Circular 23/2023/TT-BTC: To replace Circular 45/2018/TT-BTC guiding the regime for calculating the depreciation of fixed assets in Vietnam?

- Circular 23/2023/TT-BTC: To replace Circular 45/2018/TT-BTC guiding the regime for calculating the depreciation of fixed assets in Vietnam?

- What are the assets that are not subject to depreciation in Vietnam?

- What is the time to calculate the depreciation of fixed assets in Vietnam according to the latest regulations?

Circular 23/2023/TT-BTC: To replace Circular 45/2018/TT-BTC guiding the regime for calculating the depreciation of fixed assets in Vietnam?

On April 25, 2023, the Minister of Finance issued Circular 23/2023/TT-BTC on guiding the regime for managing and calculating the depreciation of fixed assets of agencies, organizations or units and fixed assets handed to enterprises by the State without calculation of the state capital portion of such enterprises.

Accordingly, Circular 23/2023/TT-BTC guides the determination of fixed assets in Article 3 of Circular 23/2023/TT-BTC as follows:

Fixed Asset Standard

1. Asset identification:

a) Asset for independent use is identified as an asset.

b) A system consisting of many individual asset parts linked together to perform a certain function or functions, without any part of which, the whole system cannot operate. then the system is identified as an asset.

c) A system consisting of many separate, interconnected assets, in which each component has a different useful life and functions independently, and requires separate management. each asset segment, each individual asset part is identified as an asset.

d) Working and/or producing animals, each animal is identified as an asset.

dd) Perennial garden on an independent land campus or each individual perennial plant is identified as an asset.

e) The land use right for each land parcel or the area assigned to agencies, organizations or units in each land parcel is determined as an asset.

g) Intellectual property rights are registered and established according to each certificate of copyright registration, certificate of registration of rights related to copyright, protection title of industrial property objects, Plant variety protection is defined as an asset.

h) Each application software is identified as an asset.

i) The trademark of each public non-business unit is identified as an asset.

2. Assets specified in Clause 1 of this Article (except for those specified in Clause 3 of this Article) shall be determined as fixed assets when simultaneously satisfying 02 of the following criteria:

a) The useful life is 01 (one) year or more.

b. The cost is 10.000.000 VND (ten million VND) or higher.

3. Assets specified in Clause 1 of this Article at public non-business units self-financed for recurrent expenditures and investment and asset expenditures at public non-business units are subject to full depreciation of fixed assets. service prices as prescribed by law and assets at public non-business units may be used all the time for business activities, leasing, joint ventures or association without forming a new legal entity according to regulations. According to the law, it is determined as a fixed asset when the following two criteria are simultaneously satisfied:

a) The useful life is 01 (one) year or more.

b) Satisfy the standard on historical cost of fixed assets according to regulations applicable to enterprises.

Thus, according to the above regulations, assets are determined as fixed assets when satisfying two conditions:

- The useful life is 01 (one) year or more.

- The original price is from 10,000,000 VND or more.

However, for assets in public non-business units, they shall only be determined as fixed assets when meeting 02 conditions:

- The useful life is 01 (one) year or more.

- Satisfy the conditions on historical cost of fixed assets according to regulations applicable to enterprises.

Circular 23/2023/TT-BTC: To replace Circular 45/2018/TT-BTC guiding the regime for calculating the depreciation of fixed assets in Vietnam?

What are the assets that are not subject to depreciation in Vietnam?

Pursuant to Clause 3, Article 11 of Circular 23/2023/TT-BTC stipulating the scope of fixed assets for depreciation has the following contents:

Scope of fixed assets for depreciation

1. Existing fixed assets at agencies, organizations and units and fixed assets assigned by the State to enterprises for management, excluding the state capital in enterprises, must be calculated for depreciation, except for the following cases: accordance with the provisions of Clauses 2, 3 and 4 of this Article.

2. Fixed assets at public non-business units subject to depreciation include:

a) Fixed assets at public non-business units to cover recurrent expenses and investment expenses by themselves.

b) Fixed assets at public non-business units which must be fully depreciated into service prices as prescribed by law.

c) Fixed assets at public non-business units that do not fall within the scope specified at Points a and b of this Clause may be used for business, leasing, joint venture or association activities without forming a legal entity. new in accordance with the law.

3. No depreciation or amortization is required for:

a) Fixed assets are land use rights in cases where the value of land use rights must be determined for calculation into the property value specified in Article 100 of Decree No. 151/2017/ND-CP.

b) Specific fixed assets specified at Point c, Clause 1, Article 4 of this Circular.

c) Fixed assets that have been fully depreciated or fully depreciated but are still usable (including fixed assets received by public non-business units after the expiry of the joint venture or association; ).

d) Fixed assets that have not been fully depreciated or fully depreciated but have been damaged and cannot be used.

