Latest business income statement template? Instructions for preparing and presenting business performance reports inVietnam?

What are the contents of the Business Performance Report Template?

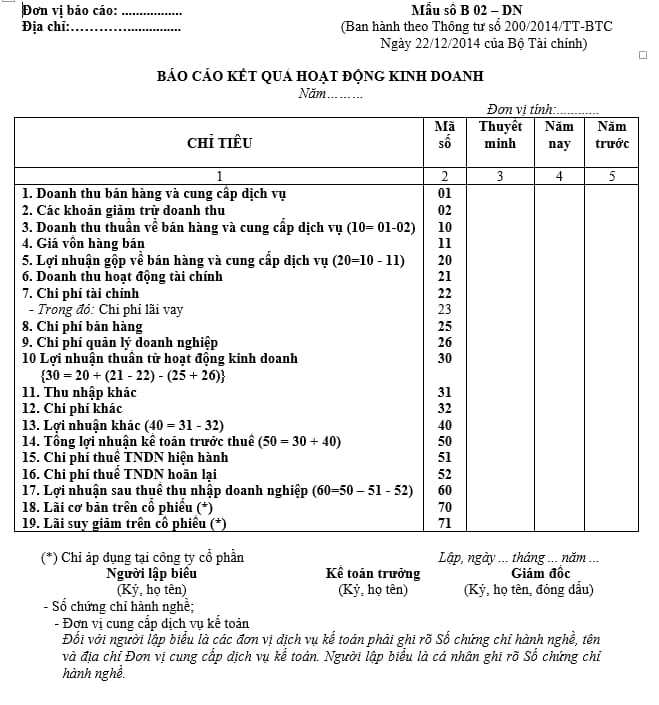

Pursuant to Form No. B 02 - DN Appendix issued together with Circular 200/2014/TT-BTC stipulating the report on business results, including the following specific contents:

Như vậy, báo cáo kết quả hoạt động kinh doanh gồm những nội dung được quy định như trên.

Tải mẫu Báo cáo kết quả hoạt động kinh doanh: Tại Đây

Mẫu Báo cáo kết qả hoạt động kinh doanh mới nhất? Hướng dẫn lập và trình bày báo cáo kết quả hoạt động kinh doanh? (Hình từ internet)

Lập Báo cáo kết quả hoạt động kinh doanh như thế nào?

Căn cứ khoản 1, khoản 2 Điều 113 Thông tư 200/2014/TT-BTC quy định về lập báo cáo kết quả hoạt động kinh doanh như sau:

Về nội dung và kết cấu báo cáo:

- Báo cáo kết quả hoạt động kinh doanh phản ánh tình hình và kết quả hoạt động kinh doanh của doanh nghiệp, bao gồm kết quả từ hoạt động kinh doanh chính và kết quả từ các hoạt động tài chính và hoạt động khác của doanh nghiệp.

- Báo cáo kết quả hoạt động kinh doanh gồm có 5 cột:

+ Cột số 1: Các chỉ tiêu báo cáo;

+ Cột số 2: Mã số của các chỉ tiêu tương ứng;

+ Cột số 3: Số hiệu tương ứng với các chỉ tiêu của báo cáo này được thể hiện chỉ tiêu trên Bản thuyết minh Báo cáo tài chính;

+ Cột số 4: Tổng số phát sinh trong kỳ báo cáo năm;

+ Cột số 5: Số liệu của năm trước (để so sánh).

(2) Về cơ sở lập báo cáo

- Căn cứ Báo cáo kết quả hoạt động kinh doanh của năm trước.

- Căn cứ vào sổ kế toán tổng hợp và sổ kế toán chi tiết trong kỳ dùng cho các tài khoản từ loại 5 đến loại 9.

How to present the income statement?

Pursuant to Clause 3, Article 113 of Circular 200/2014/TT-BTC providing guidance on the preparation and presentation of the report on business results as follows:

"Article 113. Guidelines for preparation and presentation of reports on business results (Form B02-DN)

...

