Instructions on how to process application for Vietnam extension of payment of value added tax under the tax authority's TMS system?

How is the request to extend the Vietnam extension of payment of value added tax on the TMS system handled?

According to the instructions at point a, subsection 4.1, Section 4, Official Letter 2194/TCT-KK in 2022, processing the request for extension of value-added taxpayers on the TMS system as follows:

For the proposal to extend the Vietnam extension of payment of value added tax

- The TMS system automatically updates the extended tax Vietnam extension of payment deadline for the payable value-added tax amount of the tax period March, April, May, June, July, August, 2022. and the tax period of the first quarter, the second quarter of 2022 according to the Forms 01/GTGT, 03/GTGT, 04/GTGT, 05/GTGT (including the official declaration and the additional declaration during the extended period).

- For the extended value-added tax amount according to the Appendix form 01-2/GTGT, form 01-3/GTGT, form 01-6/GTGT, the tax authority shall manage the allocated value-added tax. perform a lookup at the List of taxpayers requesting an extension on the TMS system to control and update the extended tax Vietnam extension of payment deadline.

Thus, the request to extend the Vietnam extension of payment of value added tax on the TMS system is handled as above.

Instructions on how to process application for Vietnam extension of payment of value added tax under the tax authority's TMS system? (Image from the internet)

How to extend the tax payment deadline for value added tax?

Pursuant to the provisions of Clause 1, Article 4 of Decree 34/2022/ND-CP, as follows:

"Article 4. Extension of time limit for paying tax and land rent

1. For value-added tax (except value-added tax at the import stage)

a) Extension of time limit for tax payment for the amount of value added tax payable (including the tax amount allocated to other provinces at the provincial level where the taxpayer is headquartered, the tax amount to be paid each time). incurred) of the tax period from March to August 2022 (for the case of monthly VAT declaration) and the first quarter and second quarter of 2022 (for the case of VAT declaration). quarterly value added) of enterprises and organizations mentioned in Article 3 of this Decree. The extension period is 06 months for the value-added tax amount from March to May 2022 and the first quarter of 2022, the extension period is 05 months for the value-added tax amount of June 2022 and the second quarter of 2022, the extension period is 04 months for the value-added tax amount of July 2022, the extension time is 03 months for the value-added tax amount of August 2022. the deadline at this point is counted from the end of the time limit for payment of value added tax in accordance with the law on tax administration.

In case the taxpayer makes additional declarations to the tax declaration dossier of the extended tax period, leading to an increase in the payable value-added tax amount and sending it to the tax authority before the extended tax payment time limit expires, the tax amount extended, including the additional tax payable due to the additional declaration.

Enterprises and organizations eligible for the extension shall declare and submit monthly and quarterly value-added tax declarations in accordance with current law, but have not yet paid the payable value-added tax amount. born on the declared value-added tax return. The time limit for payment of value added tax of the month and quarter is extended as follows:

- The deadline for paying value added tax of the tax period of March 2022 is October 20, 2022 at the latest.

- The deadline for paying value-added tax of the April 2022 tax period is November 20, 2022.

- The deadline for paying value added tax of the tax period in May 2022 is December 20, 2022 at the latest.

- The deadline for paying value added tax of the June 2022 tax period is December 20, 2022 at the latest.

- The deadline for paying value added tax of the tax period of July 2022 is December 20, 2022 at the latest.

- The deadline for paying value added tax of the tax period of August 2022 is December 20, 2022 at the latest.

- The deadline for paying value added tax of the tax period of the first quarter of 2022 is October 30, 2022 at the latest.

- The deadline for paying value added tax of the tax period of the second quarter of 2022 is December 31, 2022 at the latest.

b) In case an enterprise or organization mentioned in Article 3 of this Decree has branches or affiliated units, they shall declare value-added tax separately with the tax authority directly managing the branch or affiliated unit. branches and affiliated units are also subject to the extension of payment of value added tax. If a branch or affiliated unit of an enterprise or organization mentioned in Clauses 1, 2 and 3, Article 3 of this Decree does not have production and business activities in the economic sector or field, the extension shall be subject to the extension. branches, affiliated units are not subject to the Vietnam extension of payment of value added tax.

..."

Thus, value added tax (except value added tax at the import stage) is regulated as above.