4. For fixed assets that are trademarks of public non-business units used in joint venture or association activities, the brand value of public non-business units to contribute capital to joint ventures or associations shall be distributed annual/monthly/monthly expenses for joint ventures or associations as prescribed in Clause 3, Article 15 of this Circular.

Accordingly, fixed assets that are not subject to depreciation and amortization include:

- Fixed assets are land use rights for the cases in which the value of land use rights must be determined to calculate the property value specified in Article 100 of Decree 151/2017/ND-CP

- Specific fixed assets according to regulations.

- Fixed assets have been fully depreciated or fully depreciated but are still usable.

- Fixed assets that have not been fully depreciated or fully depreciated but have been damaged and cannot be used.

What is the time to calculate the depreciation of fixed assets in Vietnam according to the latest regulations?

From June 10, 2023, the time to calculate the depreciation of fixed assets shall comply with the provisions of Article 13 of Circular 23/2023/TT-BTC, specifically as follows:

Depreciation period and depreciation rate of fixed assets

1. The time to calculate the amortization and the rate of depreciation of tangible fixed assets shall comply with the provisions in Appendix No. 01 issued together with this Circular; except for the following cases:

a) For tangible fixed assets used in areas with weather conditions, environmental conditions affecting the level of depreciation of fixed assets, when necessary, the time for calculating the depreciation must be specified. and the rate of depreciation of fixed assets is different from that specified in Appendix 01 issued with this Circular, the Ministers, heads of central agencies and provincial-level People's Committees shall specify. The adjustment of the depreciation rate of fixed assets to increase or decrease must not exceed 20% of the depreciation rate of the corresponding fixed assets specified in Appendix 01 issued with this Circular.

b) For fixed assets with changes in their historical cost in the case of upgrading or expanding fixed assets according to projects approved by competent agencies or persons specified at Point b, Clause 1, Article 9 of this Circular; In this case, the time to calculate the depreciation of fixed assets is equal to (=) the used time of the asset before changing its historical cost plus (+) the remaining amortization time of the asset after upgrading or opening. wide. In which, the remaining depreciation time of the asset after upgrading and expanding is determined by the following formula:

Remaining depreciation period of assets after upgrading and expanding = (Original cost of fixed assets after change - Accumulated depreciation and amortization of fixed assets as of 31st date) /12 of the year of change of historical cost) / Annual depreciation of assets from the year of change of historical cost determined according to the provisions of Point a, Clause 6, Article 14 of Circular 23/2023TT-BTC

...

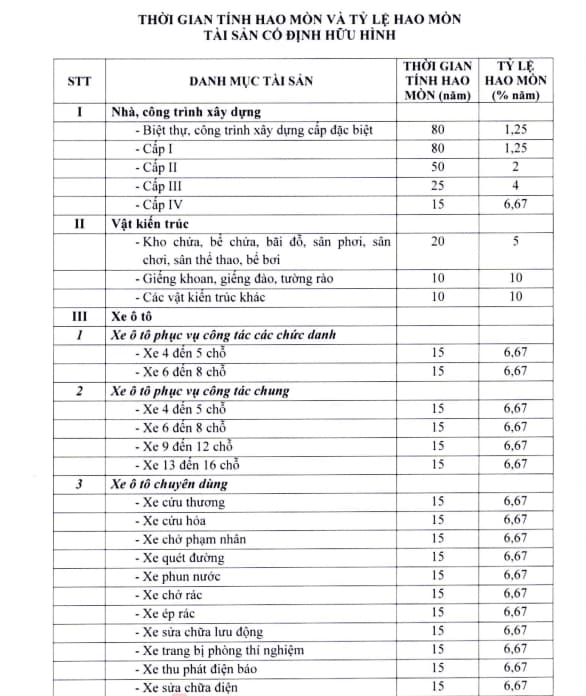

Thus, according to the above regulations, from June 10, 2023, the time for calculating tangible fixed assets shall comply with the provisions in Appendix 01 issued together with Circular 23/2023/TT-BTC (except for the special cases mentioned in Article 13 above).

Appendix 01 issued together with Circular 23/2023/TT-BTC stipulates as follows:

See the entire Appendix on the time to calculate the depreciation of fixed assets here: download

Circular 23/2023/TT-BTC takes effect from June 10, 2023, replacing Circular 45/2018/TT-BTC.

LawNet