Instructions for individuals to self-finalize personal income tax online in Vietnam in 2023? When is the deadline for individuals to self-finalize personal income tax in Vietnam in 2023?

How do individuals make their own personal income tax finalization online?

Step 1: Visit the website of the General Department of Taxation at https://canhan.gdt.gov.vn/

If the taxpayer is not registered, click the Register button and then fill in the tax code and check code information.

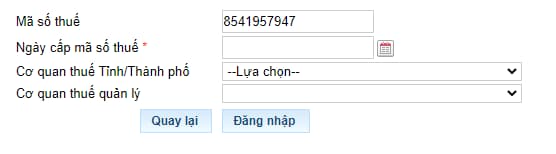

Step 2: Login to the system:

Select "Login" and fill in the appropriate fields in table (2) including "Tax code and "Check code". Then click "continue"

Continue to enter all personal information in the respective fields, including:

- Tax code

- Date of issuance of tax code

- Provincial/City tax office

- Tax management authority

After completing the information, click on the "login" box to continue.

Step 3: Declare tax finalization information

After logging in, select “Tax finalization” -> Select “Online tax declaration”:

Then completely fill in the required information fields.

Note (*) is a required field to fill in.

- Sender's name*: The system automatically fills in the registration information.

- Contact address*: The system automatically fills in the registration information.

- Contact phone*: Automatically follow tax registration information.

- Email address*: Automatically follow tax registration information.

- Choose the declaration: You choose the declaration that is suitable for your case.

- Tax Department: The system automatically fills in registration information.

- Tax Department: The system automatically fills in registration information.

- Type of declaration: Depending on the case, you can choose an official declaration or an additional declaration.

- Year of declaration: The system automatically fills in registration information (can be edited).

In the section select declarations, in case you make your own PIT finalization, you will choose declaration 02/QTT-TNCN - Declaration of PIT finalization. Then, depending on the taxpayer's case, the appropriate selection.

- Type of declaration: You choose "Official declaration"

- After completing the above information, click "Continue".

Step 4: Fill in the online declaration

The declarant declares personal information on the tax return according to the available form

Once completed, select “Complete declaration”.

Step 5: Export XML

To download the completed form declaration file -> select "XML export"

Step 6: Select “Submit declaration”

Select “Submit declaration” then enter “Check code” to verify the submission of declaration and click “Continue”.

After completing the system, there will be a notification of successful submission of the declaration.

Step 7: Print the declaration.

At the step of selecting "Dump XML", the system will send the declaration file in XML format. The payer must make "Print the declaration" to submit to the tax office to make a deduction file.

Open the file "XML Dump" then choose to print 02 copies, then sign the taxpayer's name.

Step 8: Submit tax withholding documents and tax return at the Tax Office that submitted the online declaration to complete.

Instructions for individuals to self-finalize personal income tax online in Vietnam in 2023? When is the deadline for individuals to self-finalize personal income tax in Vietnam in 2023?

What is the deadline for individuals to self-finalize personal income tax in Vietnam in 2023?

Pursuant to Clause 2, Article 44 of the 2019 Law on Tax Administration of Vietnam stipulating as follows:

Deadlines for submission of tax declaration dossiers

...

2. For taxes declared annually:

a) For annual tax statement dossiers: the last day of the 3rd month from the end of the calendar year or fiscal year. For annual tax declaration dossiers: the last day of the first month from the end of the calendar year or fiscal year

b) For annual personal income tax statements prepared by income earners: the last day of the 4th month from the end of the calendar year;

c) For presumptive tax declarations prepared by household businesses and individual businesses: the 15th of December of the preceding year. For new household businesses and individual businesses: within 10 days from the date of commencement of the business.

Thus, the deadline for personal income tax settlement in 2023 for individuals who self-finalize tax is April 30, 2023. However, in 2023, the series of holidays of the Hung Kings' Commemoration Day, April 30 and May 1 will take place in three consecutive days from April 29 to May 1, 2023, of which April 29 and May 30 fall on Saturday and Sunday.

Therefore, the personal income tax statement deadline will be moved to the first working day after the holiday period.

How much penalty will an individual who makes a self-settlement tax return submit a personal income tax settlement return late?

Pursuant to Article 13 of Decree 125/2020/ND-CP of Vietnam stipulating as follows:

Penalties for violations against regulations on time limits for submission of tax returns

1. Penalties imposed in form of cautions shall be imposed for violations arising from filing tax returns from 01 to 05 days after expiration of the prescribed time limits under mitigating circumstances.

2. Fines ranging from VND 2,000,000 to VND 5,000,000 shall be imposed for the act of submitting tax returns from 01 to 30 days after expiration of the prescribed time limits, except the cases specified in clause 1 of this Article.

3. Fines ranging from VND 5,000,000 to VND 8,000,000 shall be imposed for the act of submitting tax returns from 31 to 60 days after expiration of the prescribed time limits.

4. Fines ranging from VND 8,000,000 to VND 15,000,000 shall be imposed for one of the following violations:

a) Filing tax returns from 61 to 90 days after expiration of the prescribed time limits;

b) Filing tax returns at least 91 days after expiration of the prescribed time limits if none of additional taxes is incurred;

c) Failing to submit tax returns if none of additional taxes is incurred;

d) Failing to submit annexes under regulations regarding tax administration by enterprises having related-party transactions, enclosing CIT finalization dossiers.

5. Fines ranging from VND 15,000,000 to VND 25,000,000 shall be imposed for the act of filing tax returns more than 90 days after the prescribed deadline if such act results in additional taxes to be paid, and the taxpayer has fully paid taxes, deferred amounts into the state budget before the time of the tax authority’s announcement of the decision on tax inspection and examination, or before the time of the tax authority’s issuance of the report on the deferred submission of tax returns under the provisions of clause 11 of Article 143 in the Law on Tax Administration.

In case where the fine amount prescribed in this clause is greater than the tax amount additionally incurred in the tax return, the maximum amount of fine for this act shall be equal to the tax amount payable specified in the tax return and shall not be less than the average of fine amounts in the range prescribed in clause 4 of this Article.

6. Remedies:

a) Compelling the full payment of deferred tax amounts into the state budget with respect to the commission of the acts prescribed in clause 1, 2, 3, 4 and 5 of this Article if the taxpayer delays filing their tax return, leading to the late payment of taxes;

b) Compelling the submission of tax returns, enclosing annexes, in case of committing the acts specified in point c and d of clause 4 of this Article.

Note: The fines mentioned above are imposed upon organizations. The fines imposed upon an individual are 1/2 of those imposed upon an organization.

Thus, depending on the delay time, an individual who submits a late personal income tax settlement declaration may be fined as little as a warning to a maximum fine of VND 12,500,000.

LawNet