quarterly by the last day of the first month of the quarter following the reporting quarter, using Form No. BC26/HDG in Appendix IA enclosed herewith.

If no invoices are used during the period, the quantity of used invoices in the report shall be zero (0), and the list of used invoices is not required. If the quantity of unused invoices specified in the report on use of invoices in the previous period is zero (0) and no invoices are purchased and used during this period, submission of report on use of invoices is not required.

2. When an enterprise, business entity, household or individual business is fully or partially divided, merged, dissolved or declared bankrupt or has its ownership transferred, or when a state-owned enterprise is delegated, sold or leased, the report on its use of invoices and list of invoices used during the period shall be submitted by the same deadline with that of the tax statement dossier.

3. If an enterprise, business entity, household or individual business relocates to another province which is not under the management of its current supervisory tax authority, the report on use of invoices and list of invoices used during the period shall be submitted to the tax authority in charge of the province from which it relocates.”

Sample reporting on the use of invoices for business households applied from July 1, 2022 in Vietnam? Is there a penalty for late submission of the invoice usage report?

Sample reporting on the use of invoices for business households applied from July 1, 2022 in Vietnam?

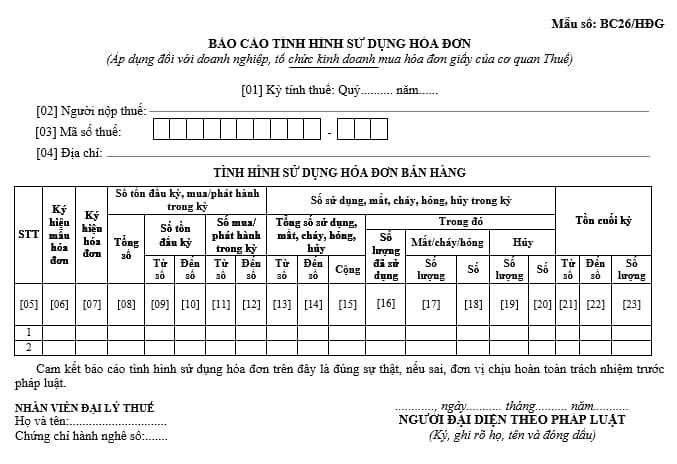

According to Appendix IA Dossier of invoices and documents - taxpayers promulgated together with Decree 123/2020/ND-CP stipulating invoices and documents, regulations on the report form for using invoices are:

Download the invoice usage report form: Here.

Is there a penalty for late submission of the invoice usage report in VIetnam?

According to the provisions of Article 29 of Decree 125/2020/ND-CP stipulating the sanctioning of administrative violations on taxes and invoices:

“Article 29. Penalties for violations against regulations on the act of preparing and delivering invoices

1. Cautions shall be imposed for the act of submitting notices or reports regarding invoices from 1 to 5 days after expiry of the regulated submission time limit under mitigating circumstances.

2. Fines ranging from VND 1,000,000 to VND 3,000,000 shall be imposed for one of the following violations:

a) Submitting notices or reports regarding invoices from 1 to 10 days after expiry of the regulated submission time limit, except the case prescribed in clause 1 of this Article;

b) Issuing invoices wrongly or those whose contents are not fully consistent with those stated in lawful notices and reports regarding invoices submitted to tax authorities.

If entities or persons, by themselves, detect errors and re-issue substitute notices or reports in accordance with regulations to their supervisory tax authorities before issuance of decisions to carry out tax inspections or reviews at the violating taxpayer’s offices by tax authorities or competent authorities, they shall not be sanctioned.

3. Fines ranging from VND 2,000,000 to VND 4,000,000 shall be imposed for the act of submitting notices or reports regarding invoices to tax authorities from 11 to 20 days after expiry of the regulated submission time limit.

4. Fines ranging from VND 4,000,000 to VND 8,000,000 shall be imposed for the act of submitting notices or reports regarding invoices to tax authorities from 21 to 90 days after expiry of the regulated submission time limit.

5. Fines ranging from VND 5,000,000 to VND 15,000,000 shall be imposed for one of the following violations:

a) Submitting notices or reports regarding invoices to tax authorities at least 91 days after expiry of the regulated submission time limit;

b) Failing to submit notices and reports regarding invoices to tax authorities as legally required.

6. If any act of violation arising from the preparation and delivery of invoice-related notices or reports is regulated in Article 23 and 25 herein, regulations of this Article shall not be applied for the imposition of administrative penalties.

7. Remedies: Compelling the preparation and delivery of invoice-related notices or reports with respect to the acts specified in point b of clause 2 and point b of clause 5 of this Article.”

The above is a sample report on the use of invoices applied from July 1, 2022.

LawNet