How to register a MoMo account in Vietnam in 2024? How to register for a MoMo account on a mobile phone?

How to register a MoMo account in Vietnam in 2024? How to register for a MoMo account on a mobile phone?

Here is a guide on how to register for MoMo:

Step 1:

Download and install the MoMo app on your Android or iPhone phone. You can download MoMo for Android here and MoMo for iOS here.

Download MoMo for Android

Download MoMo for iOS

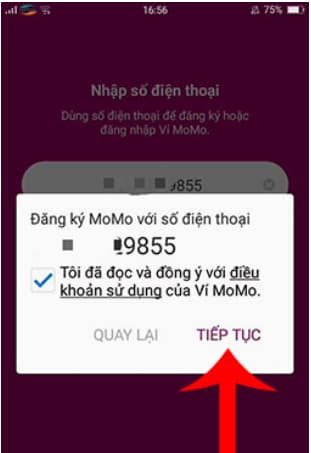

Step 2:

Next, you register for a MoMo wallet account using the phone number you are currently using. Enter your phone number correctly and then click on "Continue". You agree to the terms of use of the MoMo e-wallet by clicking on "Continue"."

Step 3:

Immediately, you will receive an OTP code to the phone number you used to register for the MoMo account in the previous step. At this point, you proceed to enter this code to proceed to the password creation section for your MoMo account.

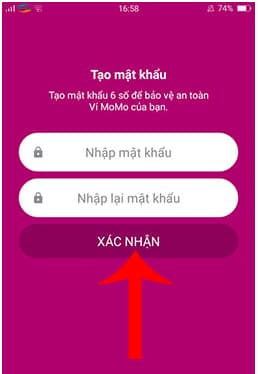

Step 4:

You enter a password to protect your MoMo wallet, once entered, press Confirm

Step 5:

To further authenticate and protect your MoMo account, you need to provide additional information such as: Full name, email address, and then click on Confirm.

Once completed, you will be taken to the main interface of the MoMo e-wallet, and the MoMo account registration process is complete. Now you can explore and experience the useful features that MoMo offers.

The above is the registration process for MoMo for your reference

How to register a MoMo account in Vietnam in 2024? How to register for a MoMo account on a mobile phone? (Image from the Internet)

How many bank accounts and cards can be linked to a MoMo account in Vietnam?

Each MoMo wallet can only be linked to a single bank account at a time.

Currently, MoMo is a partner with many banks such as Vietcombank, Vietinbank, VPBank, TPBank, OCB, SCB, ACB, VRB, Eximbank, Agribank, BIDV, VIB, Shinhan Bank, Bảo Việt Bank, and Sacombank debit cards.

What are rules of card usage in Vietnam?

Pursuant to the provisions of Article 17 of Circular 19/2016/TT-NHNN amended and supplemented by Article 1 of Circular 17/2021/TT-NHNN, Article 1 of Circular 26/2017/TT-NHNN and Article 1 Circular 28/2019/TT-NHNN, rules of card usage include the following:

- Each cardholder must provide sufficient and accurate information as required by the card issuer upon entering into the agreement on card issuance and usage and take responsibility for the accuracy of the information provided.

- When using a credit card or a debit card with overact facility, the cardholder must use money properly and make full and due repayment of loan amounts and interests thereof to the card issuer as specified in the agreement concluded with the card issuer.

- Scope of card usage:

+ Debit cards and personalized prepaid cards are used to conduct card transactions as agreed upon by the cardholder and the card issuer;

+ Credit cards shall be used to pay for goods and services; and to deposit and withdraw cash as agreed upon between the cardholder and the card issuer. Credit cards shall neither be used to transfer money to checking accounts, debit cards and prepaid cards nor credit such accounts and cards;

+ Anonymous prepaid cards shall be used to pay for permitted goods and services via all POS terminals in Vietnam’s territory; and shall not be used to conduct card transactions on the Internet or via mobile applications or to withdraw cash. Deposit into anonymous prepaid cards is regulated by Clause 2 Article 14 of Circular 19/2016/TT-NHNN

+ Supplementary card issued to a supplementary cardholder aged under 15 years is not used to withdraw cash but only for pay for purchase properly as agreed upon in writing between the card issuer and the principal cardholder.

+ Cards may be used to pay for goods and services permitted by Vietnamese law, including those purchased overseas; except the cases specified in Point c of Article 17 of Circular 19/2016/TT-NHNN.

+ Debit cards, credit cards, personalized prepaid cards issued electronically may neither draw cash in foreign currency in foreign countries nor making international payments except for clause 4 Article 10a of Circular 19/2016/TT-NHNN

- The card issuer, acquirer shall perform necessary measures to update, check, review, compare and identify customers during the card use

Vietnam: Which entities should be notified promptly when a card is lost?

Pursuant to Article 19 of Circular 19/2016/TT-NHNN, regulations on actions against cases of card losses or card disclosure are as follows:

Actions against cases of card losses or card disclosure

1. When a card is lost or a card’s information is disclosed, the cardholder must promptly notify the card issuer.

2. Upon the receipt of the notification, the card issuer shall lock the card and cooperate with relevant entities to carry out necessary operation to prevent possible damage and send another notification to the cardholder. The time limit for the actions against notification received from the cardholder does not exceed 5 working days for the card whose BIN is issued by the State Bank or 10 working days for the card whose BIN is issued by an international card association from the date on which the notification is received.

3. In case where such card is misused that cause damage, the card issuer and the cardholder shall allocate their equivalent responsibility and negotiate the measures for damage. In the event that both parties fail to reach a consensus on the measures for damage, regulations of law shall apply.

Thus, when a card is lost, the cardholder must promptly notify the card issuer.

LawNet