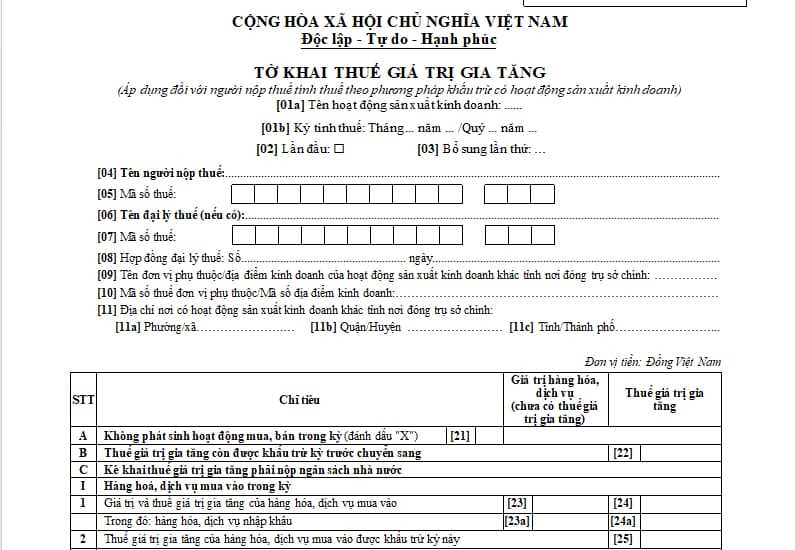

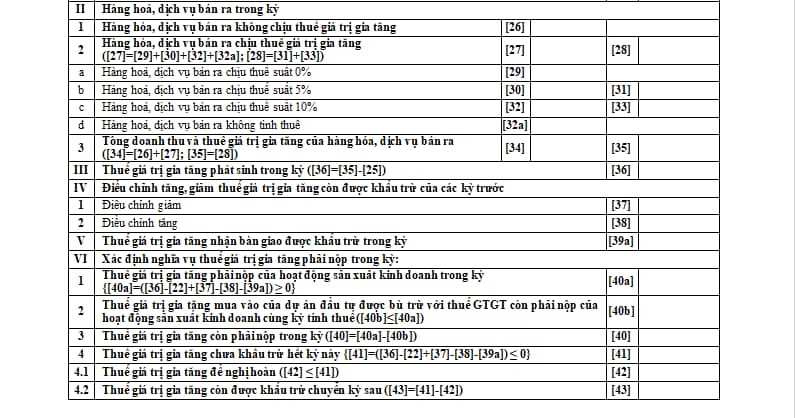

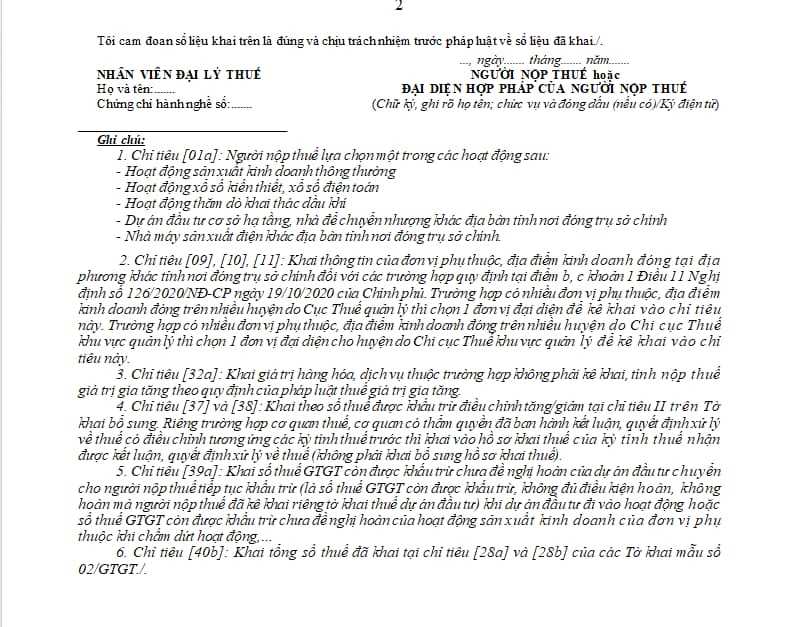

What are the contents of a value-added tax declaration form?

Pursuant to the provisions in Form No. 01/GTGT Appendix II issued together with Circular 80/2021/TT-BTC stipulating the form of value added tax declaration form as follows:

Thus, the value-added tax declaration form is prescribed according to the form above.

Download the value added tax return form: Here

LawNet