Vietnam: What is the application form for tax and land rental deferral in 2024?

Where to download the newest application form for tax and land rental deferral in 2024 in Vietnam?

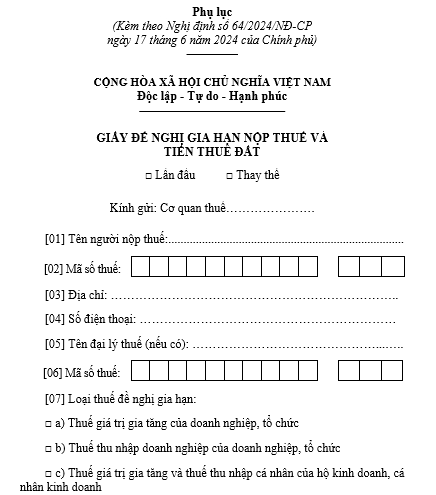

The newest application form for tax and land rental deferral in 2024 is included in the Appendix issued with Decree 64/2024/ND-CP:

>> Download the newest application form for tax and land rental deferral in 2024: Download

Vietnam: What is the application form for tax and land rental deferral in 2024? (Image from the Internet)

What are the procedures for tax deferral in Vietnam during 2024?

Under Article 5 of Decree 64/2024/ND-CP, the procedures for tax deferral in 2024 are as follows:

Step 1. The taxpayer who directly declares and pays tax to the tax authority and is eligible for a deferral shall submit the first or corrected newest application form for tax and land rental deferral (hereinafter referred to as the application form for tax deferral) electronically, directly to the tax authority or via postal services to the managing tax authority in charge of the entire amount of tax and land rent incurred during the extended tax period, together with the monthly (or quarterly) tax declaration according to tax management regulations.

In case the application form for tax deferral is not submitted concurrently with the tax declaration (monthly or quarterly), the latest submission date is September 30, 2024. The tax authority shall still grant the deferral for the tax or land rent incurred before the application form for tax deferral is submitted.

If the taxpayer has multiple items eligible for deferral managed by different tax authorities, the primary managing tax authority must communicate the application form for tax deferral to the relevant tax authorities.

Step 2. The taxpayer must self-determine and take responsibility for the accuracy of the deferral request to ensure eligibility as per Decree 64/2024/ND-CP.

If the taxpayer submits the application form for tax deferral after September 30, 2024, they will not be eligible for an deferral of tax or land rent payment according to Decree 64/2024/ND-CP.

If the taxpayer supplements the tax declaration leading to an increase in the payable amount, and this supplementary declaration is submitted before the extended payment deadline, the extended amount includes the increased amount due to the supplementary declaration.

If the taxpayer supplements the tax declaration after the extended payment deadline, no deferral will be applied to the additional amount.

Step 3. The tax authority is not required to notify the taxpayer about the acceptance of the tax and land rent payment extension.

If during the deferral period, the tax authority determines that the taxpayer is not eligible for an extension, it shall notify the taxpayer in writing. The taxpayer must pay the full amount of tax, land rent, and late payment interest for the deferral period to the state budget.

If after the deferral period, the competent authority finds through inspection or audit that the taxpayer is not eligible for an deferral under Decree 64/2024/ND-CP, the taxpayer must pay the outstanding tax, fines, and late payment interest to the state budget.

Step 4. No late payment interest will be charged for the taxes and land rent extended (even if the taxpayer submits the application form for tax deferral after submitting the tax declaration as stipulated in Step 1, or if the competent authority finds that the taxpayer eligible for the deferral has an increased amount of tax due for the extended period).

If the tax authority has charged late payment interest (if any) for the extended tax amounts as per Decree 64/2024/ND-CP, the tax authority will make adjustments to cancel the late payment interest.

Step 5. Investors of projects and works funded by the state budget, payments from the state budget for basic construction works of ODA projects subject to value-added tax must attach the tax authority’s receipt notification of the application form for tax deferral or the application form for tax deferral with confirmation of tax authority submission by the contractor when processing payments with the State Treasury.

The State Treasury, based on the documents provided by the investor, will not deduct the value-added tax during the deferral period.

After the deferral period ends, the contractor must pay the full amount of the extended tax according to regulations.

Which entities are eligible for tax deferral in Vietnam in 2024?

Under Article 3 of Decree 64/2024/ND-CP, the following entities are eligible for an deferral of value-added tax, corporate income tax, and personal income tax in 2024:

(1) Enterprises, organizations, households, household businesses, and individuals operating in the following production sectors:

- Agriculture, forestry, and fisheries;

- Food production and processing; textiles; garment manufacturing; leather and related product manufacturing; wood processing and manufacturing of wood, bamboo, rattan products (excluding beds, wardrobes, tables, and chairs); straw, rattan, and woven material products manufacturing; paper and paper product manufacturing; rubber and plastic product manufacturing; other non-metallic mineral product manufacturing; metal manufacturing; mechanical processing; metal treatment and coating; manufacturing electronic products, computers, and optical products; manufacturing automobiles and other motor vehicles; manufacturing beds, wardrobes, tables, and chairs;

- Construction;

- Publishing activities; film production, television program production, sound recording and music publishing;

- Crude oil and natural gas extraction (excluding corporate income tax from crude oil, condensate, and natural gas collected according to agreements and contracts);

- Beverage manufacturing; printing, and the reproduction of recorded media; coke and refined petroleum product manufacturing; chemical and chemical product manufacturing; manufacturing prefabricated metal products (excluding machinery and equipment); manufacturing motorcycles; machinery and equipment repair, maintenance, and installation;

- Wastewater drainage and treatment.

(2) Enterprises, organizations, households, household businesses, and individuals operating in the following business sectors:

- Transportation and warehousing; accommodation and food services; education and training; health and social assistance activities; real estate business activities;

- Labor and employment service activities; travel agency activities, tour business and supporting services, related to the promotion and organization of tours;

- Art and entertainment creation activities; library, archive, museum, and other cultural activities; sports, amusement, and recreation activities; cinema activities;

- Broadcasting activities; computer programming, consultancy, and related activities; information service activities;

- Mining support services.

(3) Enterprises, organizations, households, household businesses, and individuals engaged in the production of prioritized supporting industrial products; key mechanical products.

(4) Small and micro enterprises as defined by the Law on Supporting Small and Medium Enterprises 2017 and Decree 80/2021/ND-CP of the Government of Vietnam detailing some provisions of the Law on Supporting Small and Medium Enterprises.

The business lines of enterprises, organizations, households, household businesses, and individual businesses mentioned above must have production, business activities, and revenue generation in 2023 or 2024.

- When is the deadline for paying tax, duty payment guarantee and tax deposit in Vietnam?

- Are natural aquatic resources exempt from severance tax in Vietnam?

- Are natural swallow's nests subject to severance tax in Vietnam?

- What are the principles for developing a List of goods to be imported free of duty in Vietnam?

- How long is the CIT period of the first year in Vietnam?

- Shall individuals be entitled to tax refund if their taxed incomes do not reach a tax-liable level in Vietnam?

- What are regulations on responsibilities of income payer regarding PIT refund when being delegated to settle tax in Vietnam?

- Is it necessary to terminate the tax identification number when a business temporarily suspends its operations in Vietnam?

- What is the value-added tax declaration form for 2024 in Vietnam?

- What are forms for declaring corporate income tax in Vietnam?