3. Content and method of setting targets in the Statement of Business Performance

3.1. Revenue from selling goods and providing services (Entry 01):

- This entry reflects the total revenue from the sale of goods, finished products, investment real estate, service provision and other revenue in the reporting year of the enterprise. The data to be recorded in this entry is the accumulated amount arising on the Credit side of Account 511 “Revenue from sale of goods and provision of services” in the reporting period.

When the superior unit prepares a consolidated report with the subordinate units without legal status, revenue from sales and provision of services arising from internal transactions must be eliminated.

- This entry does not include indirect taxes, such as VAT (including VAT paid by the direct method), special consumption tax, export tax, environmental protection tax and other taxes and fees. other indirection.

3.2. Revenue deductions (Entry 02):

This entry reflects the sum of amounts deducted from total revenue in the year, including: Trade discounts, sales discounts, sales returns in the reporting period. The data to be recorded in this entry is the accrual amount arising from the debit side of Account 511 “Revenue from goods sale and provision of services” to the credit side of Account 521 “Revenue deductions” in the reporting period.

This entry does not include indirect taxes and fees that enterprises are not entitled to have to pay to the state budget (recorded as a decrease in revenue in the accounting book of Account 511) because these amounts are essentially revenues on behalf of the Government. water, is not included in the revenue structure and is not considered a revenue deduction.

3.3. Net revenue from selling goods and providing services (Entry 10):

This entry reflects the revenue from the sale of goods, finished products, investment properties, service provision and other revenue minus deductions (trade discounts, sales discounts, returned goods sold). re) in the reporting period, as the basis for calculating the business results of the enterprise. Code 10 = Code 01 - Code 02.

3.4. Cost of goods sold (Entry 11):

This entry reflects the total cost of goods, investment property, production costs of finished products sold, direct costs of the volume of completed services provided, and other costs included in the cost of goods or services. write down cost of goods sold in the reporting period. The data to be recorded in this entry is the accumulated amount arising on the Credit side of Account 632 “Cost of goods sold” in the counterpart reporting period on the Debit side of Account 911 “Determination of business results”.

When the superior unit prepares a consolidated report with the subordinate units without legal status, the costs of goods sold arising from internal transactions must be eliminated.

3.5. Gross profit from sales and service provision (Entry 20):

This entry reflects the difference between the net revenue from the sale of goods, finished products, investment properties and provision of services and the cost of goods sold arising in the reporting period. Code 20 = Code 10 - Code 11.

3.6. Revenue from financial activities (Entry 21):

This entry reflects the net financial income arising in the reporting period of the enterprise. The data to be recorded in this entry is the accumulated amount arising on the Debit side of Account 515 “Revenue from financial activities” for the credit side of Account 911 “Determination of business results” in the reporting period.

When a superior entity prepares a consolidated report with an unincorporated subordinate unit, financial income arising from internal transactions must be eliminated.

3.7. Financial expenses (Entry 22):

This entry reflects the total financial expenses, including interest payable, royalties, joint venture operating expenses, etc., incurred in the reporting period of the enterprise. The data to be recorded in this entry is the accumulated amount incurred by the Credit account 635 “Financial expenses” corresponding to the debit side of Account 911 “Determination of business results” in the reporting period.

When the superior unit prepares a consolidated report with the subordinate units without legal status, financial expenses arising from internal transactions must be eliminated.

3.8. Interest expense (Entry 23):

This entry reflects the payable interest expense which is included in financial expenses in the reporting period. The data for this entry is based on the detailed accounting book of Account 635.

3.9. Selling expenses (Entry 25):

This entry reflects the total cost of selling goods, finished products sold and services provided incurred in the reporting period. The data to be recorded in this entry is the total amount incurred on the Credit side of Account 641 “Sales expenses”, corresponding to the Debit side of Account 911 “Determination of business results” in the reporting period.

3.10. Business administration expenses (Entry 26):

This entry reflects the total administrative expenses incurred in the reporting period. The data to be recorded in this entry is the total amount incurred on the Credit side of Account 642 “Business administration expenses”, corresponding to the Debit side of Account 911 “Determination of business results” in the reporting period.

..."

Xem chi tiết nội dung và phương pháp lập các chỉ tiêu trong Báo cáo Kết quả hoạt động kinh doanh: Tại đây

LawNet