How to declare tax of foreign contractors doing business in Vietnam? What taxes do foreign contractors have to pay?

What taxes do foreign contractors have to pay when doing business in Vietnam?

According to the provisions of Article 5 of Circular 103/2014/TT-BTC as follows:

Taxes

1. Taxpayers defined in Clause 2 Article 4 Chapter I are obliged to withhold VAT and corporate income tax as prescribed in Section 3 Chapter II before paying foreign contractors and foreign sub-contractors.

2. Foreign contractors and foreign sub-contractors are foreign businesspeople that pay VAT as prescribed in this Circular or pay personal income tax as prescribed by regulations of law on personal income tax.

3. Foreign contractors and foreign sub-contractors shall pay other taxes, fees and charges in accordance with applicable regulations of law on taxes, fees and charges.

Thus, when doing business in Vietnam, foreign contractors must pay the following taxes:

- Foreign contractor is a business organization that fulfills the obligation of value-added tax (VAT), corporate income tax (CIT)

- Foreign contractors being foreign individuals doing business shall fulfill their VAT obligations under the guidance in this Circular and personal income tax (PIT) according to the law on PIT.

- For other taxes, fees and charges, the foreign contractor shall comply with the current legal documents on taxes, fees and other fees.

How to declare tax of foreign contractors doing business in Vietnam? What taxes do foreign contractors have to pay?

What are the regulations for taxpayers being foreign contractors in Vietnam?

Pursuant to Article 4 of Circular 103/2014/TT-BTC stipulating as follows:

Taxpayers

1. Foreign contractors and foreign sub-contractors who meet the requirements in Article 8 Section 2 Chapter II or Article 14 Section 4 Chapter II, do business in Vietnam, or earn income in Vietnam. The business is done under the main contract with a Vietnamese entity or another foreign entity doing business in Vietnam under the subcontract.

Foreign contractors and foreign sub-contractors that have permanent establishments in Vietnam or are residents of Vietnam shall be determined in accordance with the Law on Corporate income tax, the Law on Personal income tax, and guiding documents.

If permanent establishments and residents are defined otherwise by a Double Taxation Agreement to which Vietnam is a signatory, such Agreement shall apply.

2. Organizations established and operated under Vietnam’s law or registers its operation under Vietnam law; business entities that purchase services, services attached to goods, or pay income in Vietnam under main contracts or subcontracts; purchase goods in the form of domestic import or under Incoterms; distribute goods or provide services on behalf of foreign entities in Vietnam (hereinafter referred to as Vietnamese entities) include:

- Business organizations established under Company law, the Law on Investment, and the Law on Cooperatives;

- Business organizations of political organizations, socio-political organizations, social organizations, socio-professional organizations, armed force units, public service providers, and other organizations;

- Petroleum contractors defined in the Law on Petroleum;

- Branches of foreign companies permitted to operate in Vietnam;

- Foreign organizations or representatives of foreign organizations permitted to operate in Vietnam;

- Air ticket outlets or agents in Vietnam of foreign airlines that are entitled to enter and leave Vietnam to provide transport services directly or in cooperation;

- Organizations and individuals that provide sea transport services of foreign shipping companies; agents in Vietnam of foreign logistics companies;

- Securities companies, securities issuers, asset management companies, commercial banks where securities investment funds or foreign organizations open their securities investment accounts

- Other organizations in Vietnam;

- Businesspeople in Vietnam.

Taxpayers defined in Clause 2 Article 4 Chapter I are obliged to withhold VAT and corporate income tax as prescribed in Section 3 Chapter II before paying foreign contractors and foreign sub-contractors.

Thus, taxpayers being foreign contractors must comply with the conditions specified in Article 8 Section 2 Chapter II or Article 14 Section 4 Chapter II of this Circular.

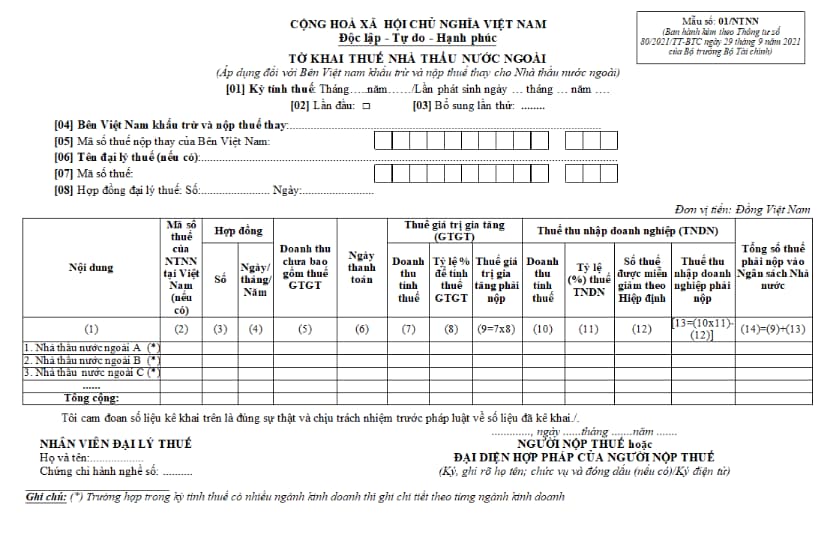

What is the most accurate tax declaration for foreign contractors doing business in Vietnam?

Tax declarations for foreign contractors doing business in Vietnam are specified in Form No. 01/NTNN issued together with Circular 80/2021/TT-BTC as follows:

Download Tax return of foreign contractors doing business in Vietnam: here

LawNet